AIG (American International Group), a globally recognized insurance giant, generates revenue from both insurance product sales and the returns on its massive investment portfolio. For AIG, balancing underwriting profit with investment returns while managing claims risk and capital costs is critical to the long-term stability of its business model.

Understanding AIG’s revenue structure and profit logic helps investors grasp how the insurance industry operates and why risk management is a core competitive advantage for insurers.

AIG Stock Basics

AIG is the stock ticker for American International Group, listed on the New York Stock Exchange (NYSE). Headquartered in New York City, it is one of the largest insurance and risk management groups globally.

Classification-wise, AIG falls under the insurance sector within financial services, with core operations in property insurance, liability insurance, commercial insurance, and professional risk management. Unlike traditional banks that rely on deposit and loan spreads, insurers generate profits primarily from premiums and investment returns.

AIG serves large corporations, small and midsize enterprises, and select individual clients across multiple countries. Because insurance is closely tied to economic activity, AIG’s performance is influenced by business investment, corporate conditions, and evolving global risks.

For insurance-focused investors, AIG represents both a major insurer and a bellwether for the global corporate risk management market.

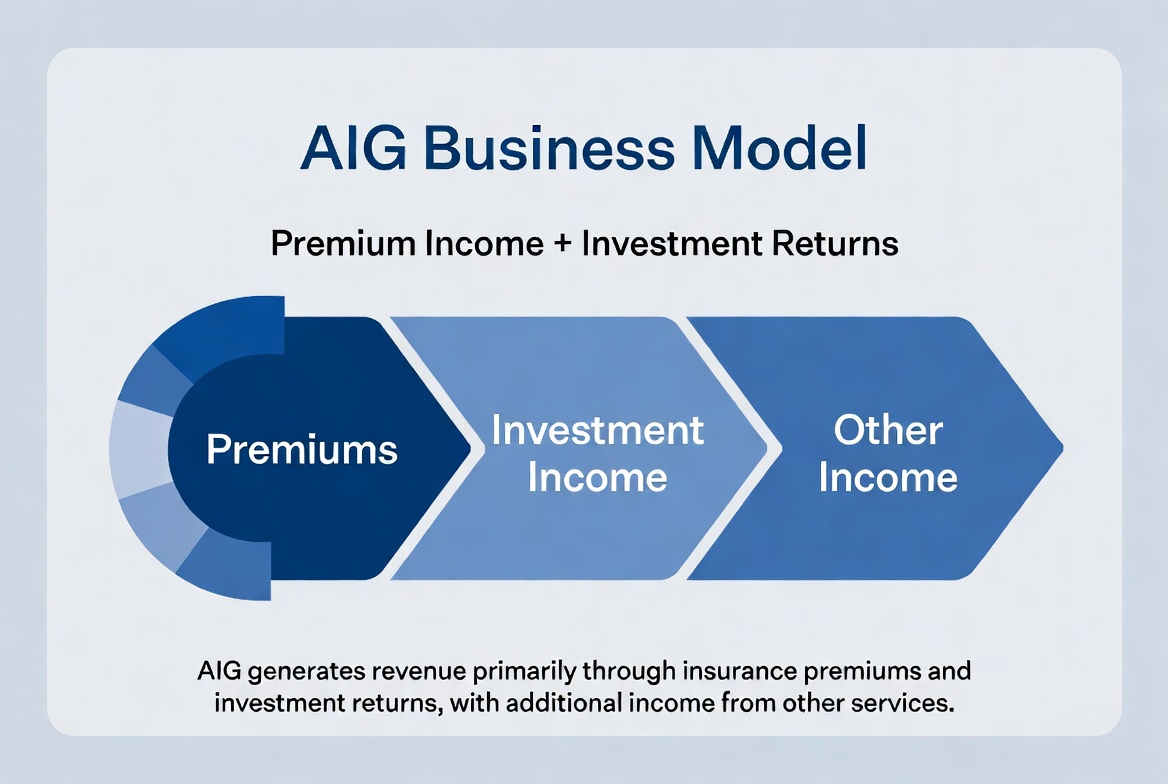

AIG’s Revenue Sources

AIG’s revenue comes from two main streams: underwriting income and investment income.

First, insurance product sales. Clients pay premiums, and AIG underwrites based on risk assessment. If claims and operating costs remain below premiums collected, the company earns underwriting profit.

