aUSD is a USD-denominated debt token issued by Arrow Finance on Robinhood Chain, backed by overcollateralized assets within the Vault and redeemable at face value for underlying assets through the Redemption Router. Unlike pegs that rely on centralized reserve commitments, aUSD’s price stability is maintained by on-chain redemption arbitrage and robust collateral backing.

Arrow Finance (ARROW) has developed a native overcollateralized CDP on Robinhood Chain, enabling users to deposit collateral and mint aUSD while maintaining exposure to the underlying asset’s price movement. Arrow Finance is unrelated to the Arrow Markets options protocol on Avalanche—be sure to verify protocol identity and contract addresses before participating.

The redemption router channels aUSD redemption pressure toward the riskiest debt positions in the system. Oracles provide real-time collateral valuations, and the redemption fee dynamically regulates arbitrage activity—together, these form the core triangle of the aUSD peg mechanism.

What Is aUSD and What Role Does It Play in Arrow Finance?

aUSD is the core debt token of Arrow Finance, recording USD-denominated liabilities within the Vault. When the health factor exceeds 1, the collateral value is greater than the debt plus fees, providing genuine asset backing for aUSD. Users mint aUSD by depositing collateral and, upon redemption, receive the Vault’s underlying assets (such as USDC, WETH, or tokenized stocks), rather than a single-asset reserve pool. aUSD serves as both a debt accounting unit and a stable value medium.

| Dimension |

aUSD (CDP Debt Token) |

Fiat Reserve Stablecoin |

| Issuance |

Overcollateralized minting via Vault |

Minting by depositing reserves |

| Redemption Target |

Underlying collateral (as routed) |

Fixed reserve asset |

| Peg Mechanism |

Face value redemption + arbitrage |

1:1 reserve redemption |

| Price Risk Source |

Collateral volatility, oracle risk, redemption fee |

Reserve transparency, custody risk |

This table summarizes the structural differences between these stablecoin types. aUSD’s stability is grounded in enforceable on-chain redemption rights, not off-chain bank promises. Opening a Vault to mint aUSD details the process from collateral deposit to debt creation. The supply of aUSD is determined at minting, while redemption dynamics set the direction of peg pressure.

How Does Face Value Redemption Work? How Does Arbitrage Support the Peg?

