LG Electronics, listed on the Korea Exchange (KRX) as a consumer electronics and vehicle solutions stock, operates through three major business divisions rather than relying on a single product line. To accurately assess the fundamentals of LG Electronics stock, it’s essential to clarify the product scope, customer structure, and revenue recognition methods within each segment.

Home appliance consumption cycles, advancements in display technology, and the ongoing shift toward automotive electronics collectively drive LG Electronics’ revenue. The home appliance segment is shaped by housing and replacement demand, the TV segment is linked to panel applications and brand premiums, while the vehicle segment depends on OEM contracts and vehicle production schedules. These cycles are not fully synchronized, so analyzing by division helps avoid oversimplifying the company’s performance.

From a Korean equity market perspective, LG Electronics stock represents a “consumer electronics + vehicle solutions” asset. Business model analysis should distinguish between end-brand operations, display technology applications, and in-vehicle electronic system supply, while also clearly defining financial boundaries with other LG Group listed entities. Differentiating LG Group’s listed entities is key to understanding the functional distinctions between LG Electronics and other units such as LG Display and LG Chem.

What are LG Electronics’ three main business divisions?

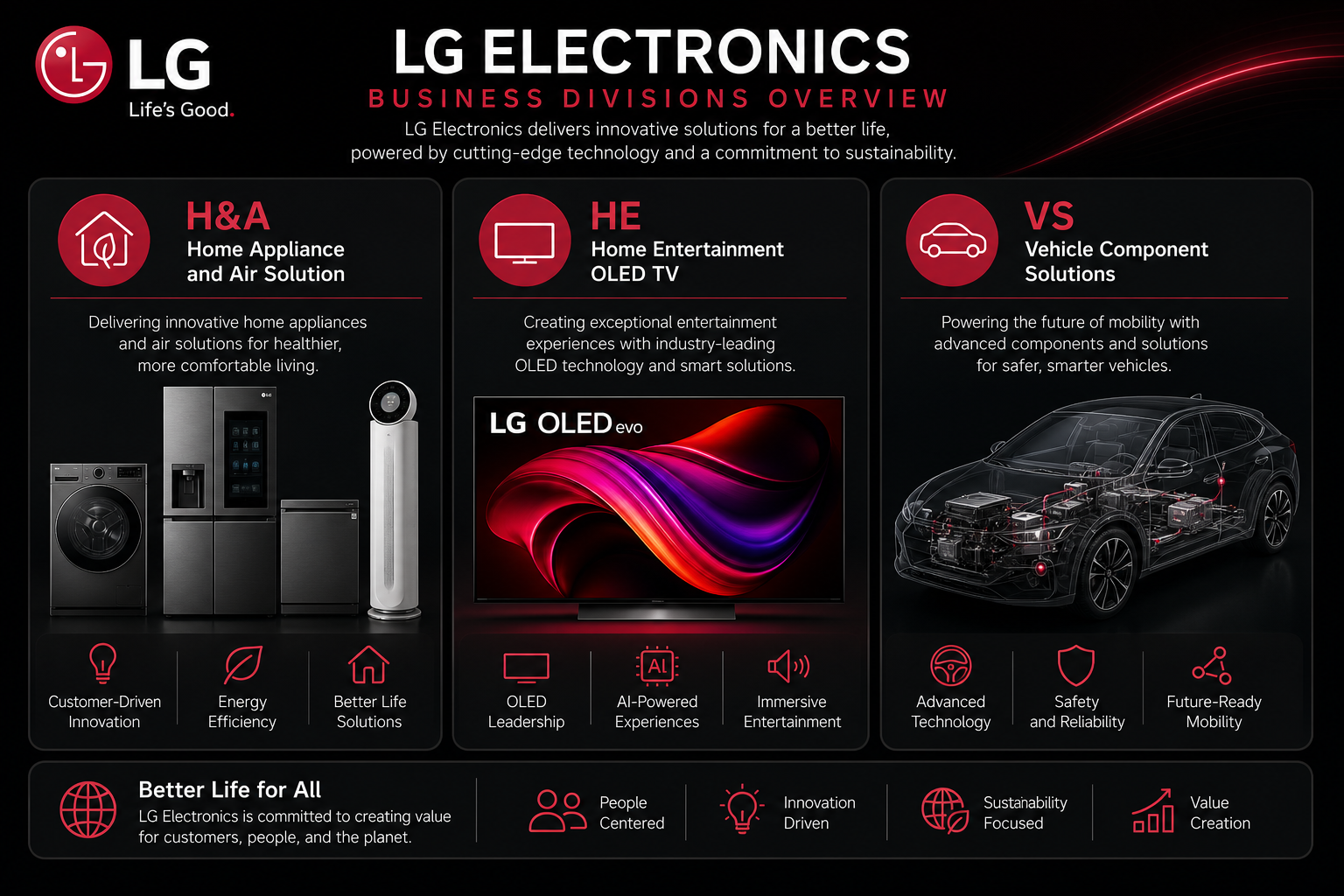

LG Electronics organizes its business into three divisions: Home Appliance & Air Solution (H&A), Home Entertainment (HE), and Vehicle component Solutions (VS). Each division operates with its own product lines, sales channels, and R&D focus, but consolidated revenue is reported at the group level.

| Division |

Abbreviation |

Core Function |

Primary Clients |

| Home Appliance & Air Solution |

H&A |

Manufacturing and sales of refrigeration, laundry, and air management equipment |

Households, commercial properties |

| Home Entertainment |

HE |

OLED/QNED TVs, audio-visual devices, webOS platform |

Home entertainment, content ecosystem partners |

| Vehicle component Solutions |

VS |

In-vehicle infotainment, displays, ADAS components |

Passenger and commercial vehicle OEMs |

This table outlines the functional roles of the three main divisions. H&A serves daily consumer needs, HE focuses on display technology and smart TV operating systems, and VS connects to the automotive supply chain. While there are technical synergies—such as display technologies spanning TVs and in-vehicle screens—each segment maintains independent revenue recognition, customer structures, and cycle sensitivities.

