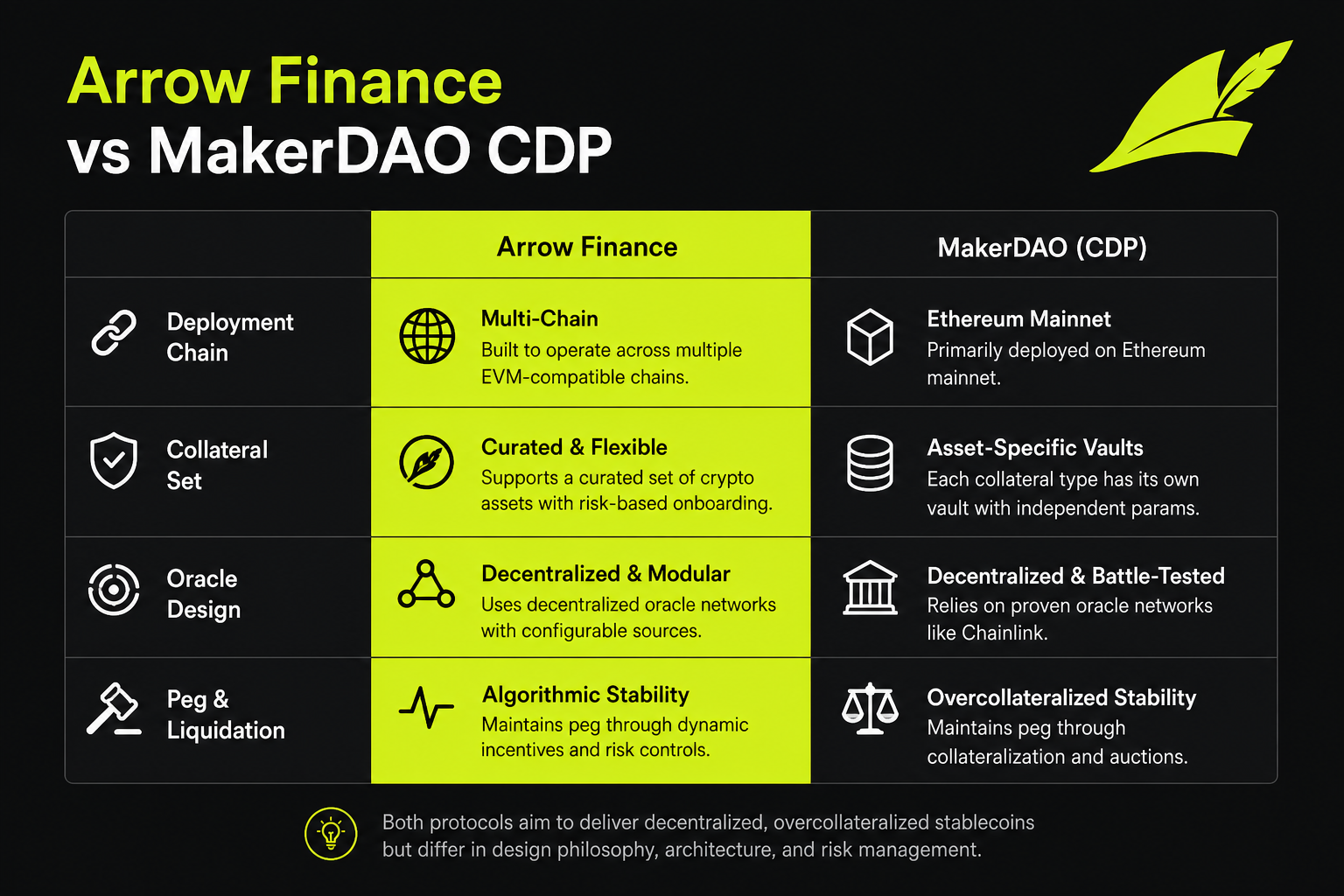

The primary distinctions between Arrow Finance and established CDPs like MakerDAO center on their deployment chains, eligible collateral sets, and stablecoin peg mechanisms. Arrow Finance is a native, over-collateralized CDP protocol built on Robinhood Chain, offering direct support for tokenized stocks and on-chain RWAs. In contrast, MakerDAO is the longest-running CDP protocol on Ethereum, minting DAI through crypto collateral and maintaining its peg via mature modules such as the PSM and DSR. Note that Arrow Finance is unrelated to Arrow Markets, an options protocol on Avalanche.

