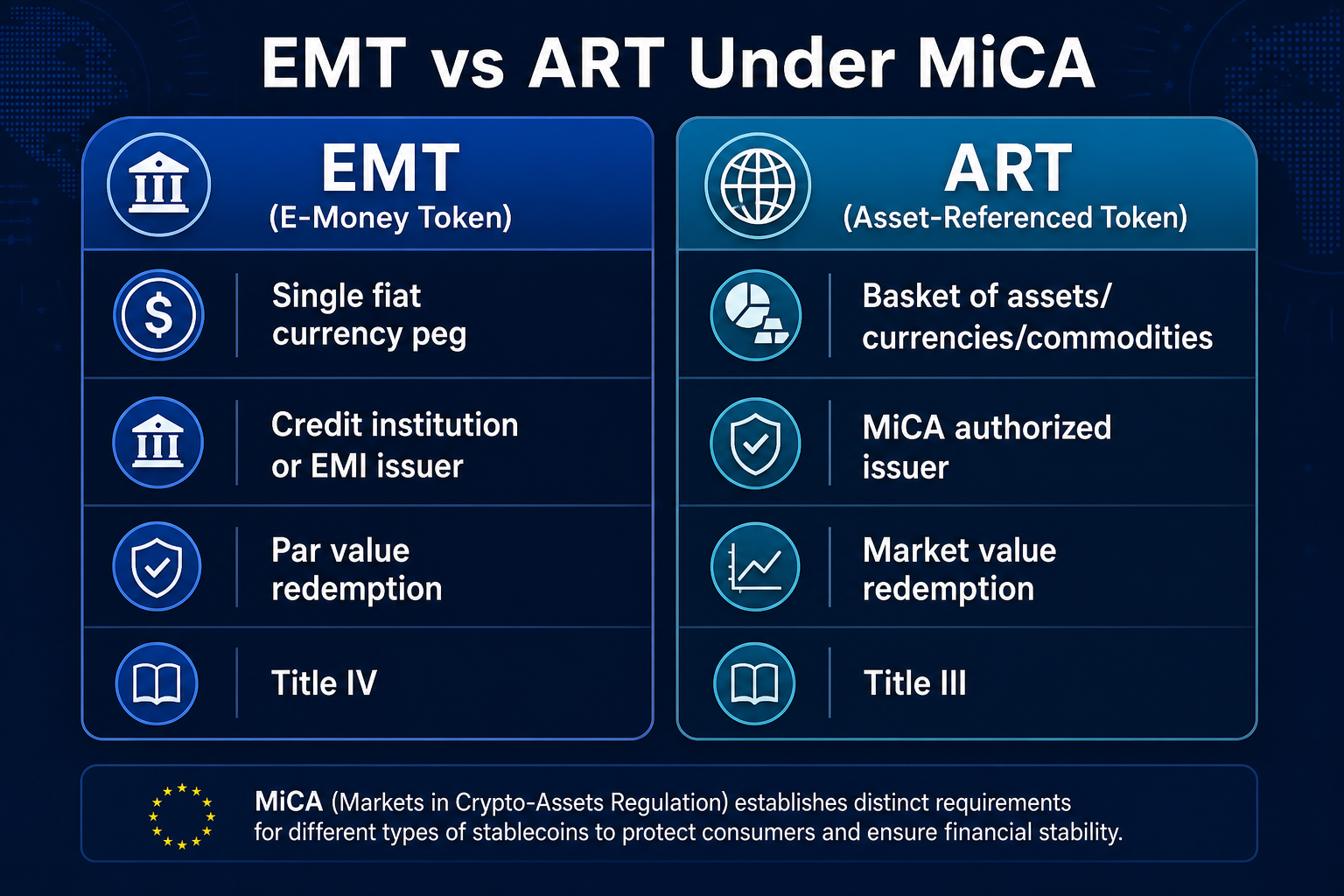

Under the EU's Markets in Crypto-Assets Regulation (MiCA), Electronic Money Tokens (EMTs) are pegged to a single fiat currency, while Asset-Referenced Tokens (ARTs) are backed by a basket of assets—this distinction forms the foundation of stablecoin regulatory categories. EMTs are primarily associated with payment and electronic money functions, whereas ARTs, due to their more complex value structures, are subject to stricter capital requirements and systemic risk management obligations.

