What Is Robinhood?

Robinhood is a U.S. fintech company best known for its “zero-commission trading” model. Initially targeting young retail investors, the platform rapidly scaled its user base by lowering barriers to entry. Its products are built around:

During the 2020–2021 retail trading boom, Robinhood leveraged meme stocks (like GameStop) and crypto asset trading to become a symbol of “democratizing finance for retail investors.”

However, as market cycles shifted and regulations tightened, this business model—highly dependent on active trading volume—began to encounter significant challenges.

Q1 Earnings Report: Key Metrics Explained

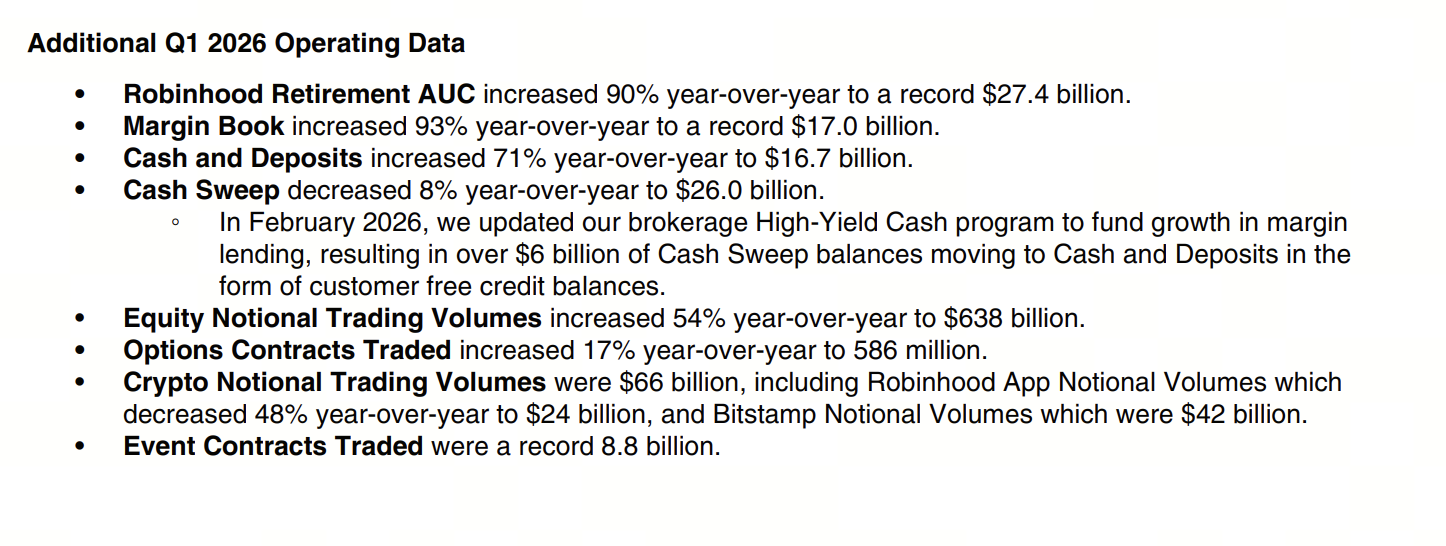

Image source: Robinhood Financial Report

The latest quarterly data reveals clear “structural divergence” for Robinhood:

-

Crypto revenue: $134 million (down 47% year-over-year)

-

Crypto trading volume: $24 billion (down 48% year-over-year)

-

Total trading revenue: $623 million (up 7% year-over-year)

-

Options revenue: $260 million (up 8% year-over-year)

-

Stock revenue: $82 million (up 46% year-over-year)

-

Net profit: $346 million (up 3% year-over-year)

Additionally, the company reported its Ethereum Layer 2 network has processed more than 100 million transactions to date.

This data sends a clear signal: Robinhood isn’t declining—it’s “switching growth engines.”

Crypto Business Decline: Cyclical or Structural?

The sharp drop in crypto revenue and trading volume is this quarter’s most notable shift, but it must be viewed in the broader industry context.

Market in a Low-Volatility Phase

Trading platform revenue is closely tied to volatility. When markets move from trends to sideways action, user trading frequency naturally drops.

