TeraWulf (WULF) stock represents the equity pricing logic of a Bitcoin mining company, where performance is determined by more than just the price of Bitcoin. The core of WULF stock lies in how the company integrates electricity, mining machines, and operations to create a system that consistently generates output. By first understanding the Panoramic Definition of TeraWulf (WULF) Stock, it's easier to analyze the revenue and cost cycle and appreciate the operational flexibility of this stock.

What is the essence of WULF’s business model?

WULF’s business model transforms available electricity and mining machine hashrate into measurable Bitcoin output, which is then converted into corporate cash flow. Unlike traditional manufacturing, the core product here isn't physical inventory, but “effective hashrate contribution per unit time.” Within this structure, the company’s value hinges on three factors: the sustainability of its hashrate scale, the controllability of unit costs, and whether its capital structure supports expansion.

Bitcoin mining companies typically face high fixed investments alongside significant operational volatility. Building mining farms, acquiring equipment, and securing electricity all require upfront capital, while revenue streams are influenced by block rewards and shifts in network competition. As a result, WULF’s operational focus is not on maximizing output at a single moment, but on maintaining a dynamic balance among output, costs, and cash.

From a shareholder’s perspective, the stock reflects not just the quantity of mining machines, but the company’s ability to convert electricity into output, and output into reinvestable cash. Hashrate sets the capacity ceiling, while electricity and financing determine whether operations can be sustained.

How is revenue generated—from hashrate to cash flow?

WULF’s revenue is generated through four key stages: hashrate online, block reward distribution, Bitcoin valuation, and financial recognition. The online rate of hashrate determines the company’s ability to participate in network ledger competition, while block rewards and transaction trading fees are the primary income sources for miners. At the financial level, revenue is recognized based on coin-holding strategies, settlement arrangements, and accounting practices.

Rising Bitcoin prices typically boost the nominal value of output, but this doesn’t automatically translate to higher profits. If total network hashrate increases and mining difficulty rises, the output allocated to each unit of hashrate may decrease. WULF’s revenue assessment must therefore consider both price and network variables—not just the price trend.

There’s also a distinction between the “output rhythm” and the “realization rhythm.” Continuous mining machine operation generates output, but the company may choose to liquidate immediately, hold coins periodically, or use the output to repay debt. The realization rhythm can alter the short-term appearance of financial statements, but the long-term cycle remains: output value must still cover operational and capital costs.

How is the cost structure organized—electricity, equipment, and financing?

WULF’s costs are divided into variable costs, semi-fixed costs, and capital costs. Electricity spending is the key variable cost, directly linked to machine operating hours and electricity contract terms. Equipment depreciation and maintenance are semi-fixed costs, impacted by mining machine efficiency and failure rates. Capital expenditures and financing costs are long-term constraints, affecting the pace of expansion and resilience to market cycles.

| Cost Level |

Main Components |

Impact Mechanism |

Operational Significance |

| Variable Cost |

Electricity purchase, grid fees |

Linked to operating hours and electricity terms |

Determines unit output cash cost |

| Semi-Fixed Cost |

Equipment depreciation, O&M |

Linked to machine efficiency and failure rates |

Determines mid-term cost curve slope |

| Capital Cost |

New machine investment, interest |

Linked to expansion plans and funding conditions |

Determines expansion ceiling and resilience |

This table highlights that mining companies are not simply passive to price swings. By optimizing their energy mix, improving equipment efficiency, and managing capital expenditures, companies can create different cost structures under similar market conditions. This is a key reason for valuation differences between WULF and its peers.