Stablecoins act as value carriers in exchange settlement, cross-border payments, and DeFi liquidity. However, their differing peg mechanisms result in distinct compliance pathways and risk exposures. Understanding the unified classification logic set by MiCA EU Crypto Regulation is crucial to differentiating EMTs from ARTs.

From a digital asset service perspective, stablecoin issuance rules are closely integrated with the CASP Crypto Asset Service Provider licensing framework. When exchanges list, distribute, or provide custody for stablecoins, they must verify both the token's category and whether the issuer meets the relevant authorization requirements.

What Is an EMT?

Under MiCA, Electronic Money Tokens (EMTs) are crypto assets pegged to the value of a single fiat currency. Typical examples include stablecoins that maintain parity with one fiat currency, such as the US dollar or euro. EMTs are regulated much like electronic money: issuers must ensure that the token's value remains aligned with the referenced fiat, provide clear redemption rights to holders, and fully back circulation with highly liquid reserve assets. Most mainstream single-fiat-pegged stablecoins fall under the EMT category, though final classification depends on the issuer’s qualifications and disclosure practices.

What Is an ART?

Asset-Referenced Tokens (ARTs) under MiCA are crypto assets pegged to the value of a basket of assets, which may include multiple fiat currencies, commodities, bonds, or other digital assets. Because ARTs have a diversified peg structure, they can exert wider systemic effects. MiCA therefore imposes stricter own capital requirements, reserve matching rules, and risk management obligations on ART issuers, who must submit a regulator-reviewed whitepaper. Stablecoins pegged to multiple currencies or backed by multiple reserve assets typically fall under the ART classification.

Key Differences at a Glance

The table below compares EMTs and ARTs across five dimensions: peg mechanism, regulatory classification, issuer qualification, capital requirements, and risk focus.

| Comparison Dimension |

EMT (Electronic Money Token) |

ART (Asset-Referenced Token) |

| Peg Mechanism |

Single fiat currency |

Basket of assets (multi-fiat, commodities, etc.) |

| Regulatory Focus |

Electronic money/payment |

Multi-asset reference, higher systemic risk |

| Issuer Qualification |

Credit institution, electronic money institution, or MiCA-authorized EMT issuer |

MiCA-authorized ART issuer |

| Capital Requirements |

Focus on reserve adequacy and redemption guarantees |

Higher own capital thresholds (e.g., minimum proportion or amount of reserves) |

| Risk Focus |

Payment stability, redemption liquidity |

Basket volatility, cross-contagion, systemic impact |

Figure 1. Core differences between EMTs and ARTs under MiCA: peg mechanism, issuer qualification, capital requirements, and risk focus.

As shown, EMTs and ARTs differ not only in their peg (single fiat vs. diversified assets), but also in issuer qualification thresholds and regulatory rigor. EMT rules are more aligned with payment compliance, while ART rules emphasize capital buffers and risk isolation for complex asset structures.

Who Can Issue EMTs and ARTs?

EMT issuers must be one of the following: a credit institution authorized under the Capital Requirements Directive (CRD); an electronic money institution authorized under the Electronic Money Directive (EMD); or another qualified entity authorized to issue EMTs under MiCA. Entities lacking proper authorization cannot issue EMTs to the public in the EU.

ART issuers must apply for MiCA authorization from their national competent authority, submit a regulator-reviewed whitepaper, governance structure, and risk management plan, and maintain minimum own capital (typically not less than a set proportion of reserves or a statutory minimum). Distribution platforms such as exchanges and brokers must hold a CASP license and verify issuer authorization and token category before listing.

How Do Reserve and Redemption Rules Differ?