Figure 1. Structure of LG Electronics’ three main business divisions: H&A Home Appliance & Air Solution, HE Home Entertainment, and VS Vehicle component Solutions.

Figure 1. Structure of LG Electronics’ three main business divisions: H&A Home Appliance & Air Solution, HE Home Entertainment, and VS Vehicle component Solutions.

How does the Home Appliance & Air Solution (H&A) segment operate?

The H&A division encompasses refrigerators, washing machines, dryers, air conditioners, air purifiers, and commercial refrigeration equipment. This segment is anchored by its global appliance brand, reaching end users through physical retail, e-commerce, and project-based channels. Revenue comes primarily from complete product sales, with some lines also offering installation services and extended warranties.

H&A operates using a “category matrix + regional channel” model. High-end product lines emphasize energy efficiency and design premiums, with smart connectivity features being integrated into major appliance categories. However, complete product sales remain the main revenue source. Key revenue drivers include housing completions, replacement cycles, energy efficiency regulations, and raw material costs. Performance should be analyzed by sales volume, product mix (high-end share), and regional composition.

How does Home Entertainment (HE) position OLED TVs?

The HE division focuses on complete TV products, investing heavily in OLED self-emissive display technology and introducing QNED and other hybrid backlight lines. The webOS smart TV operating system extends beyond TVs to select audio-visual scenarios, serving as a content gateway and ecosystem interface. HE’s revenue comes from TV sales and a portion of software and content-sharing services.

OLED TVs deliver technological differentiation for the HE division, while QNED and other lines cover a broader price range. HE is closely tied to the panel supply chain, but product branding, channels, and after-sales service are managed independently. Revenue variables include panel costs, brand premiums, screen size upgrades, and regional market share. LG Electronics vs. Samsung Electronics offers a comparative framework for Korea’s leading consumer electronics firms, focusing on display technology strategy and market cycles.

What does the VS Vehicle component Solutions division include?

The VS division supplies OEMs with in-vehicle electronic systems and components, including central infotainment, rear seat entertainment, display modules, and ADAS (Advanced Driver Assistance Systems) electronics. Revenue for VS is typically linked to model designation, production ramp-up, and project lifecycle.