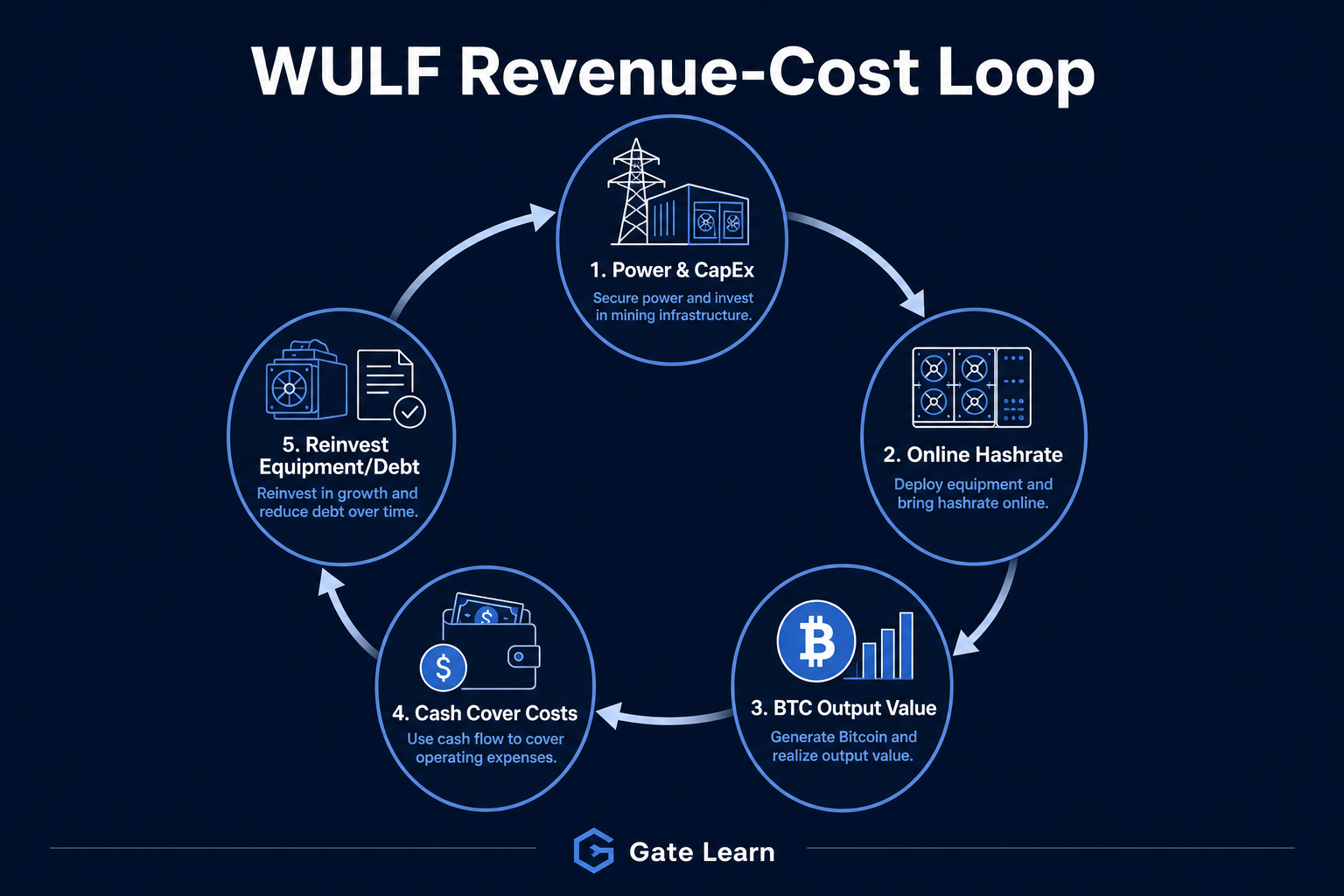

Figure 1. Schematic of TeraWulf (WULF) operating cycle: reinvesting hashrate after covering costs with revenue.

Figure 1. Schematic of TeraWulf (WULF) operating cycle: reinvesting hashrate after covering costs with revenue.

The sustainability of the revenue-cost cycle depends on whether the output value per unit of hashrate consistently exceeds the total cost per unit. If mining output continually covers electricity, operations, and financing costs, the company maintains a self-sustaining cash flow. If coverage declines, the company may rely on external financing for expansion, reducing the cycle’s stability.