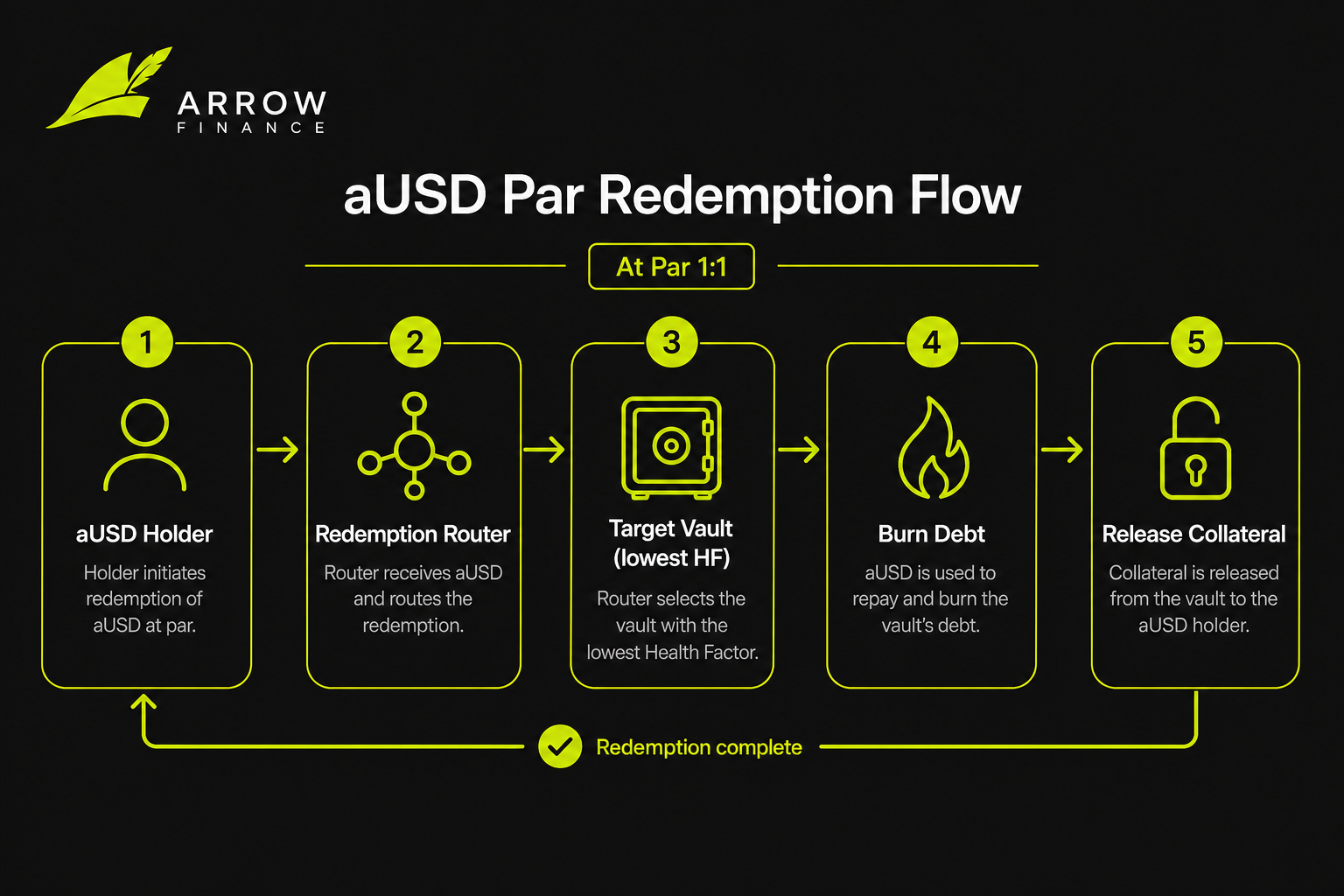

Face value redemption allows aUSD holders to exchange tokens at a 1:1 nominal value for underlying collateral (after deducting the redemption fee). When aUSD trades below $1 on secondary markets, arbitrageurs buy discounted tokens and redeem collateral through the Redemption Router for profit, driving the price back up. If aUSD trades above $1, users mint aUSD from the Vault and sell it, increasing supply and reducing the premium.

This mechanism differs from MakerDAO DAI’s PSM, as Arrow Finance routes redemptions to the Vault with the lowest health factor, rather than a single liquidity pool. The redemption flow is: submit aUSD → router selects target Vault → debt is burned → collateral is released. The type of asset received depends on the underlying collateral of the Vault selected.

Figure 1. aUSD face value redemption flow: holder submits aUSD, routed by the Redemption Router to the target Vault, which releases underlying collateral at face value.

Figure 1. aUSD face value redemption flow: holder submits aUSD, routed by the Redemption Router to the target Vault, which releases underlying collateral at face value.

