Coinbase Global, Inc. (NASDAQ: COIN) and Robinhood Markets, Inc. (NASDAQ: HOOD) are fundamentally different in their business models. COIN operates as a dedicated cryptocurrency trading and custody platform, generating revenue primarily from digital asset trading fees and subscription services. In contrast, HOOD is a full-service retail brokerage, relying on payment for order flow (PFOF), net interest income, and Gold subscriptions, with a primary focus on US equities and options. While both are Nasdaq-listed fintech companies, their underlying business structures and sensitivities to market cycles are distinct.

A common misconception when comparing COIN and HOOD is to simply categorize both as "fintech stocks," overlooking key differences in how they generate revenue and the regulatory frameworks they operate under. Coinbase (COIN) is positioned as a compliance-driven digital asset trading platform, offering retail trading, institutional custody, Coinbase One subscriptions, and participation in the USDC stablecoin ecosystem. To accurately assess industry differences, it's essential to first distinguish whether the company is a pure crypto exchange or a multi-asset retail broker, and then separately analyze trading, interest, and subscription revenues.

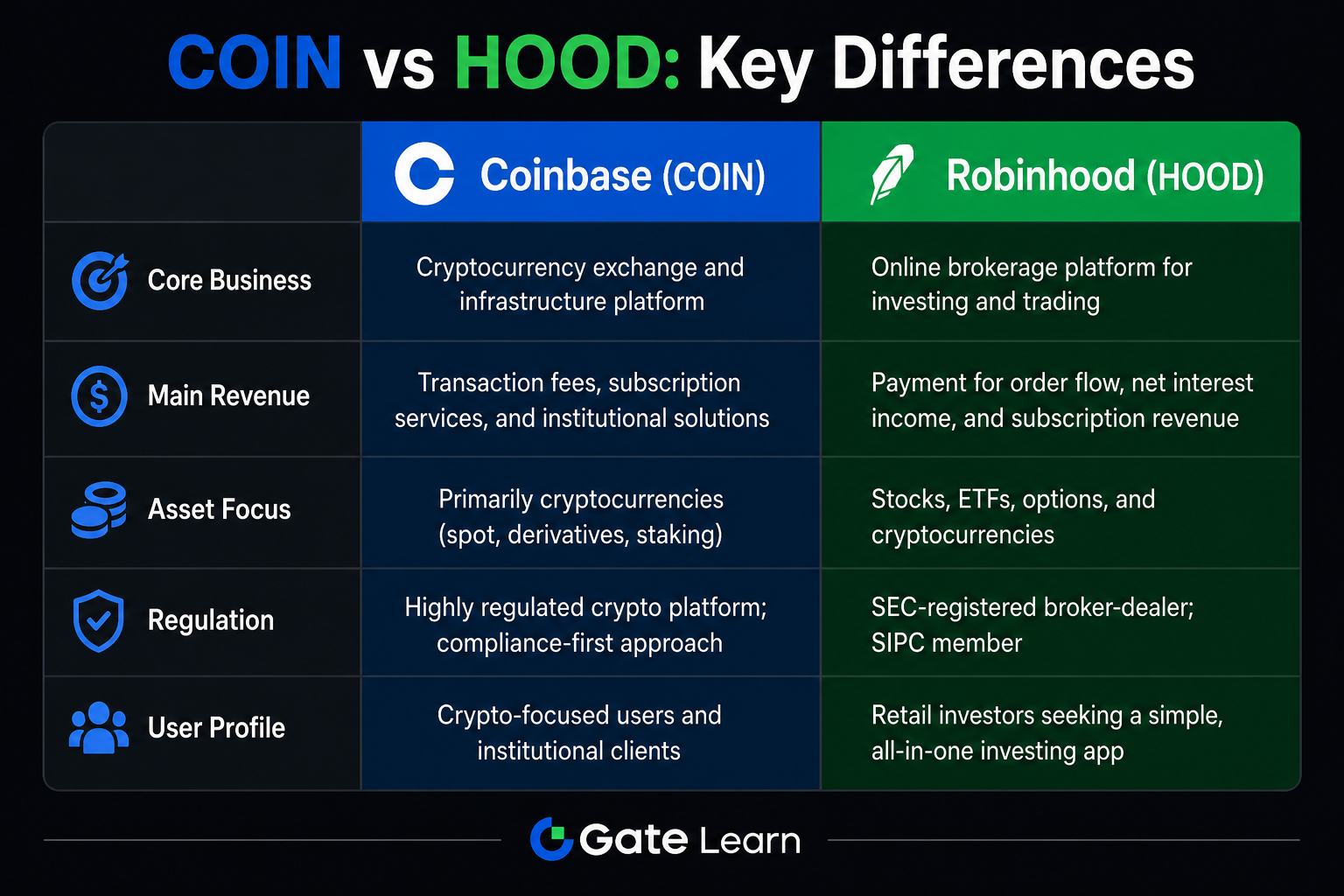

Figure 2. Key differences between COIN and HOOD: business focus, revenue drivers, asset allocation, and regulatory framework.