For a complete overview of Arrow Finance (ARROW), Arrow Finance allows users to mint aUSD without liquidating underlying assets, while MakerDAO serves as the foundational decentralized stablecoin infrastructure for Ethereum DeFi. Below, we compare protocol definitions, collateral, chain positioning, liquidation and peg mechanisms, and key limitations.

Figure 1. Matrix comparing Arrow Finance and MakerDAO by deployment chain, debt token, collateral scope, oracle, and liquidation/peg mechanisms.

Figure 1. Matrix comparing Arrow Finance and MakerDAO by deployment chain, debt token, collateral scope, oracle, and liquidation/peg mechanisms.

What Is Arrow Finance?

Arrow Finance is the first native over-collateralized CDP protocol on Robinhood Chain designed for tokenized assets, with aUSD as its core debt token. Users deposit approved collateral and mint aUSD in a single-user, single-collateral, single-debt Vault, up to the LTV ceiling. Debt is tracked as ERC-20, and collateral is released upon repayment of principal plus stability fee.

Core protocol components include the Vault Manager, Redemption Router, Stability Pool, and Surplus Buffer. ARROW token holders govern LTV and fee rates. Arrow Finance is distinct from Arrow Markets on Avalanche.

What Is MakerDAO?

MakerDAO is the oldest decentralized over-collateralized CDP protocol on Ethereum mainnet, with DAI as its principal debt token—a stablecoin pegged to $1 and backed by over-collateralized Vaults. Users deposit ETH, WBTC, stablecoins, and other assets into Maker Vaults (formerly CDPs) and mint DAI based on collateralization ratios. Collateral is released after DAI and stability fee repayment.

MKR holders govern risk parameters. The peg is maintained via the Peg Stability Module (PSM) and DAI Savings Rate (DSR). MakerDAO represents the classic Ethereum-native, crypto asset-focused CDP model, and does not natively support tokenized stocks as collateral.

How Do the Collateral Sets Differ?

Collateral scope is one of the most significant structural differences between Arrow Finance and MakerDAO. Arrow Finance supports stablecoins, liquid staking tokens, major cryptocurrencies, primary and secondary tokenized stocks, and on-chain ETFs and RWAs. MakerDAO’s core collateral includes ETH, WBTC, stablecoins, and other crypto assets approved through governance; RWA integration requires additional compliance and custodial arrangements, and is not a native protocol feature.

| Collateral Type |

Arrow Finance |

MakerDAO (Typical) |

| Stablecoins |

USDC, sUSDe, etc. |

USDC, DAI, and other governance-approved assets |

| Liquid Staking |

wstETH, weETH |

Select LSTs via governance |

| Major Cryptos |

WETH, WBTC |

ETH, WBTC, etc. |

| Tokenized Stocks |

Primary ~55% LTV, Secondary ~40% LTV |

Not natively supported |

| ETF & RWA |

On-chain issuance and settlement |

Requires separate RWA module or external structures |

| Capital Efficiency |

USDC up to ~90% LTV |

Varies by asset; typically lower for ETH |

Arrow Finance integrates tokenized stocks into its CDP framework; MakerDAO offers deeper crypto collateralization. For detailed parameters, see Collateral LTV Parameters. Tokenized stock collateral introduces trading hour and NAV oracle constraints, so Arrow Finance employs more conservative LTVs and wider liquidation buffers.

How Do Chain Environments and RWA Positioning Differ?

Arrow Finance is deployed on Robinhood Chain, sharing an environment with tokenized stock and ETF issuers, enabling positions with stock assets without cross-chain operations. MakerDAO is deployed on Ethereum mainnet, offering deep DAI composability, but collateralizing tokenized stocks typically requires extra issuance and compliance steps, outside the default Vault scope.

Chain selection determines oracle architecture: Arrow Finance uses dedicated NAV oracles for stocks, allowing price freezing or wider buffers during market closures; MakerDAO primarily relies on Chainlink for crypto and stablecoins and does not address stock trading session logic.

How Do Liquidation and Stablecoin Mechanisms Compare?

