As the crypto industry moves into an institutional phase, regulation has become one of the key factors shaping market development. Over the past decade, the United States has consistently ranked among the largest crypto asset markets globally, while the European Union has pioneered the world's first comprehensive crypto asset legal framework—the MiCA Regulation. These two major economies have adopted divergent regulatory approaches, leading to two distinct models of industry evolution.

For cryptocurrency exchanges, stablecoin projects, Web3 startups, and institutional investors, both regulatory frameworks—covering market access, licensing, token issuance, and stablecoin operations—are shaping global expansion strategies and long-term development roadmaps.

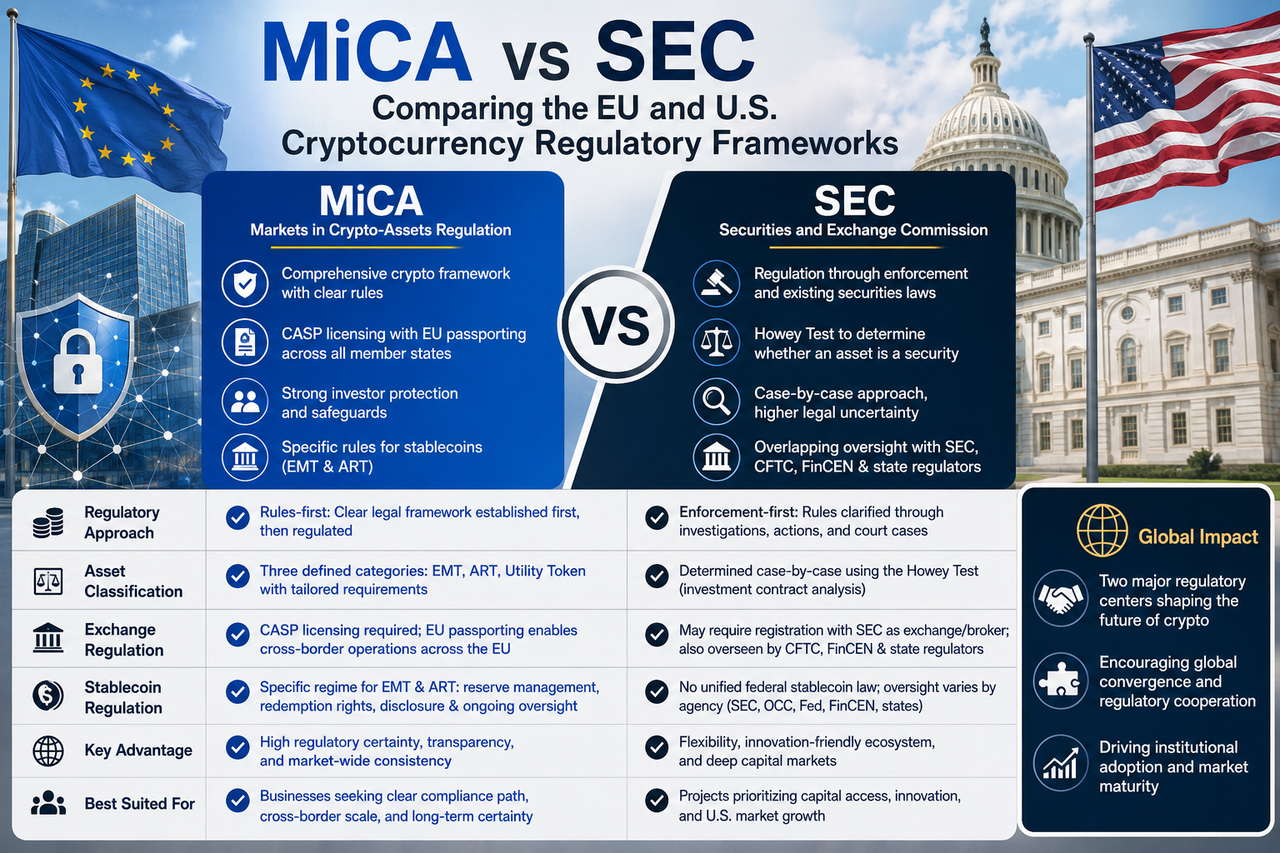

What Are MiCA and SEC?