What Is COIN?

Coinbase Global, Inc. (COIN) is a Nasdaq-listed US cryptocurrency trading platform, trading under the ticker COIN. The company provides individuals and institutions with digital asset trading, custody, staking, and related financial infrastructure, and operates Base and other Layer 2 networks.

Coinbase fulfills three main roles in the industry: as a retail trading gateway, an institutional custody and Prime service provider, and an ecosystem participant in USDC stablecoin and developer APIs. COIN's revenue is split into transaction revenue and subscription and services revenue. Transaction revenue is directly tied to crypto market trading volumes, while subscription and services revenue includes Coinbase One, custody fees, blockchain reward sharing, and stablecoin-related income. In trading and industry comparisons, Coinbase should be evaluated separately from full-service brokers, Bitcoin-holding companies, and decentralized exchanges.

What Is HOOD?

Robinhood Markets, Inc. (HOOD) is a Nasdaq-listed US retail brokerage, trading under the ticker HOOD. The company offers retail clients zero- or low-commission trading in US stocks, options, ETFs, and select cryptocurrencies, and provides higher limits, lower rates, and cash management through its Robinhood Gold subscription.

Robinhood’s revenue model is built on payment for order flow (PFOF), net interest income, and Robinhood Gold subscription fees. PFOF is earned by routing retail orders to market makers; net interest income comes from client cash balances, securities lending, and credit card interest; Gold subscriptions provide recurring service fees. Compared to COIN, HOOD is primarily focused on US equities and options, with crypto trading comprising only a small part of its business. HOOD’s regulatory framework is based on SEC and FINRA broker-dealer rules, which differ structurally from the digital asset and money transmission licensing regime COIN faces.

How Do Revenue Drivers and Business Structures Differ?

The revenue drivers of COIN and HOOD reflect their core business differences. Coinbase’s revenue is highly elastic to crypto market activity: it collects fees from retail and institutional digital asset trades, with transaction revenue rising alongside market volume. Subscription and services revenue provides a stable recurring stream, including Coinbase One membership fees, custody fees, and stablecoin ecosystem revenue. The Coinbase stock business model is best understood by analyzing revenue by segment, fee structures, and user activity.

Robinhood’s revenue is more closely tied to US equity trading activity, client cash balances, and the interest rate environment. PFOF is linked to the volume of securities trades; net interest income is influenced by Fed policy and idle client funds. Crypto trading is a minor contributor to HOOD’s revenue, so it should not be viewed as a pure crypto trading platform.

| Revenue Type |

Coinbase (COIN) |

Robinhood (HOOD) |

| Trading-Related |

Digital asset trading fees (core) |

PFOF (US equity/options order routing) |

| Interest-Related |

Limited (not a core driver) |

Net interest income (client cash, securities lending) |

| Subscription-Related |

Coinbase One, custody fees |

Robinhood Gold membership fees |

| Other |

Stablecoin revenue, blockchain rewards, developer fees |

Credit card, minor crypto trading fees |

| Cycle Sensitivity |

Highly correlated with crypto trading volumes |

Driven by US equity activity and interest rates |

This table shows that COIN analysis should focus on crypto trading volumes and fee tiers, while HOOD analysis should emphasize securities trading volume, client asset balances, and interest rate variables.

Figure 1. COIN vs HOOD revenue drivers: trading fees, PFOF, net interest, and subscription service differences.

Figure 1. COIN vs HOOD revenue drivers: trading fees, PFOF, net interest, and subscription service differences.

Comparing Crypto Exposure and Regulatory Touchpoints

Crypto exposure is one of the most significant points of differentiation between COIN and HOOD. Coinbase’s core business revolves around digital assets—trading, custody, staking, and stablecoin ecosystems—all directly exposed to crypto market cycles and US digital asset regulation. While Robinhood offers some crypto trading, its crypto business represents a much smaller share of revenue and user engagement than COIN, and the company remains closer to a traditional retail brokerage.

On the regulatory front, Coinbase operates under SEC oversight, state money transmitter licensing, and custody rules. The classification of digital assets as securities, compliance costs, and litigation risk are ongoing factors. Robinhood is mainly regulated by the SEC and FINRA as a broker-dealer, subject to best execution, PFOF disclosures, client asset segregation, and options suitability rules, with crypto regulation playing a secondary role. SEC policy shifts on digital assets impact COIN more directly, while changes to broker-dealer rules or PFOF policies are more likely to affect HOOD’s revenue model and disclosure requirements.

