In early June 2026, the AI chip sector experienced a landmark market swing. A leading custom ASIC specialist reported quarterly revenue up 48% year-over-year, yet its stock plunged over 13% in after-hours trading. This seemingly contradictory outcome precisely highlights a reality: when market expectations for a company are pushed to extreme highs, even a minor deviation from "perfection" can trigger a sentiment reversal, regardless of solid underlying performance. As of June 5, 2026, Gate data shows that after Broadcom (AVGO) surged to $495 this week, it has since retreated to a near-term low, currently trading at $419, with an intraday loss exceeding 12%.

Were Broadcom’s Quarterly Results Actually Good?

From an objective financial perspective, this earnings report was far from weak. Q2 total revenue reached $22.187 billion, up ~48% year-over-year, hitting a multi-year high for quarterly revenue growth and slightly beating the consensus estimate of $22.129 billion. Non-GAAP adjusted EPS came in at $2.44, also above analyst expectations of $2.40. The semiconductor solutions segment generated $15.009 billion in revenue, beating Bloomberg’s consensus of $14.65 billion—actual performance outperformed institutional forecasts.

More notably, the quality of earnings was strong. Adjusted EBITDA hit $15.2 billion, representing 69% of revenue, and operating margins reached a record 67%, both exceeding the company’s prior guidance. Free cash flow stood at $10.3 billion, or 46% of revenue, demonstrating robust cash generation. Meanwhile, the debt burden from the VMware acquisition has been effectively absorbed, with the leverage ratio dropping to 1.8x, returning to a healthy pre-acquisition level.

Based on these metrics, there were no signs of deterioration in the company’s core operations. The issue wasn’t "how poorly it performed," but rather "how high market expectations had climbed."

Why Market Expectations Far Exceeded Actual Guidance

In the five trading days before the earnings release, the company’s market cap rose by over $300 billion, with the stock hitting a 52-week high of $495 in regular trading and gaining nearly 39% year-to-date. At such extreme valuations, the implied market expectation bar had been raised to an almost insurmountable height. A P/E ratio exceeding 90x leaves virtually no room for any performance shortfall.

The direct trigger for the sharp price correction was the "gap" in AI semiconductor guidance. The company guided Q3 AI semiconductor revenue at $16.0 billion, while Bloomberg’s consensus estimate was $17.2 billion—a difference of about $1.2 billion (7%). For the full fiscal year 2026, AI chip sales guidance of $56.0 billion also fell short of the average analyst estimate of $57.6 billion, a gap of nearly $1.6 billion (2.8%).

Broadcom AI Semiconductor Guidance vs. Market Expectations — The Expectation Gap Triggered a >12% Price Correction

| Item | Market Extreme Expectation ($B) | Company Actual/Guidance ($B) | Expectation Gap | Market Reaction |

|---|---|---|---|---|

| Q2 AI Semiconductor Revenue (Actual) | ~10.5 – 10.8 | 10.8 | Roughly in line | Hit $495 intraday high |

| Q3 AI Semiconductor Guidance | 17.2 (Bloomberg consensus) | 16.0 | -$1.2B (-7%) | After-hours plunge >13% |

| FY2026 Full-Year AI Chip Expectation | 57.6 (analyst average) | 56.0 | -$1.6B (-2.8%) | Intraday max drawdown >12% |

A logical interpretation: this selloff was not driven by fundamental deterioration, but by a concentrated release of "expectation gap" pressure. When a stock has already climbed at a near-parabolic slope within a short period, any guidance below a "blowout" level can trigger profit-taking—not because the guidance implies growth stagnation.

Is the Upside Trend in Fundamentals Still Intensifying?

