Coinbase Global, Inc. (NASDAQ: COIN) is a publicly traded US crypto exchange listed on NASDAQ. Its core business model packages trading, custody, and subscription services into a scalable revenue structure. As part of a deep dive into Coinbase (COIN) revenue composition, understanding what drives COIN stock value starts with two key lines: trading revenue and subscription and services revenue.

Coinbase reports its financials in two primary revenue categories: trading revenue, which fluctuates with trading activity, and subscription and services revenue, which includes membership subscriptions, custody fees, blockchain reward sharing, and stablecoin ecosystem participation. The scale and gross margin differences between these two revenue streams directly impact COIN’s exposure to crypto market cycles. COIN vs HOOD compares Coinbase’s trading fee and subscription-driven model with Robinhood’s reliance on payment for order flow and net interest income, helping clarify the sources of COIN’s cyclical sensitivity.

What Is Trading Revenue and How Does It Work?

Trading revenue is Coinbase’s most direct income source, generated from fees paid by retail and institutional clients for buying and selling digital assets. For retail, this covers simple buy/sell and Advanced Trade; for institutions, it includes OTC trades and block matching, with Advanced Trade’s maker/taker tiered fee structure being the most transparent.

The trading revenue model is: “order matching → fee calculation per rules → recognized as trading revenue.” Coinbase does not take directional risk on user trades; revenue depends on notional trading volume, effective fee rates, and transaction frequency. When market activity rises, trading revenue is highly elastic; when markets are quiet, lower trading demand directly compresses this revenue line.

| Trading Scenario |

Main User Segment |

Fee Structure |

Revenue Characteristics |

| Retail Simple Buy/Sell |

Individual investors |

Spread or fixed fee |

Low barrier, high frequency, market-sensitive |

| Advanced Trade |

Active traders |

Maker/taker tiered fees |

Transparent rates, large trades concentrated |

| Institutional OTC |

Funds, corporate treasuries |

Negotiated or volume discounts |

Large ticket sizes, high client loyalty |

This table summarizes the three main trading scenarios. To analyze COIN’s trading revenue, retail activity, pro trader share, and institutional block trades should be examined separately. Trading revenue is highly correlated with crypto price volatility and is the most cyclical part of COIN’s revenue mix.

What’s Included in Subscription and Services Revenue?

Subscription and services revenue consolidates Coinbase’s recurring service fees outside trading, providing a crucial buffer against market cycles. It includes Coinbase One membership fees, blockchain rewards, custody service fees, stablecoin-related income, and developer platform charges.

Coinbase One offers retail users monthly or annual subscriptions, with benefits like lower trading fees and priority support. Blockchain rewards are earned from staking or Earn product revenue sharing, while custody and Prime service fees are included as institutional service subcategories within subscription and services revenue.

| Subscription & Service Segment |

Product |

Fee Logic |

Cycle Sensitivity |

| Coinbase One |

Retail membership |

Fixed monthly/annual fee |

Relatively low |

| Blockchain rewards |

Staking, Earn |

Revenue share by stake and protocol |

Medium |

| Custody services |

Institutional custody |

Fees based on assets under custody |

Low |

| Stablecoin income |

USDC ecosystem |

Share of circulation-based revenue |

Medium |

| Developer platform |

API, Base tools |

Usage or enterprise contracts |

Low to medium |

USDC and Coinbase One further detail the product structure behind subscription and services revenue, spanning stablecoin mechanisms, membership benefits, and institutional custody. Growth in subscription revenue relies more on user base, custody asset stock, and ecosystem adoption than daily trading frequency.