Second, investment income. Since claims are not paid immediately, premiums create a large pool of investable funds. These funds are typically allocated to bonds, cash instruments, and other stable assets, generating steady returns.

For large insurers, investment income can significantly affect overall profitability. Thus, insurance companies act as both operators and asset managers, and AIG is a prime example of this dual model.

Below is a simplified breakdown of AIG’s revenue sources:

| Revenue Source |

Main Components |

| Premium Income |

Property, liability, commercial insurance, etc. |

| Underwriting Profit |

Premiums minus claims and operating costs |

| Investment Income |

Returns from bonds, cash, and other assets |

| Other Income |

Risk management and related service fees |

How Property Insurance Generates Revenue

Property insurance is one of AIG’s largest segments and a key premium driver.

It covers buildings, factories, warehouses, equipment, and other assets. Clients pay premiums calculated based on risk level, coverage, and historical losses, and AIG assumes the corresponding claims liability.

The core of this model is risk pricing. Accurate risk assessment and appropriate premium setting allow premiums to exceed claims and costs over time, yielding underwriting profit.

For AIG, property insurance extends beyond ordinary commercial assets to include large industrial facilities, energy projects, and multinational corporate assets. These large-scale policies generate substantial premium income but also demand superior risk management.

As corporate asset bases grow and global risks become more complex, property insurance remains a cornerstone of AIG’s long-term strategy.

How Commercial Insurance Drives Growth

Commercial insurance offers higher premium volumes and more complex risk structures than personal insurance, making it a vital growth driver for AIG.

Coverage includes liability insurance, cybersecurity insurance, professional liability, aviation insurance, and customized industry solutions. Businesses rely on these products to mitigate operational risks.

For example, a large manufacturer may need property, product liability, and employee coverage, while a tech firm prioritizes cybersecurity and data protection. These needs fuel the commercial insurance market’s expansion.

AIG’s long-standing focus on corporate clients has built strong capabilities in risk assessment, underwriting, and global service networks. Rising corporate risk management demands and increasing global business activity make commercial insurance a key revenue growth engine for AIG.

Why the Investment Portfolio Affects Profitability

Unlike many service companies, an insurer’s profitability depends not only on sales but also on investment management acumen.

After collecting premiums, insurers hold a pool of funds for future claims—known as “insurance float.” These funds are invested in bonds, Treasuries, and other low-risk assets to generate additional returns.

Given AIG’s massive portfolio size, interest rates and market conditions directly impact earnings. Higher rates boost returns on new investments, while low rates can compress yields.

Thus, investment management is integral to the insurance business. AIG must excel at both insurance operations and maintaining a sound investment strategy to balance long-term returns with capital safety.

Why Risk Control Underpins Long-Term Stability

Risk control is a core competitive advantage in insurance. Even with substantial premium income, poor claims management can pressure profits.

For AIG, risk control permeates every stage—from pre-underwriting risk assessment to policy pricing, claims management, and capital allocation.

For instance, rising natural disaster frequency can increase property insurance claims; more cyberattacks raise cybersecurity payout costs; global economic swings affect both insurance demand and investment returns. Insurers must continuously refine risk models and underwriting strategies.

Over the long term, the insurance industry competes on risk management, not just sales volume. Those who assess risks more accurately and control claims costs more effectively are better positioned for stable profitability. This is a key source of AIG’s enduring competitive strength.

Summary

AIG’s business model rests on a dual foundation: premium income and investment returns. Through property insurance, commercial insurance, and professional risk management, the company generates steady premiums. By investing insurance float, it creates additional investment income. Meanwhile, risk control determines underwriting profit and long-term stability. For AIG, insurance is not merely a risk-transfer business but a system built around risk assessment, capital management, and long-term asset operations.

FAQ

How does AIG primarily make money?

AIG earns income from premium collections, underwriting profit, and investment returns.

What is an insurance company’s premium income?

Premium income is the fee clients pay for insurance coverage. It is a primary revenue source for insurers.

Why is commercial insurance important for AIG?

Commercial insurance typically involves higher premium volumes and long-term client relationships, making it a core growth segment for AIG.

Where does an insurance company’s investment income come from?

It comes from returns on bonds, government securities, cash management tools, and other investment assets.

What is insurance float?

Insurance float refers to the pool of funds an insurer holds between collecting premiums and paying claims, which can be invested.

Why does risk control affect an insurance company’s profitability?

If claims costs consistently exceed premium income, profitability declines. Hence, risk control is essential for sustainable insurance operations.