MiCA stands for Markets in Crypto-Assets Regulation, a unified regulatory framework tailored by the European Union for the digital asset industry. Its scope encompasses crypto asset issuance, stablecoin management, exchange operations, and investor protection, all aimed at establishing consistent standards across the EU market.

The SEC (U.S. Securities and Exchange Commission) oversees the U.S. securities market. Since the U.S. lacks a federal-level law specifically for crypto, the SEC regulates digital asset projects under existing securities laws, defining regulatory boundaries through enforcement actions.

In essence, MiCA is a new regulation purpose-built for the crypto industry, while the SEC extends traditional financial oversight to the digital asset market.

What Is the Core Difference Between MiCA and SEC?

The fundamental difference lies in regulatory philosophy.

The EU follows a "rules-first" model: it first creates a complete legal framework, then enforces based on those rules. Companies entering the market usually understand their compliance requirements, licensing conditions, and operational responsibilities upfront.

The U.S. adopts an "enforcement-first" approach. Through investigations, penalties, and litigation, regulators gradually clarify which digital assets may be securities and which business models require oversight.

This creates higher regulatory certainty in Europe, while the U.S. market retains greater flexibility and interpretive leeway. For crypto enterprises seeking long-term, stable growth, clear regulatory expectations are often more attractive.

How Does MiCA Define Crypto Assets?

To create a unified system, MiCA explicitly categorizes digital assets and applies differentiated rules to each category.

- Electronic Money Tokens (EMTs): Stablecoins pegged to a single fiat currency.

- Asset-Referenced Tokens (ARTs): Tokens linked to multiple assets, including fiat, commodities, or other digital assets.

- Utility Tokens: Tokens providing access to specific products, services, or blockchain network functions.

This classification lets projects identify their regulatory category early, enabling more precise token issuance, product design, and compliance planning. Unlike models reliant on regulatory interpretation, MiCA's system reduces legal uncertainty.

How Does the SEC Determine If a Crypto Asset Is a Security?

Unlike the EU, the U.S. has no unified digital asset classification system.

The SEC typically applies the Howey Test to decide if an asset is a security. Under this test, if investors contribute money and reasonably expect profits from the efforts of others, the asset may be deemed a security.

Because different projects have varying business models and token structures, the same test can yield different outcomes in different contexts. This is a key reason for the long-running U.S. debate over whether certain tokens are securities.

This model offers high flexibility but also brings greater legal risk and compliance uncertainty for crypto projects.

How Does MiCA Regulate Cryptocurrency Exchanges?

MiCA establishes a unified framework through the CASP (Crypto-Asset Service Provider) regime. Any platform offering digital asset services to EU users generally needs CASP authorization.

Beyond licensing, MiCA requires exchanges to implement robust customer asset protection mechanisms, risk management systems, and market surveillance to ensure user asset safety and prevent manipulation.

After obtaining CASP authorization, companies can use the EU passporting mechanism to operate across the entire EU market, without needing separate licenses in each member state. This drastically reduces cross-border operational costs and supports the development of a unified European digital asset market.

How Does the SEC Regulate Cryptocurrency Exchanges?

The U.S. exchange regulatory system is more complex.

Beyond the SEC, certain activities may also fall under the Commodity Futures Trading Commission (CFTC), Financial Crimes Enforcement Network (FinCEN), and state-level regulators. If a platform is found to offer securities trading services, it may need to register and operate as a securities exchange or broker-dealer.

Due to ongoing disputes over digital asset classification, many exchanges face persistent regulatory investigations and litigation risks. This raises compliance costs and increases policy uncertainty for market participants.

