As on-chain derivatives trading continues to grow, Perp DEXs are gradually evolving from early AMM models toward order book models. More traders want to retain control over their on-chain assets while also gaining matching speed, market depth, and trading experience close to those of centralized exchanges.

Hyperliquid has gained attention in this context. Unlike traditional AMM-based perpetual protocols, it uses a native Layer 1 architecture and an on-chain order book mechanism, allowing trade matching, position management, and risk control to operate within one unified system.

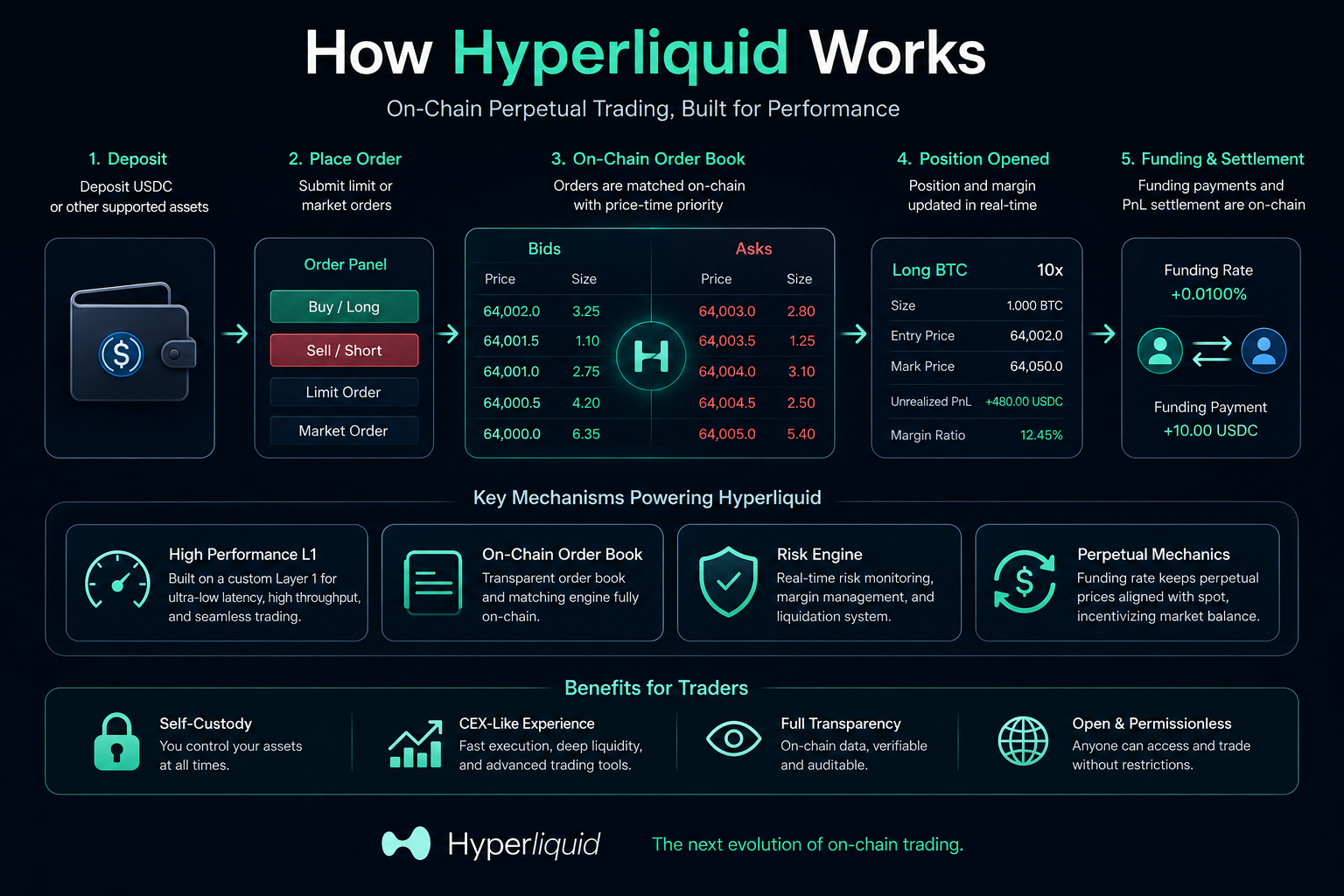

What Is Hyperliquid’s On-Chain Trading Process?