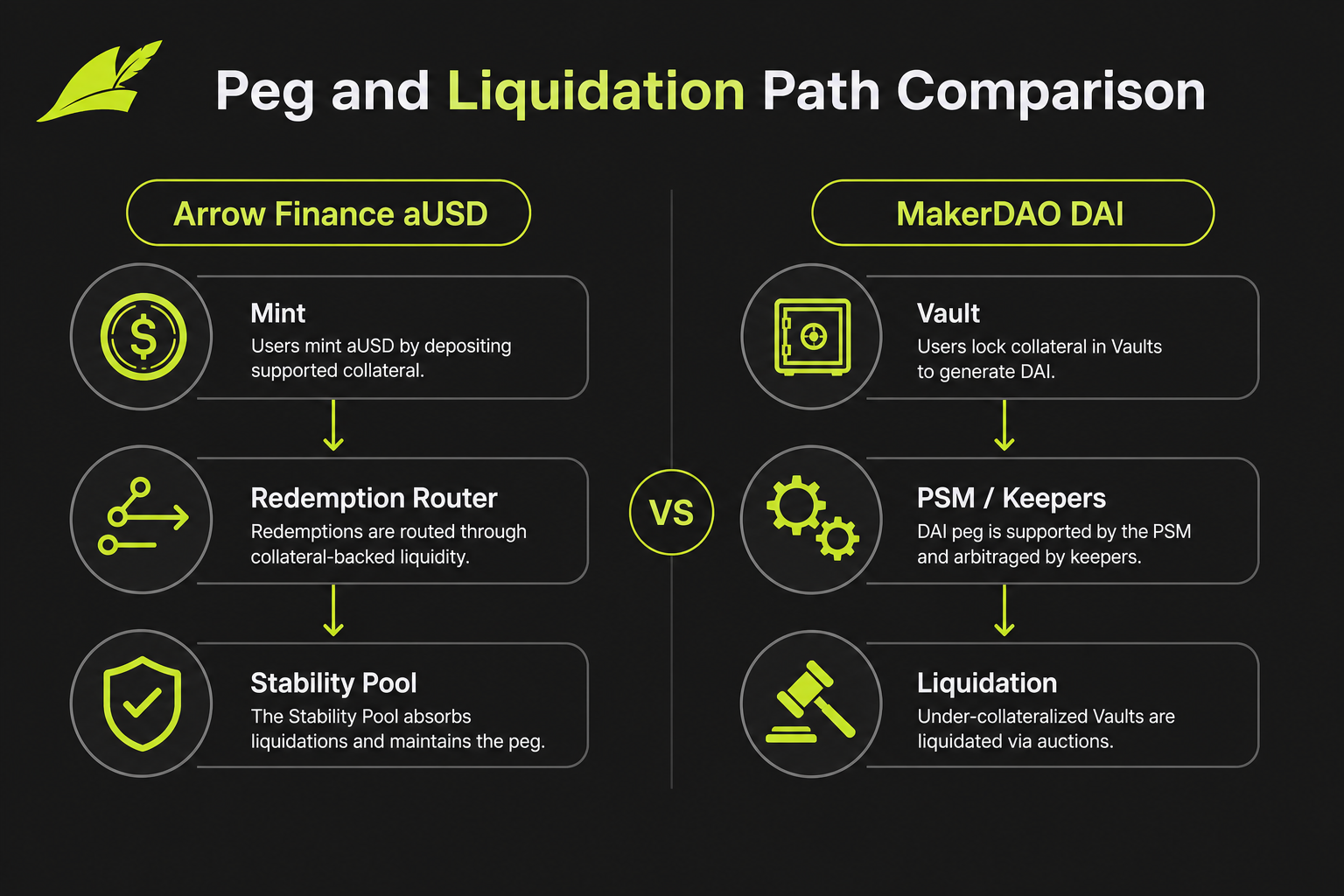

Arrow Finance’s aUSD is redeemed for collateral at face value via the Redemption Router, which prioritizes Vaults with the lowest health factor. If the health factor drops below 1, the Stability Pool burns debt and acquires collateral at a discount, with penalties around 10%–13%. MakerDAO’s DAI relies on the PSM and reserves like USDC to balance supply and demand, with the DSR influencing holding incentives; liquidation occurs via auction or a unified liquidation engine.

| Mechanism Module |

Arrow Finance (aUSD) |

MakerDAO (DAI) |

| Peg Core |

Redemption Router (face-value redemption) |

PSM + market arbitrage + DSR |

| Liquidation Execution |

Unified Stability Pool |

Auction / liquidation engine |

| System Reserves |

Surplus Buffer |

Surplus buffer and multiple asset reserves |

| Redemption/Exchange Fee |

~0.25%–2% |

PSM fees vary by asset |

| Interest |

Stability fee 0.5%–4% APR |

Stability fee + DSR |

The Redemption Router allocates debt-side pressure; the PSM manages reserve-side liquidity. For more, see aUSD Peg and Redemption Router.