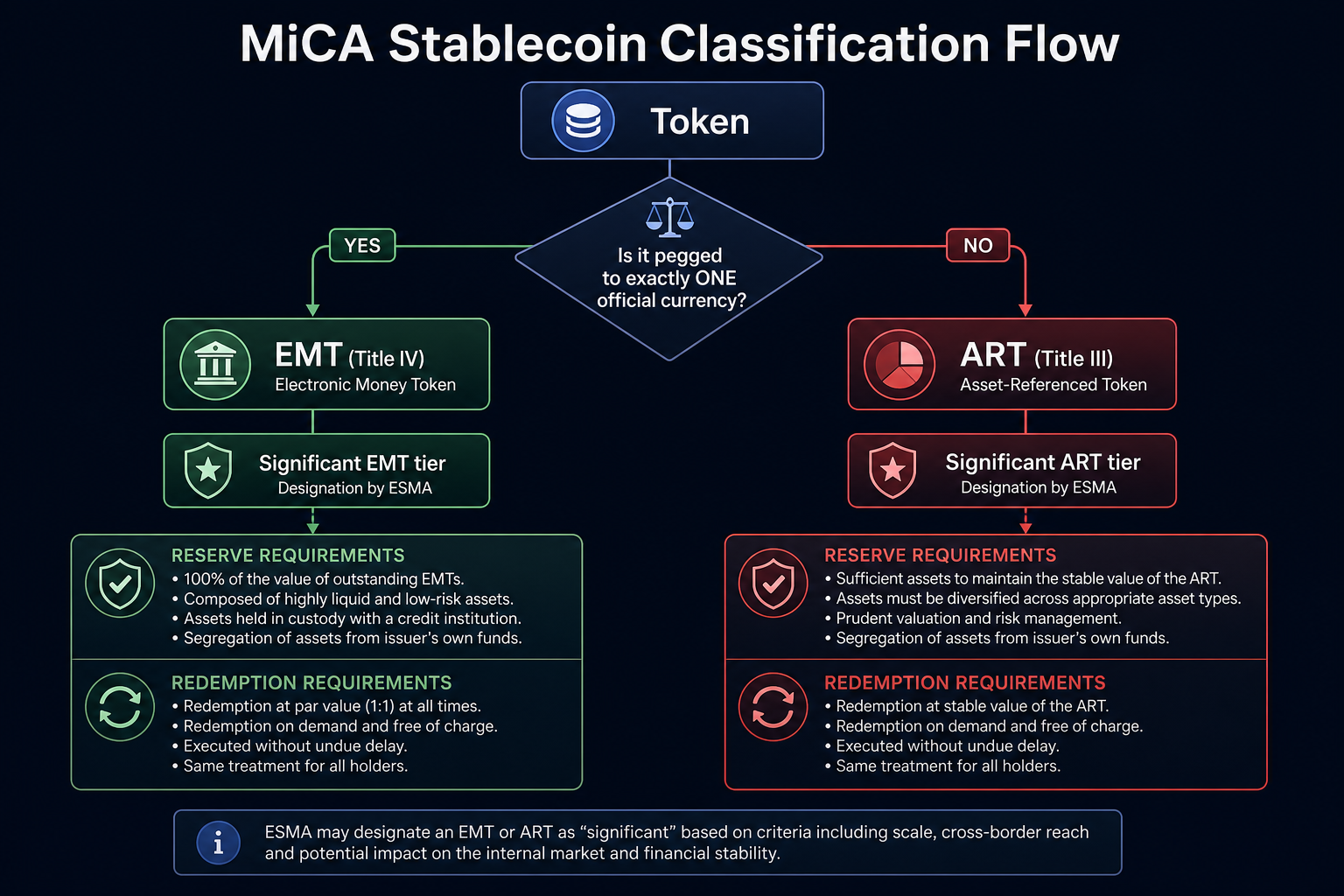

EMT reserve rules require issuers to fully back all circulating EMTs with reserves at all times. These reserves must be invested in safe, low-risk assets and segregated from the issuer’s own assets. Holders have the right to redeem at face value for the referenced fiat currency, and the redemption mechanism must be clearly disclosed in the whitepaper.

ART reserve rules require that reserve assets match the reference basket, providing sufficient liquidity and diversification to address fluctuations in basket components. ART holders are entitled to redeem or exit their position according to the agreed mechanism, with details specified in the whitepaper. Both token types must continually disclose reserve composition and submit regular reports to regulators.

What Is a Significant Token?

MiCA introduces a “Significant Token” classification, imposing stricter regulatory obligations on EMTs or ARTs with major market impact. Regulators assess factors such as number of holders, circulation size, trading volume, cross-border usage, and integration with the financial system. Once a token is classified as significant, issuers must meet higher own capital requirements, increase the frequency of reserve disclosures, and establish more robust risk management and contingency plans.