Core Differences at a Glance

| Comparison Item |

Coinbase (COIN) |

Robinhood (HOOD) |

| Company Type |

Pure crypto trading platform |

Comprehensive retail broker |

| Listing Code |

NASDAQ: COIN |

NASDAQ: HOOD |

| Asset Focus |

Crypto assets |

US stocks, options, ETFs |

| Core Revenue |

Trading fees, subscription services |

PFOF, net interest, Gold subscription |

| Institutional Business |

Custody, Prime, OTC trading |

Limited |

| Stablecoin/On-Chain Ecosystem |

USDC, Base chain |

None |

| User Profile |

Crypto-native users, institutions |

Broad retail investors |

| Cycle Driver |

Crypto trading volumes |

US equity activity, interest rates |

| Regulatory Framework |

SEC + state money transmitter licenses |

SEC + FINRA broker-dealer rules |

This table summarizes the core differences between COIN and HOOD across nine key dimensions. When making comparisons, first determine whether the subject is a "crypto trading platform" or a "comprehensive broker," then select the appropriate revenue metrics and risk factors.

What Are the Limitations of This Comparison?

There are inherent structural limitations in comparing COIN and HOOD directly. Their financial reporting categories differ—Coinbase’s “transaction revenue” and Robinhood’s “transaction-type revenue (including PFOF)” do not cover the same scope and cannot be ranked by revenue share alone. User overlap does not imply identical business models: COIN’s crypto exposure spans trading, custody, staking, and stablecoins, while HOOD’s crypto business is just one part of a multi-asset brokerage. Their sensitivities to market cycles also differ, so it is inappropriate to use a single market indicator to explain both stocks’ performance.

Trading execution and fundamental analysis should be addressed separately. Gate’s COIN purchase guide covers account setup, ticker search, order placement, and fee verification; for HOOD, search for the ticker separately and verify the main entity, Robinhood Markets, Inc., to avoid selection errors.

Summary

Coinbase Global, Inc. (COIN) and Robinhood Markets, Inc. (HOOD) are both Nasdaq-listed fintech stocks, but they differ significantly in company type and revenue drivers. COIN is focused on digital asset trading and custody, generating revenue mainly from trading fees and subscription services, with concentrated exposure to crypto and digital asset regulatory risk. HOOD is centered on US equities, options, and some crypto brokerage, with revenue dependent on PFOF, net interest, and Gold subscriptions, fitting more closely within the traditional retail brokerage model. When comparing these two stocks, first classify by business focus, revenue structure, and regulatory touchpoints, then analyze their respective cycle sensitivities and compliance risks. Avoid relying on a single "fintech" or "crypto concept" label in place of a multi-dimensional assessment.

FAQ

What are the differences between COIN and HOOD?

COIN is a pure cryptocurrency trading platform, with revenue mainly from digital asset trading fees and subscription services, covering trading, custody, staking, and the USDC stablecoin ecosystem. HOOD is a full-service retail broker, with revenue dependent on payment for order flow, net interest income, and Gold subscriptions, focusing on US equities and options. The two differ in regulatory frameworks, user profiles, and sensitivity to market cycles.

What is Coinbase stock?

Coinbase stock refers to the common stock of Coinbase Global, Inc. traded on Nasdaq under the ticker COIN. The company is a major US digital asset trading platform, offering retail and institutional trading, custody, subscription services, the USDC stablecoin ecosystem, and Base chain infrastructure. It is not the same as comprehensive broker stocks like Robinhood.

How does trading COIN differ from traditional brokers?

COIN represents a listed crypto trading platform, with its stock price closely linked to crypto trading activity and digital asset regulatory developments. Traditional broker stocks (such as HOOD) are more influenced by US equity trading volumes, client asset balances, and interest rates. In trading, COIN and HOOD use different Nasdaq tickers, so always confirm the company when searching or reviewing positions.

How does Coinbase generate revenue?

Coinbase earns revenue mainly from two sources: transaction revenue (fees from retail and institutional digital asset trading) and subscription and services revenue (Coinbase One membership fees, custody fees, blockchain reward sharing, stablecoin-related income, and developer platform fees). Transaction revenue fluctuates with market activity, while subscription services provide a more stable recurring income stream.

What are the risks of Coinbase stock?

The main risks include high correlation of transaction revenue with crypto market cycles, uncertainty around SEC regulation of digital assets, intensifying industry competition, and rising costs for custody security and compliance. When comparing with HOOD, note the differences in revenue structure and regulatory touchpoints—do not apply the same risk checklist to both.