For modern banks, profitability relies not only on loan volume but also on customer base, assets under management (AUM), the interest rate environment, and risk control capabilities. The key reason PNC has maintained a leading position in the U.S. regional banking market is its integrated financial ecosystem spanning personal finance, corporate finance, and wealth management.

PNC Stock Basics

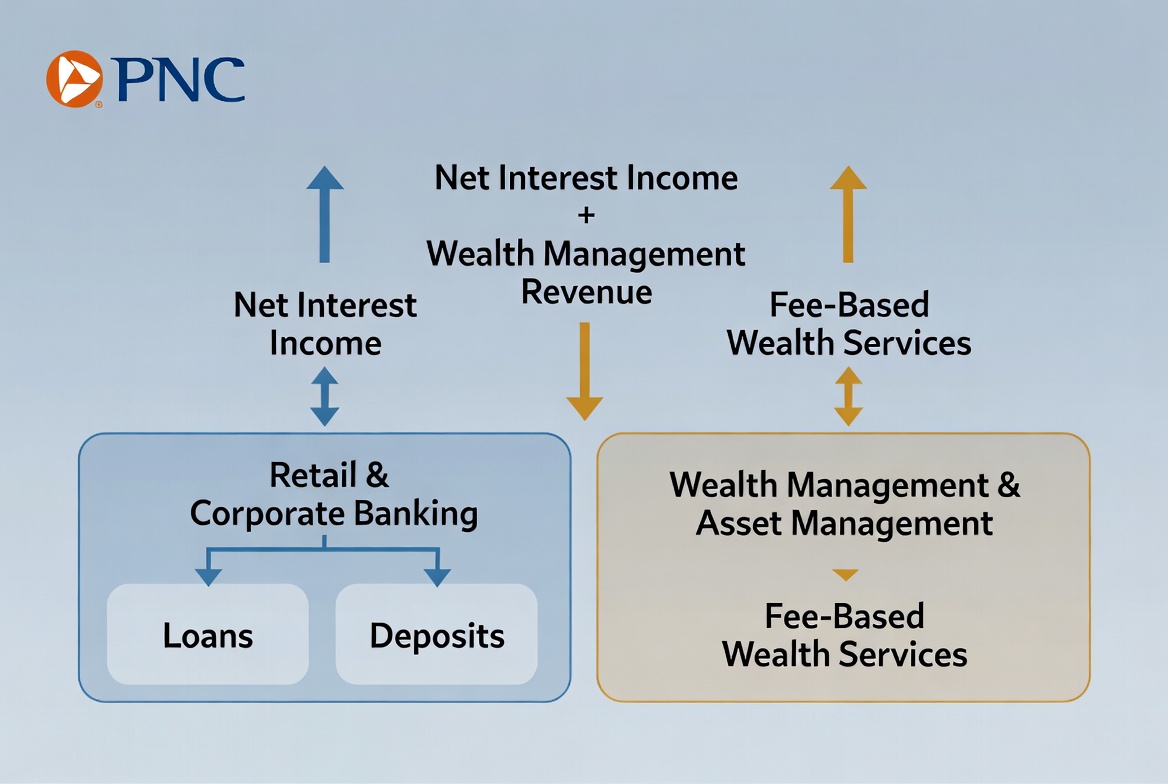

PNC operates across commercial banking, retail banking, wealth management, and corporate finance, serving individual consumers, small and midsize businesses, large corporations, and institutional investors. Compared to community banks, PNC offers a more comprehensive service suite; relative to global giants like JPMorgan Chase, PNC stays focused on the U.S. domestic market.

PNC is the New York Stock Exchange ticker for PNC Financial Services Group. Headquartered in Pittsburgh, Pennsylvania, it ranks among the largest U.S. regional banking groups by asset size.

Within the U.S. banking sector, PNC is widely regarded as a key representative of the regional banking space. Its performance is closely tied to U.S. economic growth, loan demand, consumer spending, and interest rate movements, making it a bellwether for the U.S. financial industry.

PNC’s Revenue Streams

PNC’s revenue falls into two primary categories: interest income and non-interest income. Interest income has long been the core driver, while wealth management and corporate finance are steadily boosting the significance of non-interest income.

The most traditional banking profit model stems from deposit-taking and lending. PNC gathers customer deposits as a funding base, then extends loans to individuals and businesses, earning the spread between loan interest and deposit costs. This model, known as net interest income, remains the most critical revenue source for most banks.