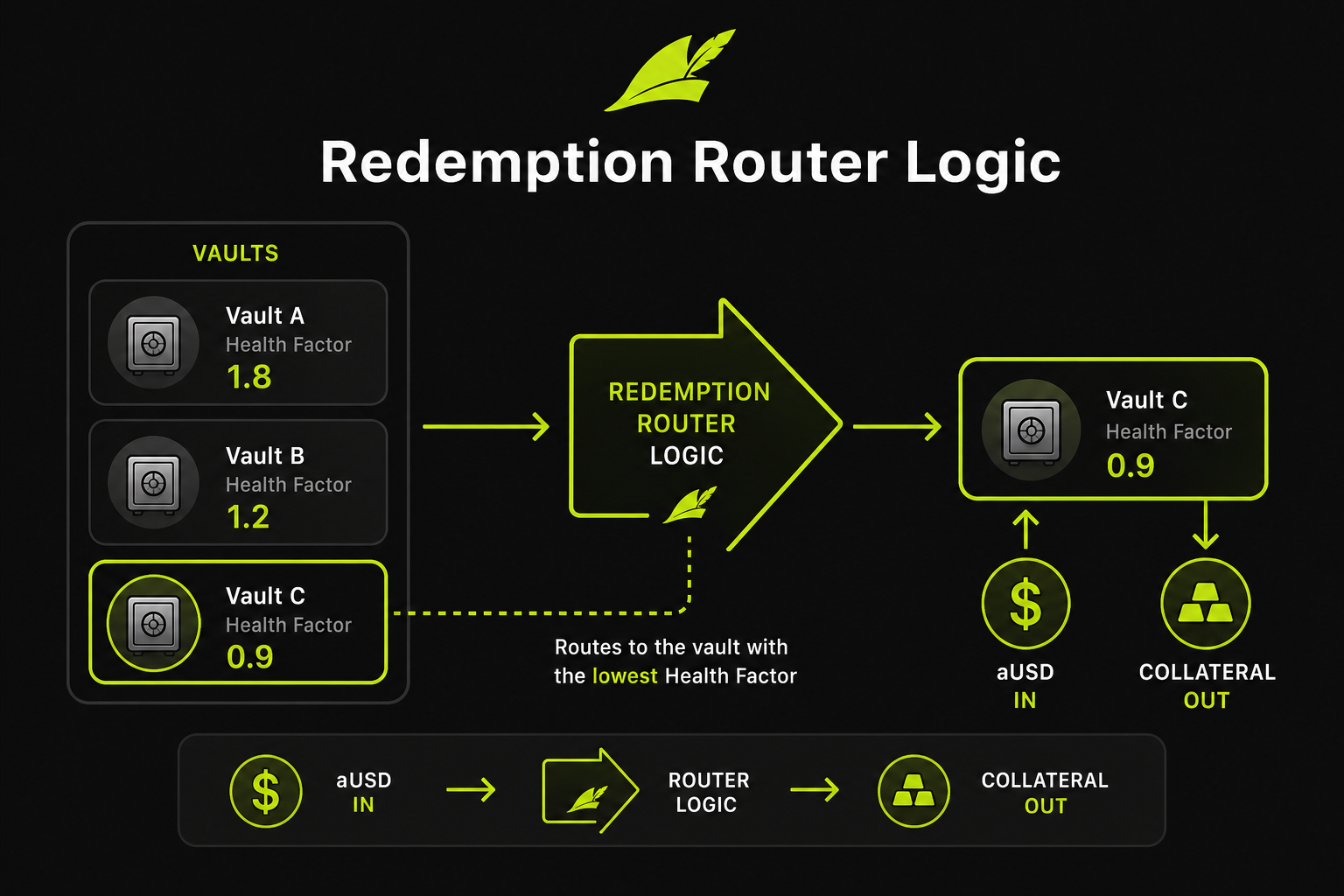

How Does the Redemption Router’s Routing Logic Operate?

The Redemption Router assigns each aUSD redemption to the Vault with the lowest Health Factor, which measures the safety margin of collateral relative to debt plus fees—the lower the factor, the higher the risk. Redeeming aUSD from high-risk Vaults burns their debt and releases collateral, effectively deleveraging those positions and targeting the riskiest debt.

Routing is sequential, prioritizing Vaults from lowest to highest HF. The redeemer receives the underlying asset of each targeted Vault, with the redeemable amount limited by the Vault’s outstanding debt. The redemption fee is deducted from the collateral. If the lowest HF Vault lacks sufficient debt, routing continues to the next lowest HF Vault until the redemption is fulfilled or system capacity is reached. Vault holders can prepay debt or add collateral to avoid being targeted.

Figure 2. Redemption Router routing logic: redemption requests are directed to Vaults with the lowest Health Factor, targeting the highest-risk debt first.

Figure 2. Redemption Router routing logic: redemption requests are directed to Vaults with the lowest Health Factor, targeting the highest-risk debt first.

How Are Collateral Prices Determined by Oracles? How Do Price Deviations Affect the Peg?

aUSD’s peg relies on oracles that provide USD valuations for collateral. Arrow Finance uses a dual-layer oracle system: Chainlink price feeds for crypto assets and stablecoins, and a dedicated NAV (Net Asset Value) oracle for tokenized stocks, synchronized with Robinhood Chain’s stock markets.

Crypto asset oracles operate in continuous markets, with deviations typically caused by brief delays or extreme volatility. Tokenized stock oracles must handle market closures: prices are frozen or buffers widened to prevent outdated NAV-based minting or unwarranted liquidations. Near market close, borrowing may be suspended and liquidation buffers increased.

| Collateral Type |

Oracle Source |

Special Handling |

| Stablecoins / Major Crypto |

Chainlink |

Standard feed updates |

| Liquid Staking Tokens |

Chainlink |

Includes depeg risk |

| Primary Tokenized Stocks |

Dedicated NAV oracle |

Price frozen during closure |

| Secondary Tokenized Stocks |

Dedicated NAV oracle |

More conservative buffer parameters |

If collateral is overvalued, Vaults can mint more aUSD than is truly backed, weakening redemption support. If undervalued, health factors appear artificially low, making Vaults unnecessarily subject to liquidation or redemption. ARROW governance can adjust oracle sources and buffer parameters as needed.

How Does the Redemption Fee Affect the Peg? How Does It Differ from Other Fees?

Arrow Finance charges a variable redemption fee of 0.25%–2% on aUSD redemptions, deducted from collateral received and allocated to the Surplus Buffer. The redemption fee acts as a peg moderator: higher rates reduce arbitrage incentives and slow redemptions, easing pressure on low HF Vaults; lower rates enhance arbitrage and accelerate peg convergence.