Core Differences at a Glance

The table below summarizes the most frequently searched user comparison points for quick reference:

| Comparison Dimension |

Arrow Finance |

MakerDAO |

| Deployment Chain |

Robinhood Chain |

Ethereum mainnet |

| Debt Token |

aUSD |

DAI |

| Core Collateral |

Tokenized stocks + crypto + stablecoins |

Crypto assets + stablecoins |

| RWA Positioning |

Native support for tokenized stocks and ETFs |

RWA not core |

| Peg Mechanism |

Redemption Router |

PSM + DSR |

| Liquidation Path |

Unified Stability Pool |

Auction / liquidation engine |

| Oracle |

Chainlink + stock NAV |

Primarily Chainlink |

| Governance Token |

ARROW |

MKR |

This table highlights differences in chain, assets, tokens, and mechanisms. For tokenized stock-backed loans, Arrow Finance offers a more defined collateral boundary; for DAI in the Ethereum ecosystem, MakerDAO represents a mature, modular solution. For opening positions, see How to Open a Vault and Mint aUSD.

Figure 2. Schematic comparison of aUSD and DAI peg redemption and liquidation pathways.

Figure 2. Schematic comparison of aUSD and DAI peg redemption and liquidation pathways.

What Are the Limitations of This Comparison?

Direct comparisons must clarify their scope. The Ethereum DeFi ecosystem is more mature, while Robinhood Chain and tokenized stock infrastructure are still emerging. Tokenized stock collateral involves trading hour and NAV disclosure constraints, not present in classic MakerDAO Vaults, though DAI and PSM reserves also face evolving regulatory impacts. Redemption Router and PSM serve different adjustment logics; numerical comparisons are for structural reference only. MakerDAO does not represent all CDPs (e.g., Liquity, RAI use different mechanisms). Arrow Finance is unrelated to Avalanche Arrow Markets; always verify protocol identity before participating.

Summary

Both Arrow Finance and MakerDAO are over-collateralized CDPs, but their positioning is fundamentally distinct: Arrow Finance is a native Robinhood Chain protocol, with aUSD as its debt token, incorporating tokenized stocks, ETFs, and RWAs, and relying on the Redemption Router and Stability Pool for its peg. MakerDAO is a classic Ethereum CDP, with DAI at its core, primarily backed by crypto assets and maintaining its peg via the PSM and DSR. Differences are rooted in chain environment, collateral set, and repayment mechanisms—not simply “new vs. old” or “strong vs. weak.” Always independently assess collateral volatility, oracle, liquidation, and smart contract risks before participating in any protocol.

FAQ

What Are the Key Differences Between Arrow Finance and MakerDAO?

There are three main differences: deployment chain (Robinhood Chain vs. Ethereum); collateral scope (Arrow Finance natively supports tokenized stocks and RWAs, MakerDAO is crypto asset-centric); and peg/liquidation mechanisms (aUSD relies on the Redemption Router and Stability Pool, DAI relies on the PSM, DSR, and auction-based liquidation). Both are over-collateralized CDPs but serve different chain environments and asset structures.

What Is Arrow Finance?

Arrow Finance is a native over-collateralized CDP protocol on Robinhood Chain focused on tokenized assets. Users deposit approved collateral to mint aUSD in Vaults. The protocol is non-custodial, debts are tracked as ERC-20, and the ARROW token governs risk parameters. Arrow Finance is unrelated to Arrow Markets on Avalanche.

What Is aUSD?

aUSD is a USD-denominated debt token over-collateralized in Arrow Finance Vaults, redeemable at face value for underlying collateral via the Redemption Router. Minting involves depositing collateral, opening a Vault, and minting up to the LTV limit; interest accrues via the stability fee, and collateral is released upon repayment. Both aUSD and MakerDAO’s DAI are CDP debt tokens, but differ in chain deployment and peg modules.

How Do MakerDAO’s DAI and aUSD Peg Mechanisms Differ?

DAI’s peg relies on the PSM for reserve swaps, market arbitrage, and the DSR to influence holding incentives. aUSD’s peg uses the Redemption Router to direct redemptions to Vaults with the lowest health factor, in conjunction with Chainlink and stock NAV oracles. MakerDAO’s approach emphasizes reserve-side adjustment, while Arrow Finance focuses on debt-side pressure allocation—each tailored to its on-chain and asset environment.

What Else Should Users Consider When Comparing?

Distinguish Arrow Finance (Robinhood Chain CDP) from Arrow Markets on Avalanche (options protocol). Always verify contracts and entry points to guard against impersonation. LTVs and fees are set by protocol governance and may change by vote. Mechanism descriptions do not constitute investment advice; participation requires independent risk assessment.