Retail Trading Enthusiasm Fades

The speculative frenzy fueled by meme coins, NFTs, and high leverage trading has cooled, making users more cautious.

Capital Migrates to Traditional Channels

With institutions like BlackRock launching crypto ETFs, some capital is now accessing the market through traditional financial systems. This means:

In summary, this is not just a Robinhood issue—it’s a cyclical correction and structural shift across the entire crypto trading sector.

Non-Crypto Revenue Growth: Robinhood’s “Second Growth Curve”

As the crypto business declines, Robinhood’s other segments are delivering solid results, providing new growth drivers.

Options: A Stable Cash Flow Engine

Options revenue reached $260 million, up 8% year-over-year.

Key features of the options segment:

-

High frequency trading

-

High leverage

-

Stable fee structure

This makes options one of Robinhood’s most reliable profit sources.

Stock Trading: Traditional Markets Rebound

Stock revenue surged 46% year-over-year, reflecting:

Event Contracts: The Standout New Variable

Event contract revenue soared 320% year-over-year, making it the biggest highlight.

These products let users trade on event outcomes, such as:

-

Macroeconomic data

-

Political developments

-

Market trends

Essentially, this is a “financialized prediction market.” The trend closely mirrors on-chain prediction markets, showing that traditional platforms are adopting Web3 product logic.

What Does the Surge in Event Contracts Mean?

The growth in event contracts isn’t just about revenue—it reflects a shift in user behavior:

From “Price Speculation” to “Outcome Betting”

Users are moving beyond trading price movements to participating in the outcomes of events themselves.

From “Long-Term Holding” to “Short-Term Engagement”

Event contracts typically have short cycles, fitting well with fragmented trading habits.

The underlying asset is no longer just a financial instrument, but “information and probability.”

This could signal a broader trend: in the future, segments of the financial market may be built around “events” rather than traditional assets.

Beyond short-term revenue shifts, Robinhood’s Layer 2 strategy is even more significant.

Its L2 network has processed over 100 million transactions, signaling that:

-

Users are interacting on-chain

-

The platform is evolving beyond trade matching

-

Robinhood is entering core infrastructure competition

Strategic Value of This Approach:

Strengthen user retention: User assets and activity remain within the Robinhood ecosystem.

Lower trading costs: L2 enables a more efficient settlement experience.

Expand use cases: The platform can support DeFi, NFTs, on-chain identity, and more in the future.

In essence, this replicates a proven path: centralized platform → proprietary chain → ecosystem building.

Industry Shifts: Robinhood Faces a New Competitive Landscape

The current market has entered a “multi-layered competition” era:

Trading Layer Competition

Traditional brokers, crypto exchanges, and ETF products are all competing for user trading activity.

Infrastructure Competition

Boundaries between on-chain ecosystems and centralized platforms are blurring.

User Onboarding Competition

Controlling user accounts and capital inflows is key to market leadership.

In this environment, Robinhood must successfully transform or risk being sidelined.

The Deeper Causes of the Stock Price Drop

Despite a solid earnings report, Robinhood’s stock fell more than 6% after hours, mainly due to:

Core Business Missed Expectations

The market was expecting a rebound in crypto activity.

Concerns About Growth Quality

While event contracts are growing rapidly:

Unclear Valuation Logic

Investors are still reassessing Robinhood’s strategic positioning.

Robinhood’s Future: Three Clear Strategic Paths

Based on current data and strategy, Robinhood may pursue three directions:

Integrate stocks, options, crypto, and derivatives to become a one-stop trading gateway.

Path 2: On-Chain Infrastructure Gateway

Build its own Web3 ecosystem via Layer 2.

Continue expanding new products like event contracts.

In the end, Robinhood’s future may combine all three—a financial platform uniting trading, products, and infrastructure.

Conclusion: From “Trading Gateway” to “Financial Operating System”

Robinhood is facing not just a growth challenge, but a structural transformation.

Short term:

Long term:

-

Revenue streams are more diversified

-

The Layer 2 strategy opens new horizons

-

Product innovation boosts user engagement

Robinhood is evolving from a “trading app” into a “financial operating system.”