On Hyperliquid, a perpetual futures trade is not simply a matter of “placing an order and getting filled.” Internally, the system goes through multiple stages, including asset crediting, order broadcasting, matching, position updates, margin calculation, funding rate settlement, and risk monitoring.

Unlike most Perp DEXs that use AMM pricing, Hyperliquid manages bid and ask quotes through an on-chain order book, so its operating logic is closer to the matching engine of a traditional exchange. After a user submits an order, the system matches it based on price priority and time priority, then updates the account state in real time.

A complete trading process usually includes asset deposits, order submission, order matching, position opening, margin management, funding rate settlement, and final position closing. These modules work together to form Hyperliquid’s on-chain perpetual trading system.

How Do User Assets Enter the Hyperliquid System?

Before trading, users need to bridge or deposit assets into the Hyperliquid network. Because Hyperliquid uses its own native Layer 1, assets do not remain directly on the Ethereum mainnet. Instead, they enter Hyperliquid’s execution environment.

Once assets enter the system, they are recorded in the on-chain account state and serve as the margin base for later trading. Unlike centralized exchanges, users do not need to hand assets over to a traditional custodian. Instead, they control funds directly through on-chain accounts.

The system dynamically separates available margin, used margin, and unrealized profit and loss within an account. After users choose their leverage level, the account’s risk profile changes accordingly. The higher the leverage, the smaller the safety buffer needed to maintain the position, which makes liquidation easier to trigger.

This stage effectively determines the range of risk a user can absorb later, and it is a foundational part of the perpetual futures system.

How Does Hyperliquid’s Order Book Match Trades?

One of Hyperliquid’s core features is that it uses an on-chain order book instead of AMM pool pricing. After a user submits an order, the system broadcasts it to the on-chain matching engine and completes matching according to price priority and time priority.

This process is similar to that of a traditional exchange. Buy orders are matched against the lowest ask, while sell orders are matched against the highest bid. If the price cannot be filled immediately, the order enters the order book and waits for another trader to match it.

Users can submit market orders or limit orders. Market orders are executed immediately at the best available current price, while limit orders are executed only when the specified price is reached. Whether an order is filled immediately also affects the fee structure and the trader’s role in market liquidity.

| Role |

Meaning |

Impact on Liquidity |

| Maker |

Provides resting order liquidity |

Increases market depth |

| Taker |

Actively takes liquidity to execute |

Consumes market liquidity |

This structure is also one of the main reasons Hyperliquid is often compared with AMM-based Perp DEXs. The order book model places greater emphasis on real bid and ask depth and efficient price discovery, while the AMM model relies more on liquidity pool pricing.

After a Position Is Opened, How Does the System Calculate Profit, Loss, and Margin?

After an order is filled, the system creates the corresponding position and continuously tracks changes in market prices. The equity in a user’s account changes in real time with market fluctuations, while data such as entry price, current mark price, unrealized profit and loss, and margin ratio are updated at the same time.

The margin ratio can usually be expressed as:

$$\text{Margin Ratio}=\frac{\text{Account Equity}}{\text{Position Value}}$$

When the market price moves in a favorable direction, account equity increases. When it moves against the position, account equity decreases. To reduce the risk of market manipulation, most perpetual futures platforms do not use the latest traded price directly as the basis for risk assessment. Instead, they use a mark price mechanism. Hyperliquid also combines external market data with internal order book conditions to calculate risk levels.

This dynamic update mechanism means perpetual futures trading is always under real time risk assessment.

Why Does the Funding Rate Mechanism Keep Running?

Because perpetual futures have no expiration date, the system needs a funding rate mechanism to help keep the contract price close to the spot market.

The funding rate is essentially a periodic payment mechanism between long and short traders. When the perpetual price is above the spot price, longs usually pay shorts. When the perpetual price is below the spot price, shorts pay longs.