VS follows standard automotive parts industry practices: participating in OEM design bids, completing development and validation upon winning contracts, and recognizing revenue based on shipment volume or project agreements after mass production begins. The trend toward smart cockpits and electrification is driving the product line from standalone screens to integrated systems, with customer concentration typically higher than in consumer segments. Revenue drivers include auto sales, new energy vehicle penetration, configuration rates, and project ramp-up schedules. The business cycle is distinct from H&A and HE.

At-a-glance: Revenue drivers

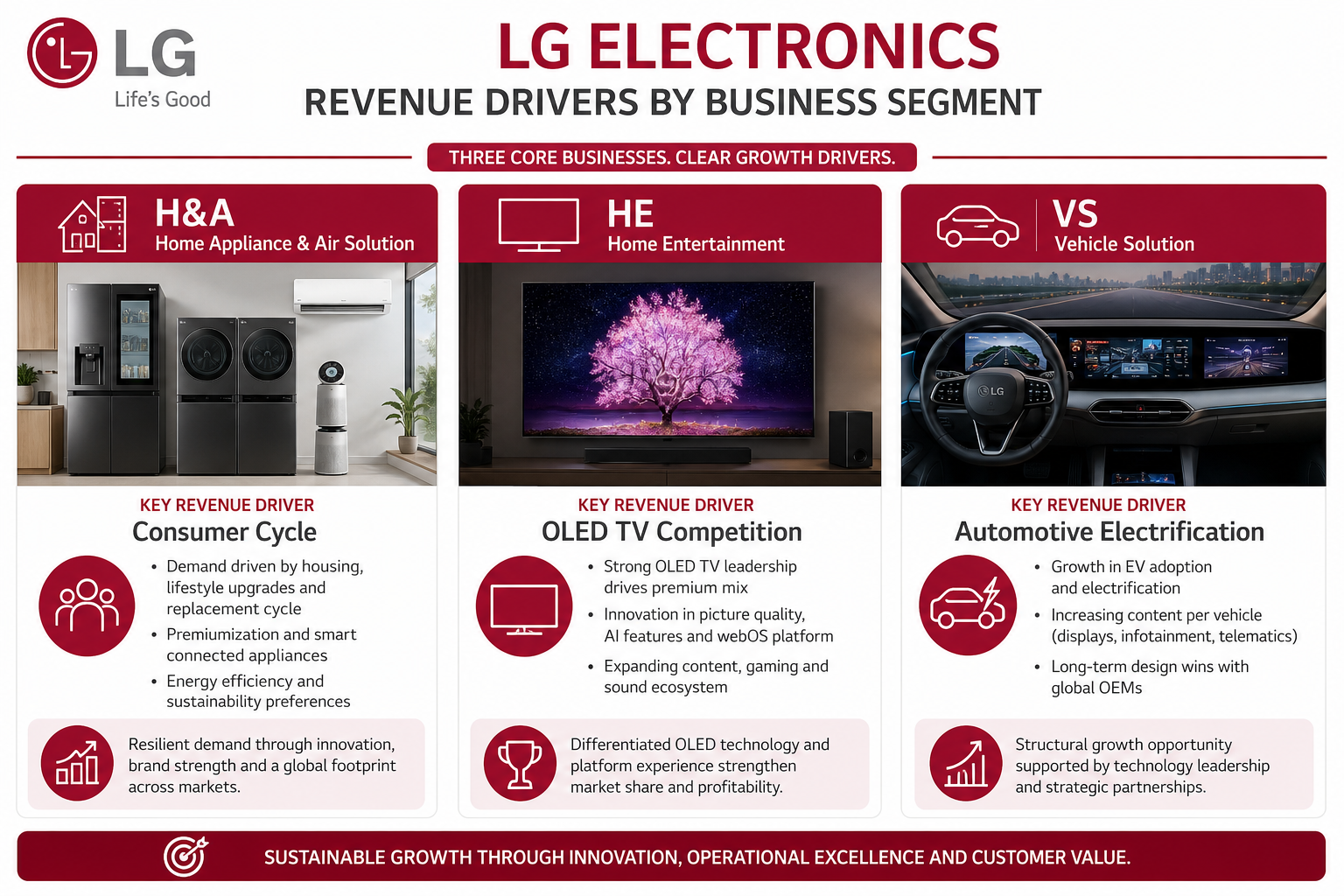

A thorough analysis of LG Electronics stock fundamentals requires side-by-side review of the revenue drivers for each major division. The table below summarizes the core variables and key metrics for each segment.