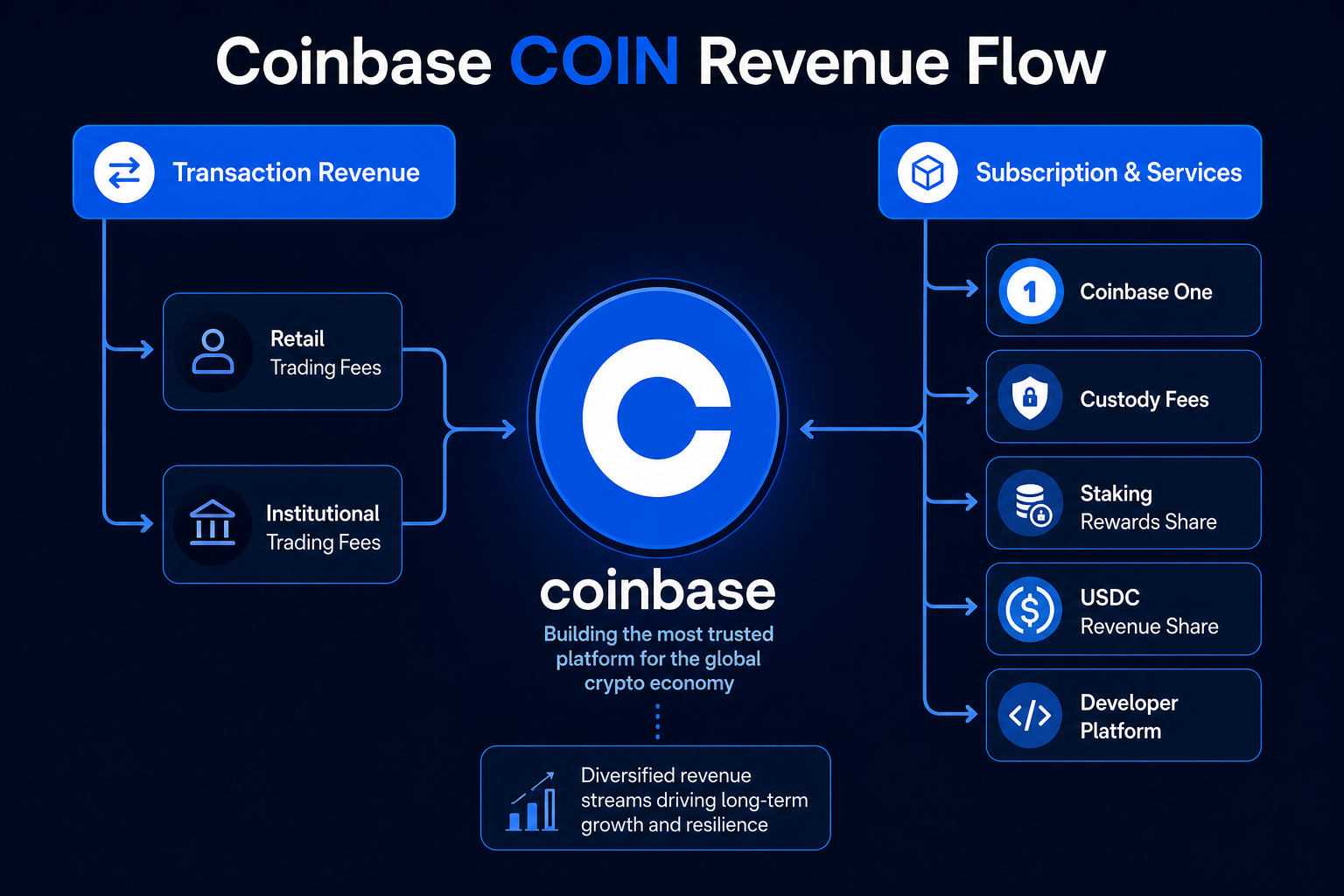

Figure 1. Coinbase dual-track revenue flow: trading revenue from retail and institutional trading fees; subscription and services revenue from Coinbase One, custody, staking rewards, and the USDC ecosystem.

How Are Institutional Prime and Custody Services Priced?

Institutional Prime and custody services are designed for hedge funds, family offices, and corporate treasuries, offering tiered asset custody, OTC liquidity access, and compliance reporting. Custody fees are typically charged annually or quarterly as a percentage of assets under custody (AUC); Prime brokerage adds trading execution and cross-venue liquidity, combining custody and trading-related fees.

The pricing model for custody and Prime emphasizes “asset stock” over “trading frequency.” Institutional clients are charged ongoing fees for storing digital assets; Prime clients incur additional transaction-related fees for large trades, with some counted as trading revenue and others as subscription and services revenue. Assets under custody is a key metric for institutional business health, less directly sensitive to daily market swings than retail trading revenue.

How Sensitive Is the Revenue Structure to Crypto Cycles?

COIN’s revenue structure is most sensitive to crypto market cycles through the link between trading revenue and market activity. In high-volatility periods, trading demand and revenue expand; in low-volatility phases, even with stable subscription and custody balances, trading revenue can contract sharply.