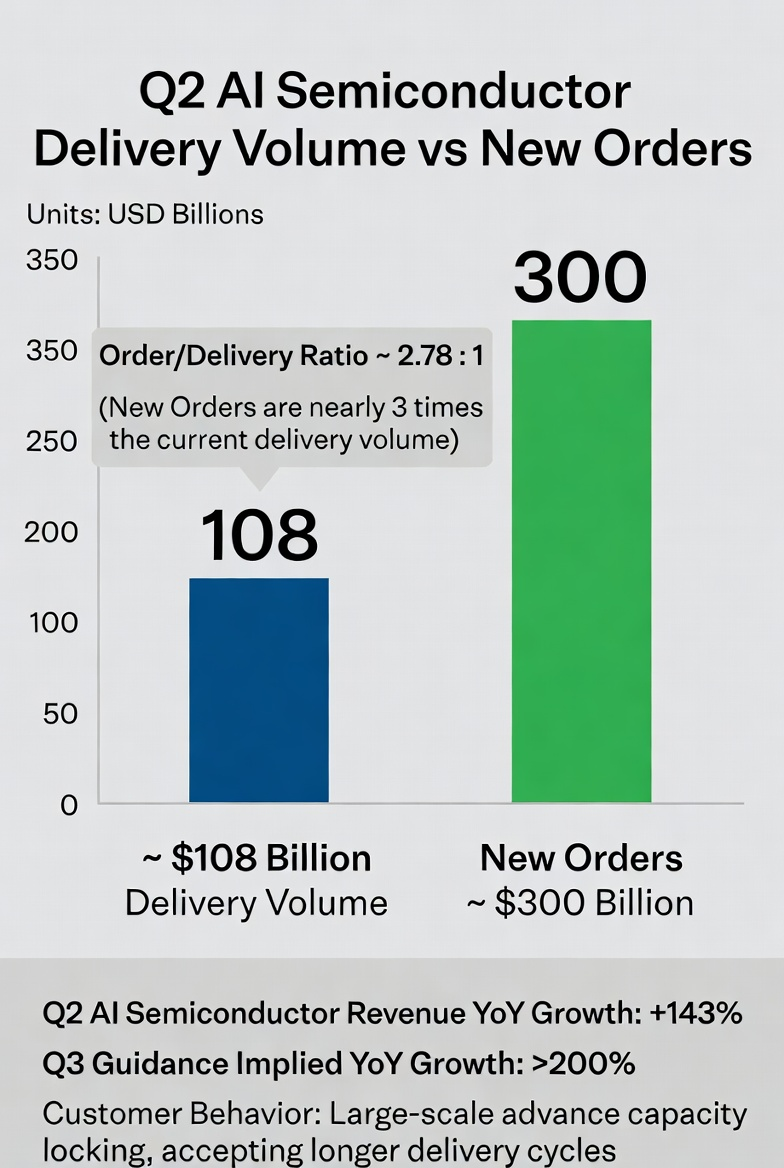

From an operational standpoint, upward momentum has not only held but accelerated. AI semiconductor revenue reached $10.8 billion in Q2, up a substantial 143% year-over-year and $2.4 billion sequentially, broadly in line with expectations. From Q1 to Q2, AI business growth continued to ramp, and the implied year-over-year growth rate for Q3 guidance exceeds 200%—a sign that customer orders are pouring in at an even faster pace from an already large base.

Order signals are even more striking. During the earnings call, the CEO revealed that while the company delivered $10.8 billion in AI semiconductors in the quarter, new AI semiconductor orders placed during that period exceeded $30 billion. That $30 billion in new orders is nearly three times the delivery amount, indicating that downstream demand has not contracted but remains extremely robust. Customers are aggressively pre-booking capacity, and their acceptance of longer lead times itself strongly underscores the sustainability of demand.

Broadcom AI Semiconductor — Current Deliveries vs. New Orders (FY2026 Q2)

How AI Inference Market Expansion Reshapes the Industry Landscape

To understand the deeper backdrop of this volatility, we must place it within the framework of a structural shift in the AI computing market. The explosion of AI inference workloads is the most critical variable in the chip industry in 2026. According to institutional data, AI inference loads have risen from about one-third of total computing demand in 2023 to two-thirds in 2026, with the market size expected to be 2 to 3 times that of training hardware.

A direct consequence of this structural shift is that the economic advantage of custom ASICs is sharply magnified. In inference scenarios, ASICs offer far superior energy efficiency and unit cost advantages over general-purpose GPUs. For example, a custom inference chip developed by OpenAI in partnership with a leading supplier boasts an energy efficiency of 6.8 TOPS/W, compared to 4.5 TOPS/W for a comparable industry benchmark.