| Division |

Main Revenue Drivers |

Primary Cycle Source |

Key Metrics |

| H&A |

Appliance sales, product mix, regional blend |

Consumer cycle, housing and replacement demand |

High-end share, energy efficiency regulations, raw material costs |

| HE |

TV shipments, OLED/QNED mix, panel costs |

Display tech iteration, seasonal demand |

Screen size upgrades, brand premiums, competitive landscape |

| VS |

Designated projects, vehicle production, configuration penetration |

Automotive production/sales, electrification |

Customer concentration, project ramp-up, validation progress |

This table summarizes the mechanisms driving revenue, but does not constitute a performance forecast. The revenue contribution from each division will shift with segment growth and external factors. Segment data in financial reports is the primary source for tracking each division’s results. Segment-based analysis clarifies how “appliance leader,” “OLED TV,” and “vehicle solutions” labels map to verifiable fundamentals.

Figure 2. Revenue drivers for LG Electronics’ business divisions: consumer demand, display technology, automotive electronics, and regional mix.

Figure 2. Revenue drivers for LG Electronics’ business divisions: consumer demand, display technology, automotive electronics, and regional mix.

Business model analysis should also respect group entity boundaries: LG Electronics’ financial statements reflect only its own operations and do not include revenue from LG Display or LG Chem. Always verify listed entities by their full company names.

Summary

LG Electronics’ business model is anchored by the revenues of its three main divisions: H&A, HE, and VS. H&A provides stable cash flow in home appliances and air management, HE captures the technology and brand premium of OLED TVs and the webOS platform, and VS meets the specialized needs of automotive electronics and smart cockpits. Understanding revenue composition requires segment-level analysis of downstream clients, product cycles, and recognition schedules, while clearly differentiating LG Electronics from other LG Group entities and Korean industry peers.

FAQ

What are LG Electronics’ main revenue sources?

LG Electronics’ revenue primarily comes from three divisions: sales of refrigerators, washing machines, and air conditioners in Home Appliance & Air Solution (H&A); OLED/QNED TVs and audio-visual devices in Home Entertainment (HE); and in-vehicle infotainment, displays, and ADAS components in Vehicle component Solutions (VS).

How do H&A and HE segments recognize revenue differently?

H&A recognizes revenue mainly from complete appliance sales, reaching end users via retail and project channels. HE recognizes revenue from TV sales and some software services, linked to display technology, panel costs, and brand premiums. Both serve consumer markets, but product cycles and competitive dynamics differ.

How does the VS division generate revenue?

VS generates revenue through OEM-designated projects: participating in bids for vehicle electronic systems, completing development and validation after winning, and recognizing revenue by shipment volume or project contract as models move to mass production. Revenue timing is tied to auto production/sales, new energy vehicle adoption, and project ramp-up progress.

How do the business models of LG Electronics and LG Display differ?

LG Electronics focuses on home appliances, complete TVs, and vehicle electronic systems, acting as an end-brand and system integrator. LG Display specializes in manufacturing display panels as an upstream supplier. Both are independent listed entities under the LG Group with separate stock codes and financial statements.

Why analyze LG Electronics’ business model by division?

Each division has different downstream clients, cycle drivers, and revenue recognition schedules: H&A is driven by consumer cycles, HE by display competition and tech upgrades, and VS by automotive contracts and production progress. Segment-based analysis prevents oversimplification of overall performance.

What should be verified before trading LG Electronics stock?

On the business side, verify the revenue structure of all three divisions, key segment drivers, and group entity boundaries. On the trading side, confirm the listed entity, Korean market access, fee structures, and order types. Separate your fundamental analysis from platform operations.