Subscription and services revenue offers some cyclical cushion: fixed Coinbase One fees aren’t tied to daily volume, custody fees are based on asset stock, and USDC circulation and staking participation generate recurring income—fluctuating less than trading fees.

| Revenue Category |

Key Drivers |

Cycle Sensitivity |

Relative Stability |

| Trading revenue |

Volume, fee rates, volatility |

High |

Low |

| Coinbase One |

Subscriber count |

Low |

High |

| Custody & Prime |

Assets under custody |

Medium |

Medium-high |

| Blockchain rewards |

Staking volume, protocol yield |

Medium |

Medium |

| USDC-related income |

Stablecoin circulation |

Medium |

Medium |

This table compares the cyclical exposure of each revenue type by key drivers. Quarterly trading revenue shouldn’t be projected as a long-term trend; instead, both revenue mix and gross margin differences should be considered together. As discussed in COIN Regulation and Compliance, regulatory uncertainty can also indirectly impact revenue structure through trading volume and institutional custody appetite.

Main Revenue Lines at a Glance

Coinbase categorizes revenue in its quarterly reports as trading revenue and subscription and services revenue. The table below presents the main revenue lines alongside corresponding products and key indicators for practical financial analysis.

| Financial Report Line |

Core Product/Service |

Key Metrics |

Notes |

| Trading revenue |

Retail trading, Advanced Trade, Institutional OTC |

Retail trading volume, institutional trading volume, effective fee rate |

Highest cyclicality |

| Subscription & services revenue |

Coinbase One, custody, staking, USDC, API |

Subscriber count, assets under custody, USDC circulation |

Recurring sources |

| Of which: Blockchain rewards |

Staking, Earn |

Assets staked |

Protocol-dependent |

| Of which: Custody fees |

Institutional custody |

Assets Under Custody (AUC) |

Institutional trust metric |

| Of which: Stablecoin income |

USDC ecosystem |

USDC circulation |

Operated with Circle |

When reviewing financials, distinguish total revenue from gross margin by subcategory, and analyze alongside retail and institutional user metrics. The interplay between trading and subscription revenues is a key signal for COIN’s business model evolution.