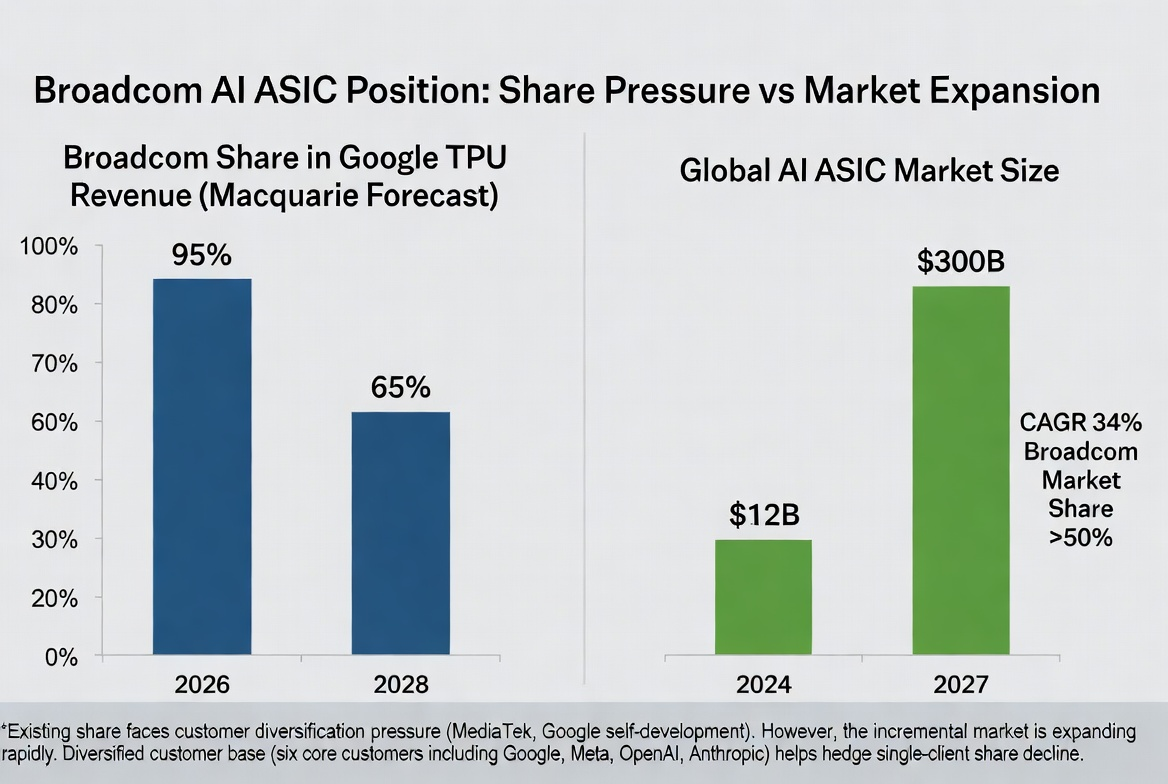

Goldman Sachs predicts that ASICs will account for 40% of the total AI chip market in 2026, further surpassing 45% by 2027, nearly matching GPU share. Counterpoint Research estimates that the AI ASIC market will grow from $12 billion in 2024 to $30 billion in 2027, a CAGR of 34%. Within this segment, Broadcom holds over 50% market share.

Thus, a reasonable inference is that this stock price adjustment has not undermined the long-term industrial foundation of the ASIC track. Instead, it provides a classic case study of the importance of "expectation management" in high-growth industries.

Can Competitive Shifts Disrupt the Industry Position?

Any rapidly expanding market inevitably attracts more entrants, and the ASIC space is no exception. Key customers are advancing diversification strategies. Some investment banks predict that due to MediaTek’s growing role and Google’s continued internal chip strategy, Broadcom’s share of Google TPU-related revenue will gradually decline from ~95% in 2026 to 80% in 2027 and further to 65% in 2028. Consequently, Macquarie trimmed its FY2028 earnings forecast by 21% and downgraded the stock from Outperform to Neutral.

Expected Change in Broadcom’s Share of Google TPU and Overall ASIC Market Expansion

Another competitive thread comes from the general-purpose GPU leader extending into custom solutions. Nvidia is actively building a custom chip design business, reportedly with a potential scale of up to $60 billion, directly encroaching on ASIC suppliers’ traditional territory. When the GPU leader leverages its dominance in the data center ecosystem to enter the custom market, competitive intensity in the space will undoubtedly increase in the coming years.

However, the moat in custom chips cannot be overlooked. Design, verification, and deployment processes typically take over two years, making customer switching costs extremely high. Broadcom currently has six core custom chip customers, including the most aggressive AI infrastructure spenders globally—Google, Meta, OpenAI, and Anthropic—and collaboration is deepening. With solid existing customer relationships, new entrants face significant barriers in time, validation, and ecosystem integration to disrupt the current landscape.