How Do MiCA and SEC Differ on Stablecoin Regulation?

Stablecoins are a key focus for both regulators, but their approaches diverge significantly.

MiCA has created a dedicated stablecoin framework, splitting them into EMTs and ARTs. Requirements cover reserve asset management, user redemption rights, information disclosure, risk control, and ongoing supervision.

For major stablecoins like USDT and USDC, MiCA provides a relatively clear compliance pathway, allowing issuers to adjust their business structures accordingly.

The U.S. currently lacks a unified stablecoin law. The SEC focuses on whether stablecoins involve security attributes, while other agencies oversee them from payment, banking, and anti-money laundering perspectives. As a result, the U.S. stablecoin regulatory system is still evolving.

Why Is MiCA Considered More Certain?

MiCA has drawn global attention primarily because its framework offers high certainty.

Through a unified legal text, MiCA explicitly defines asset classifications, market access standards, licensing regimes, and operational obligations. Companies can assess compliance costs before launching and plan long-term strategies.

For large financial institutions and institutional investors, regulatory clarity often outweighs a lenient but ambiguous environment. That's why more international exchanges and Web3 companies are making Europe a key market for their global compliance strategies.

What Are the Strengths of the SEC Model?

While MiCA excels in certainty, the SEC model has its own advantages.

The U.S. boasts the world's largest capital market and most mature financial innovation ecosystem. Its long-standing regulatory experience allows it to quickly identify market risks and respond. Moreover, case-driven regulation leaves more room for innovation, avoiding premature rules that could hinder emerging technologies.

Thus, the U.S. model emphasizes the interaction between market practice and regulation, while the European model prioritizes rule clarity and institutional design.

How Will MiCA and SEC Shape the Global Crypto Industry?

As the digital asset market matures, the EU and U.S. are emerging as the two most influential regulatory centers.

Europe attracts enterprises and institutional capital seeking a clear regulatory environment through MiCA. The U.S. maintains its lead through a vast financial market and innovation ecosystem. In the future, more countries may combine MiCA's unified legislative approach with the U.S.'s enforcement and market oversight experience.

Over the long term, global crypto regulation is likely to converge toward a hybrid model—offering both legal certainty and space for innovation.

Summary

MiCA and SEC represent the world's two most important cryptocurrency regulatory models. MiCA establishes clear market rules and a licensing system through unified legislation, while the SEC relies on existing securities laws and enforcement actions. They differ significantly in asset classification, exchange regulation, stablecoin management, and market access.

As the crypto industry becomes more institutional and global, the regulatory environment will be a key competitive factor. For exchanges, stablecoin issuers, and Web3 projects, understanding MiCA and SEC's regulatory logic is essential—not only for global compliance strategies but also for navigating the future of digital asset markets.

FAQs

Is MiCA stricter than the SEC?

They can't be simply compared. MiCA is defined by clear, broad rules; the SEC emphasizes enforcement and security classification. MiCA offers more certainty; the SEC offers more flexibility.

How does MiCA regulate cryptocurrency exchanges?

MiCA requires exchanges to obtain CASP (Crypto-Asset Service Provider) authorization and to set up customer asset protection, risk management, and market surveillance. Once authorized, they can operate across the entire EU.

How does the SEC determine if a cryptocurrency is a security?

The SEC uses the Howey Test: if investors contribute money and expect profits from others' efforts, the asset may be a security.

How do MiCA and SEC differ on USDT and USDC?

MiCA has a dedicated stablecoin framework with clear rules on reserves, redemption, and disclosure. The U.S. lacks a unified stablecoin law, with oversight spread across multiple agencies.

Why are more crypto companies paying attention to MiCA?

MiCA offers unified rules and a clear compliance path, making it easier to assess costs and risks. After obtaining CASP authorization, companies can access the entire EU market—a major draw for international crypto firms.