The stability fee (0.5%–4% APR) accrues over time on outstanding debt, impacting the health factor. Liquidation penalties (10%–13%) incentivize the Stability Pool and reserve accumulation. Only the redemption fee directly affects the redemption path and the speed at which the market price returns to peg.

| Fee Type |

Rate Range |

Peg Impact |

| Redemption Fee |

0.25%–2% |

Regulates redemption arbitrage incentives and pace |

| Stability Fee |

0.5%–4% APR |

Affects debt growth and Vault health factor |

| Liquidation Penalty |

10%–13% |

Indirectly supports the peg by maintaining system solvency |

If market discounts exceed 2%, arbitrage remains profitable even at the highest redemption fee. Governance must balance peg responsiveness with the impact of redemptions on Vault holders when adjusting fee parameters.

In What Scenarios Might the Peg Fail?

Face value redemption and permissionless arbitrage are the primary mechanisms supporting the aUSD peg, but under extreme conditions, temporary deviations from $1 can occur. The following are structural risks, not price forecasts.

If collateral prices crash system-wide, multiple Vaults’ health factors may drop simultaneously, and redeemers could receive highly volatile assets, with discounts reflecting concerns about collateral quality. The Stability Pool and redistribution process handle liquidations, and the Surplus Buffer absorbs bad debt; if losses exceed reserves, peg support is weakened.

During tokenized stock market closures, NAV freezes but debt remains. Sharp volatility before closure or price gaps after reopening can make many Vaults subject to liquidation at once, increasing redemption pressure. Smart contract bugs, oracle manipulation, or debt ceiling breaches can all undermine overcollateralization. If liquidity is insufficient, arbitrageurs may struggle to liquidate collateral, prolonging market discounts.

Summary

The aUSD peg is underpinned by overcollateralization, face value redemption, and permissionless arbitrage. The Redemption Router targets Vaults with the lowest health factor, focusing pressure on the riskiest debts. Chainlink and NAV oracles provide real-time collateral valuations. The redemption fee (0.25%–2%) regulates arbitrage activity. The Stability Pool, liquidation penalties, and Surplus Buffer form a robust backstop, creating a closed-loop peg mechanism.

Maintaining the aUSD peg requires close attention to arbitrage margins, Vault health factor distribution, and oracle data quality—any weakness can amplify price deviations.

FAQ

What is aUSD?

aUSD is a USD-denominated debt token issued by Arrow Finance on Robinhood Chain, backed by overcollateralized assets in the Vault. Users deposit approved collateral to mint aUSD, which can be redeemed at face value for underlying assets via the Redemption Router. It should not be confused with Arrow Markets on Avalanche.

How does aUSD maintain its $1 peg?

The peg is maintained through face value redemption and permissionless arbitrage. When aUSD trades below $1, arbitrageurs buy discounted tokens and redeem collateral through the Redemption Router, pushing the price back up. The Redemption Router prioritizes Vaults with the lowest health factor, while Chainlink and NAV oracles provide collateral valuations. The redemption fee (0.25%–2%) regulates redemption pace.

What is Arrow Finance?

Arrow Finance is the first native overcollateralized CDP protocol for tokenized assets on Robinhood Chain. Users deposit crypto assets, stablecoins, or tokenized stocks as collateral to mint aUSD in Vaults, retaining upside exposure to the underlying assets. ARROW is a fixed-supply governance token used to adjust risk parameters and fee curves.

How does the Redemption Router work?

The Redemption Router directs aUSD redemption requests to the Vault with the lowest health factor. Redemption burns that Vault’s aUSD debt and releases its collateral, effectively deleveraging high-risk Vaults. If the lowest HF Vault lacks sufficient debt, routing continues to the next lowest HF Vault until the redemption is complete.

How does the redemption fee affect aUSD price?

The redemption fee is deducted from collateral received, with the rate (0.25%–2%) set by governance. Higher rates reduce arbitrage incentives and slow redemptions; lower rates increase arbitrage and accelerate peg restoration. If the market discount exceeds the combined redemption fee and transaction costs, arbitrage remains profitable and drives the price toward $1.

What happens if the aUSD peg fails?

Short-term price deviations may occur due to collateral crashes, oracle delays, NAV freezes during market closures, or liquidity shortages. The Stability Pool and Surplus Buffer backstop liquidations and bad debt. If systemic losses exceed reserves, the support for face value redemption weakens and discounts may persist. Mechanism risks should be independently evaluated based on collateral composition and governance parameters.