How Fund Rotation and Market Sentiment Affect Short-Term Trends

At the macro level, signs of a temporary cooling in AI trades are emerging. The tech sector selloff triggered by earnings was not an isolated event—the Dow Jones Industrial Average rose 1.73% that day, outperforming the Nasdaq by the widest margin in nearly 17 months, indicating a clear rotation from high-momentum tech stocks into traditional sectors. Financial and healthcare sector gains lacked significant fundamental catalysts, mainly reflecting capital absorption after high-momentum sectors declined.

Risk appetite indicators are currently at levels rarely seen in the past 10–15 years. If momentum factors continue to retreat, major indices may face pressure even with good market breadth. From a market feedback perspective, some institutions believe that chip stocks have rallied very strongly from March lows. A catalyst-triggered, multi-day correction would actually be healthy for the overall market.

Future Outlook

Based on current information, the following dimensions will be key in judging the subsequent trajectory:

Order delivery pace and capacity ramp efficiency. Whether the over $30 billion in new orders can be converted into revenue as planned depends on the speed of overcoming capacity bottlenecks. TSMC’s CoWoS advanced packaging capacity allocation is a critical reference variable—Broadcom’s pre-orders have surged to 200,000 wafers, up 122% year-over-year.

The pace of customers’ in-house chip strategy. Directional changes in custom chip investments by core customers like Google, Meta, and OpenAI will directly impact Broadcom’s medium- to long-term market share expectations.

Software business valuation restructuring. VMware’s software business, with annualized revenue approaching $30 billion and gross margins as high as 93–94%, is gaining independent valuation recognition in the market. Once the defensive value of the software business is fully priced, its ability to hedge semiconductor cyclicality will become an important valuation support.

The inflection point for AI inference market volume. ASIC’s core application is inference, not training. The actual pace of inference market adoption will directly determine the long-term growth potential of the custom chip space.

Summary

Broadcom’s post-earnings stock price correction is essentially a sentiment release triggered by "unfulfilled perfect expectations," not a reversal of fundamental trends. AI semiconductor revenue growth is accelerating, orders far exceed deliveries, and the structural advantage of custom ASICs in the expanding inference market remains intact. What the market truly needs to watch is the pace of competitive evolution—customer diversification and entry by peers into custom chips will pressure market share and margins in the medium to long term. The industry’s long-term upward trend is unshaken, but the process of expectation convergence continues in the near term, and pricing precision for this track will further increase.

FAQ

Which data in this earnings report actually beat market expectations?

Q2 total revenue of $22.187 billion exceeded the consensus of $22.129 billion; semiconductor segment revenue of $15.009 billion beat the $14.65 billion estimate; adjusted EPS of $2.44 surpassed the expected $2.40; adjusted EBITDA reached $15.2 billion, or 69% of revenue. Additionally, Q3 total revenue guidance of $29.4 billion also came in above the consensus of $28.7 billion.

What is the specific difference between AI semiconductor guidance and market expectations?

Q3 AI semiconductor revenue guidance is $16.0 billion versus the market average of $17.2 billion, a gap of about $1.2 billion. Full-year AI chip sales guidance is $56.0 billion versus the prior market average of $57.6 billion, a gap of about $1.6 billion. The discrepancy mainly stems from more aggressive market assumptions regarding the potential for FY2027 AI revenue exceeding $100 billion.

How much will customer in-house chips impact the business?

Investment banks predict that due to MediaTek’s increasingly important role and Google’s internal chip strategy, Broadcom’s share of Google TPU-related revenue may gradually decline from ~95% in 2026 to ~65% by 2028. However, with six core custom chip customers (Google, Meta, OpenAI, Anthropic, etc.), the impact of share changes at a single customer can be partially offset by customer portfolio diversification.

What is the competitive outlook for ASIC vs. GPU in the AI inference market?

Inference-side demand is becoming the core driver of the AI computing market. In inference scenarios, ASICs offer 3–5x energy efficiency improvements and a 40–60% reduction in total cost of ownership (TCO), providing significant economic advantages in scaled deployments. Institutions predict ASICs will account for over 45% of the AI chip market by 2027, closing in on GPU share.