Figure 2. MiCA stablecoin classification: base categories (EMT/ART) and additional capital and disclosure obligations for Significant Tokens.

The Significant Token mechanism embodies MiCA’s risk-tiered approach: the greater the market impact, the higher the issuer’s regulatory responsibilities.

How Are USDT, USDC, and EURC Classified Under MiCA?

Mainstream fiat-pegged stablecoins are typically classified as EMTs under MiCA. USDT (Tether) maintains a 1:1 peg with the US dollar and is categorized as an EMT; Tether must secure EMT issuance authorization and comply with reserve, redemption, and disclosure obligations. USDC (USD Coin) is also pegged to the US dollar and falls under the EMT category; full compliance depends on the outcome of EU authority authorization and ongoing reviews. EURC (Euro Coin) is pegged to the euro and is a typical euro-denominated EMT, subject to EMT compliance standards. MiCA Regulation of USDT and USDC further explores reserve management and Significant Token compliance for major dollar stablecoins in the EU.

The table below summarizes the preliminary classification of three major stablecoins. Actual compliance status depends on issuer disclosures and regulatory authorization.

| Stablecoin |

Pegged Currency |

Preliminary MiCA Classification |

Key Compliance Considerations |

| USDT |

USD |

EMT |

Issuer authorization, reserve disclosure, redemption mechanism |

| USDC |

USD |

EMT |

Authorization progress, reserve attestation, EU distribution arrangements |

| EURC |

EUR |

EMT |

Euro reserve matching, EMT issuer qualification, Significant Token threshold |

Summary

MiCA divides stablecoins into two main categories: EMTs, pegged to a single fiat currency and subject to electronic money regulation; and ARTs, pegged to a basket of assets and subject to stricter capital and systemic risk controls. Issuer qualification, reserve and redemption rules, and the Significant Token classification together form the core of EU stablecoin compliance. Mainstream fiat-pegged stablecoins such as USDT, USDC, and EURC are typically classified as EMTs, but ultimate compliance depends on issuer authorization and ongoing regulatory adherence.

FAQ

What’s the difference between EMT and ART?

EMTs are pegged to a single fiat currency and regulated similarly to electronic money and payment tools, with a focus on reserve adequacy and redemption guarantees. ARTs are pegged to a basket of assets with more complex value sources, requiring higher own capital and advanced risk management. MiCA uses the peg mechanism as the starting point, then overlays issuer qualification and Significant Token classification rules.

Is USDT an EMT or ART?

USDT is generally pegged 1:1 to the US dollar and, under MiCA, is classified as an EMT. Final regulatory determination depends on Tether’s issuance authorization, reserve management, disclosure, and EU compliance. MiCA does not ban USDT, but requires issuers to meet EMT regulatory standards.

Who can issue EMTs under MiCA?

EMT issuers must be authorized credit institutions, electronic money institutions, or other qualified entities authorized under MiCA. Issuers must maintain 100% reserve backing, a clear redemption mechanism, and ongoing reserve disclosures. Entities without proper authorization cannot issue EMTs to the public in the EU.

What are MiCA’s requirements for stablecoin reserves and redemption?

Issuers must fully back circulating stablecoins with highly liquid reserves, segregated from their own assets. EMT reserves must always cover the circulating supply at a 100% ratio, and holders are entitled to redeem at face value for fiat. ART reserves must match the reference basket, with redemption terms clearly listed in the whitepaper. Both token types must regularly disclose reserve composition and report to regulators.

What is a Significant Token under MiCA?

A Significant Token is an EMT or ART that meets regulatory thresholds for number of holders, circulation size, trading volume, or cross-border impact. Once classified as significant, issuers face higher own capital requirements, more frequent disclosures, and stricter liquidity and risk management to address the systemic impact of large stablecoins.

How is EURC classified under MiCA?

EURC is pegged to the euro and is a typical EMT. Euro stablecoin issuers must comply with EMT rules, ensure euro reserves match circulation, guarantee redemption rights, and complete MiCA issuance or distribution authorization. If circulation reaches significant thresholds, EURC may also be subject to additional Significant EMT regulatory obligations.