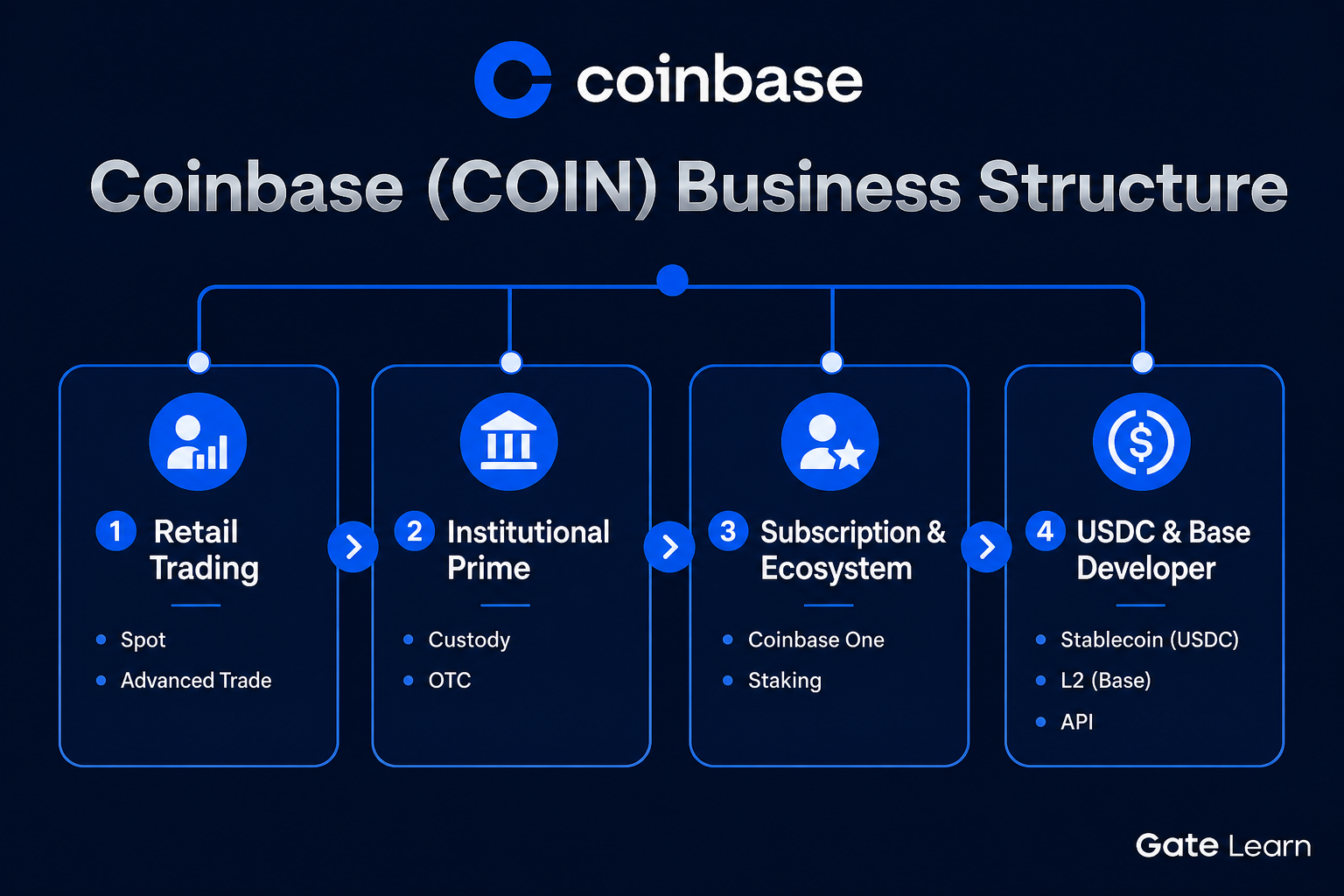

Figure 2. Coinbase revenue structure overview: trading revenue and subscription & services revenue with their key drivers.

Figure 2. Coinbase revenue structure overview: trading revenue and subscription & services revenue with their key drivers.

Summary

Coinbase Global, Inc. (NASDAQ: COIN) operates a dual-track business model: trading revenue from digital asset transaction fees, highly sensitive to crypto market activity; and subscription and services revenue, integrating Coinbase One, custody/Prime, staking rewards, USDC ecosystem, and developer platform fees, providing relatively stable recurring income. Assessing COIN’s revenue drivers requires viewing trading elasticity, custody balances, subscription scale, and regulatory environment within a unified framework.

FAQ

How Does Coinbase Make Money?

Coinbase earns revenue primarily from two sources: trading revenue (fees from retail and institutional crypto transactions) and subscription and services revenue (Coinbase One membership fees, custody and Prime service fees, blockchain reward sharing, USDC-related income, and developer platform fees). Trading revenue is market-sensitive; subscription services offer more stable recurring income.

What Is the COIN Stock Ticker?

COIN is the NASDAQ ticker for Coinbase Global, Inc., the leading US digital asset exchange. Investor relations provide financials and governance disclosures; Gate Stocks users can search and verify the company by COIN.

What Is Coinbase One?

Coinbase One is a paid subscription for retail users, offering lower trading fees, priority support, and enhanced on-chain features. Membership fees are part of subscription and services revenue, making it a key product line for reducing COIN’s reliance on trading revenue.

What’s the Relationship Between USDC and Coinbase?

USDC is issued by Circle, with Coinbase and Circle jointly operating the stablecoin ecosystem and sharing revenue from USDC circulation. USDC-related revenue is included in subscription and services income, creating ecosystem synergy with Coinbase’s retail trading and custody businesses, though USDC itself is not issued solely by Coinbase.

What Are the Risks of Coinbase Stock?

COIN’s main risks include: trading revenue’s high correlation with crypto market cycles; regulatory uncertainty from the SEC regarding digital assets; increased industry competition; and rising costs for asset security and compliance. Revenue structure shifts significantly with market cycles, requiring analysis of segment data and regulatory trends.

Which Revenue Stream Is More Stable: Trading or Subscription?

Subscription and services revenue is more stable than trading revenue, as it depends on subscriber count, custody balances, and ecosystem adoption rather than daily trading frequency. Trading revenue is more market-sensitive, and the mix between the two reflects COIN’s exposure to crypto cycles.