Funding payments can usually be expressed as:

$$\text{Funding Payment}=\text{Position Size}\times\text{Funding Rate}$$

This mechanism encourages the market to automatically balance long and short positioning, reducing the chance that perpetual prices remain far away from spot prices for extended periods. The funding rate is not a fixed fee charged by the platform. It is a dynamic exchange between traders and one of the key features that distinguishes perpetual futures from traditional futures.

When Is Hyperliquid’s Liquidation Mechanism Triggered?

The risk engine continuously monitors the margin level of every account. When account equity falls below the maintenance margin requirement, the system may trigger liquidation.

The core logic can be understood as:

$$\text{Account Equity}<\text{Maintenance Margin}$$

Once the risk threshold is triggered, the system automatically reduces or closes part of the position and completes the exit through market liquidity. The goal is to avoid negative account balances and maintain overall market stability.

Because Hyperliquid uses a high-performance order book structure, its liquidation process is usually closer to the logic of a traditional exchange than some AMM-based protocols. However, during extreme market conditions, wider slippage, declining liquidity, and cascading liquidations may still occur, so leveraged trading always carries significant risk.

Why Does Hyperliquid’s Native Layer 1 Affect the Trading Experience?

Most on-chain perpetual protocols are built on general-purpose smart contract chains, while Hyperliquid chose to build a native Layer 1. The core goal of this design is to bring order matching, state updates, risk calculation, and liquidation logic into the same execution environment.

As a result, Hyperliquid can achieve lower latency, higher-frequency state updates, and more stable order book depth.

| Capability |

Impact on Trading Experience |

| Lower latency |

Improves order response speed |

| High-frequency state updates |

Reduces price desynchronization |

| On-chain order book |

Improves depth and price discovery efficiency |

| Native risk engine |

Optimizes liquidation and margin management |

This architecture is also one of the main reasons Hyperliquid is often described as offering an “on-chain trading experience close to a CEX.”

How Is Hyperliquid Different from a Traditional CEX?

Although Hyperliquid’s trading experience is close to that of a centralized exchange, its underlying structure is still clearly different.

| Dimension |

Hyperliquid |

Traditional CEX |

| Asset custody |

Controlled through on-chain accounts |

Centrally custodied by the platform |

| Matching transparency |

Verifiable on-chain |

Internal system not visible |

| Liquidation mechanism |

Executed by on-chain rules |

Controlled inside the platform |

| Order book |

On-chain order book |

Centralized order book |

| Risk |

Smart contract and on-chain risks |

Custody and platform risks |

This difference also explains why more traders are paying attention to the trend of “CEX-like trading on-chain.” Hyperliquid is trying to create a new balance between self-custody and a high-performance trading experience.

Conclusion

Hyperliquid’s operating logic is built on an on-chain order book, a native Layer 1, and perpetual futures risk management mechanisms. A complete trade is not just a simple buy or sell action. It involves multiple systems working together, including matching, margin management, funding rates, risk monitoring, and liquidation.

Compared with earlier Perp DEXs, Hyperliquid places greater emphasis on high-performance matching and a trading experience closer to that of centralized exchanges, while maintaining on-chain transparency and asset self-custody. This model is also helping push the on-chain derivatives market from AMM structures toward high-performance order book architectures.

FAQs

Does Hyperliquid Use AMM?

No. Hyperliquid mainly uses an on-chain order book for matching, rather than relying on AMM liquidity pool pricing.

Why Is Hyperliquid’s Trading Experience Close to a CEX?

Because its native Layer 1 and high-performance matching engine enable lower latency, higher-frequency state updates, and more stable order book depth.

What Is the Purpose of Hyperliquid’s Funding Rate?

The funding rate is used to balance long and short positions and help keep perpetual contract prices close to the spot market.

How Does Hyperliquid’s Liquidation Mechanism Work?

When account equity falls below the maintenance margin requirement, the system automatically reduces or closes positions to control risk and avoid negative balances.

What Is the Biggest Difference Between Hyperliquid and Traditional Perp DEXs?

The biggest difference is its on-chain order book and native Layer 1 architecture, while most traditional Perp DEXs rely more on AMM models and general-purpose public chains.