WULF’s operational cycle operates as an “input-output-reinvestment” loop: the company invests in electricity and equipment to generate output, which is then used for upgrades, debt management, and hashrate optimization. The more stable this cycle, the better the company can maintain continuous production through market fluctuations. If the cycle weakens, financial pressures intensify during downturns.

Evaluating the cycle requires distinguishing “accounting profit” from “cash stress capacity.” Depreciation impacts accounting profit, but what truly disrupts reinvestment is rising cash costs, debt maturities, and unsynchronized equipment upgrades.

How does the Bitcoin cycle affect operational efficiency?

The Bitcoin cycle impacts both revenue and costs. Revenue is influenced by price and block reward changes, while costs are affected by network competition, equipment upgrades, and financing conditions. After a halving event, rewards per unit of hashrate decrease, making energy efficiency and cost control even more critical and often reshuffling operational efficiency rankings. For further insight, see WULF and the Bitcoin Cycle, Halving, and Hashrate Relationship.

Cycle analysis focuses not on single market moves, but on identifying a company’s survival threshold at different stages. Lower unit costs and a stable financing structure allow the cycle to continue even in downturns, while excessive reliance on high prices increases vulnerability. If hashrate expansion isn’t matched by lower unit costs, capacity built in upswings can become a heavier cash burden in downturns.

What core indicators matter for evaluating WULF’s business model?

A robust indicator framework reduces reliance on single narratives. Key metrics include:

- Operational efficiency: online hashrate, mining machine energy efficiency, and unit electricity output

- Cost resilience: average electricity price, unit output cost, and depreciation pressure

- Financial safety: cash reserves, debt maturities, and interest coverage ratio

These indicators should be evaluated collectively. If hashrate grows alongside high costs, operational quality may not improve; if costs drop but hashrate declines, it may simply reflect contraction. Comparing metrics within the same time frame gives a clearer view of cycle improvement. Also consider “reinvestment coverage”—whether operating cash flow, after debt and maintenance capex, is sufficient to support equipment upgrades.

What are the advantages, risks, and limitations of the business model?

The business model’s strength is its reliance on quantifiable variables—electricity price, hashrate, and output efficiency are all trackable. Its limitation is heavy dependence on external network rules and energy conditions, which companies cannot fully control. Risks center on price volatility, rising mining difficulty, energy cost fluctuations, and tightening financing, as detailed in WULF Risks, Market Cycles, and Liquidity Factors.

For WULF, operational resilience depends not on expansion speed, but on matching expansion with cost control and capital structure. Overinvestment relative to cash flow can break the cycle; synchronized investment and efficiency gains promote stability. Advantages, limitations, and risks should be stated separately and are not investment advice.

Summary

TeraWulf (WULF) stock’s business model is a cyclical system: “hashrate for output, output covers costs, cash reinvested in hashrate.” Revenue and costs are influenced by multiple variables, so analysis should consider operational efficiency, cost structure, and financial constraints together. Focusing on cycle stability provides a more comprehensive view of mining company performance than price trends alone.

FAQ

Does WULF’s revenue depend only on Bitcoin’s price?

No. While Bitcoin’s price affects nominal output, network difficulty, online hashrate, and equipment efficiency all impact unit output. Revenue assessment requires analyzing price and network competition together.

What is the most critical cost for TeraWulf?

Electricity is typically the most important cash cost, as mining machines continuously consume power. The structure of electricity contracts and energy procurement stability significantly affect unit output cost and operational flexibility.

Why do mining companies with similar profiles perform differently?

Differences mainly arise from energy structure, equipment efficiency, depreciation pressure, and financing terms. Even facing the same Bitcoin cycle, companies can have very different cost curves and cash flow resilience.

How can you assess the robustness of WULF’s revenue-cost cycle?

Check if unit hashrate output consistently covers total unit cost, and monitor cash reserves and debt maturities. If operating cash flow supports equipment upgrades and necessary expansion, the cycle is generally robust.

What are the main risks in WULF’s business model?

Key risks include falling Bitcoin prices, rising mining difficulty, increasing electricity costs, and tightening financing conditions. These factors affect profit margins and cash flow, impacting operational stability and valuation expectations.