At the same time, modern banks are increasingly prioritizing non-interest income. Wealth management, investment advisory, cash management, payment services, and capital markets activities all generate fee income. These revenue streams are less directly dependent on loan volume, helping to create a more stable and diversified income structure.

| Revenue Source |

Key Components |

| Interest Income |

Personal loans, commercial loans, credit products |

| Wealth Management Income |

Investment advisory fees, asset management fees |

| Corporate Finance Income |

Cash management, financing services |

| Service Fee Income |

Payment, account, and transaction services |

This composition allows PNC to maintain relatively balanced growth across different economic conditions.

How Deposit and Lending Generate Revenue

Deposit-taking and lending form the bedrock of PNC’s business model and the classic profit engine of banking. Banks acquire funds by accepting deposits and then deploy those funds into loans, creating a capital cycle.

For individuals, loan products include mortgages, auto loans, lines of credit, and credit cards. For businesses, the offerings span operating loans, equipment financing, commercial real estate lending, and merger financing. All these loans generate interest income, a core profit driver.

Profitability hinges on spread management. In simple terms, PNC pays depositors a lower interest rate than it charges on loans; the difference is net interest income. For example, when a bank attracts low-cost deposits and lends at higher rates, it secures stable returns.

But lending is not risk-free. Banks must assess borrowers’ creditworthiness and repayment ability to minimize defaults. Thus, risk management capability is a key determinant of profitability in deposit and lending operations.

How Wealth Management Fuels Growth

As client assets grow, wealth management has become one of the most important growth areas for modern banks. For PNC, it not only adds revenue but also strengthens long-term client relationships.

Wealth management serves high-net-worth individuals, family offices, and institutional investors. Services include asset allocation, retirement planning, investment advisory, trust services, and wealth transfer planning. Unlike lending, wealth management focuses on long-term asset appreciation and risk management.

A key advantage of wealth management is its relatively stable revenue model. Many asset management products charge fees based on AUM, so revenue scales with client asset growth. This reduces the bank’s dependence on loan demand and interest rate cycles.

For PNC, wealth management has become a vital part of business evolution. With an aging U.S. population and growing wealth accumulation, demand for investment planning and wealth transfer continues to rise, offering long-term growth potential.

How Corporate Finance Expands Revenue

Corporate finance is a key differentiator for PNC compared to typical retail banks. Corporate clients often require more complex financing and higher-value services.

Businesses need loans for expansion, equipment purchases, or working capital. Beyond traditional lending, PNC offers cash management, payment processing, trade finance, and capital markets services to optimize capital efficiency.

Large corporations demand specialized solutions—cross-border payments, foreign exchange risk management, bond issuance advisory, and M&A financing. These services generate fee income and deepen client loyalty.

By engaging with companies at various growth stages, PNC builds enduring partnerships. Corporate clients bring not only loan revenue but also cross-selling opportunities, further diversifying income sources.

Why the Interest Rate Environment Matters

The interest rate environment is a critical external factor for bank profitability. Banks profit from the spread between funding costs and loan returns, so rate changes directly affect net interest income.

When rates rise, new loans typically earn higher interest. If deposit costs rise more slowly, banks can widen their net interest margin, boosting profits. In certain phases, a rising rate environment can therefore benefit bank earnings.

However, higher rates may dampen loan demand and increase repayment burdens. If economic growth slows or defaults rise, banks face headwinds.

For a regional bank like PNC, rates affect not only loan yields but also deposit behavior and overall financial market activity. As a result, interest rate cycles are a key factor for investors analyzing banking performance.

Summary

PNC’s business model rests on deposit-taking and lending, wealth management, and corporate finance. Interest income remains the dominant revenue source, while wealth management and corporate finance build a more diversified profit structure. At the same time, the interest rate environment, loan demand, and risk management continually shape the bank’s performance. Through a comprehensive financial ecosystem serving both individuals and businesses, PNC has established itself as a major force in U.S. regional banking.

FAQ

How does PNC make money?

PNC generates revenue primarily through loan interest income, wealth management fees, corporate finance fees, and payment and account service charges.

What is net interest income?

Net interest income is the difference between a bank’s interest earned on loans and the interest paid on deposits. It is one of the most critical profit sources for banks.

Why is wealth management important?

Wealth management provides stable fee income tied to AUM, reducing the bank’s reliance on lending and interest rate cycles.

What does corporate finance include?

Corporate finance typically covers commercial lending, cash management, payment processing, trade finance, and capital markets services.

How do interest rate changes affect PNC?

Rate changes influence loan yields, deposit costs, and loan demand, directly impacting net interest income and overall profitability.

Is PNC a regional or national bank?

PNC is classified as a large regional bank. It operates across multiple U.S. states but remains primarily focused on the domestic market.