The U.S. consumer market is vast, and credit-based spending has become an important part of the modern retail system. From everyday shopping to healthcare expenses, and from home improvement to electronics purchases, a large share of consumer activity depends on financing tools. Synchrony Financial provides financial services in these consumption scenarios and has gradually become one of the most representative companies in the U.S. consumer finance industry.

Synchrony Financial originally grew out of General Electric’s financial services system before becoming independently listed and focusing on the consumer finance market. Unlike traditional commercial banks, the company does not focus on corporate lending or investment banking. Instead, it has built its business system around consumer financing needs.

SYF is the ticker symbol under which Synchrony Financial trades on the New York Stock Exchange (NYSE). The company is headquartered in Connecticut, United States, and is an important participant in the U.S. consumer finance industry.

Today, Synchrony Financial has established partnerships with many retail brands, healthcare institutions, and service companies across the United States. Its financial products cover credit cards, consumer loans, installment payments, digital payments, and other areas. In the U.S. consumer finance market, SYF has built a strong market presence and brand influence.

What Are Synchrony Financial’s Revenue Sources?

Synchrony Financial’s revenue structure is mainly built around consumer credit. The company earns interest income by providing consumers with credit lines and financing services, while also supporting continued business growth through long-term relationships with retail partners.

Compared with traditional banks, SYF’s revenue depends more heavily on consumer activity and credit usage. When consumers continue using credit cards for purchases, choose installment payments, or apply for consumer loans, the company can earn revenue from the use of funds.

Overall, Synchrony Financial’s revenue sources mainly include the following areas:

| Revenue Source |

Main Content |

| Credit card interest income |

Interest generated from credit card balances |

| Consumer lending income |

Installment payments and financing services |

| Merchant partnership revenue |

Co-branded cards and retail partnership programs |

| Fee income |

Account services and related fees |

| Deposit business income |

Revenue related to certain financial products |

This revenue structure allows the company to benefit from both growth in consumer spending and the expansion of its partner ecosystem.

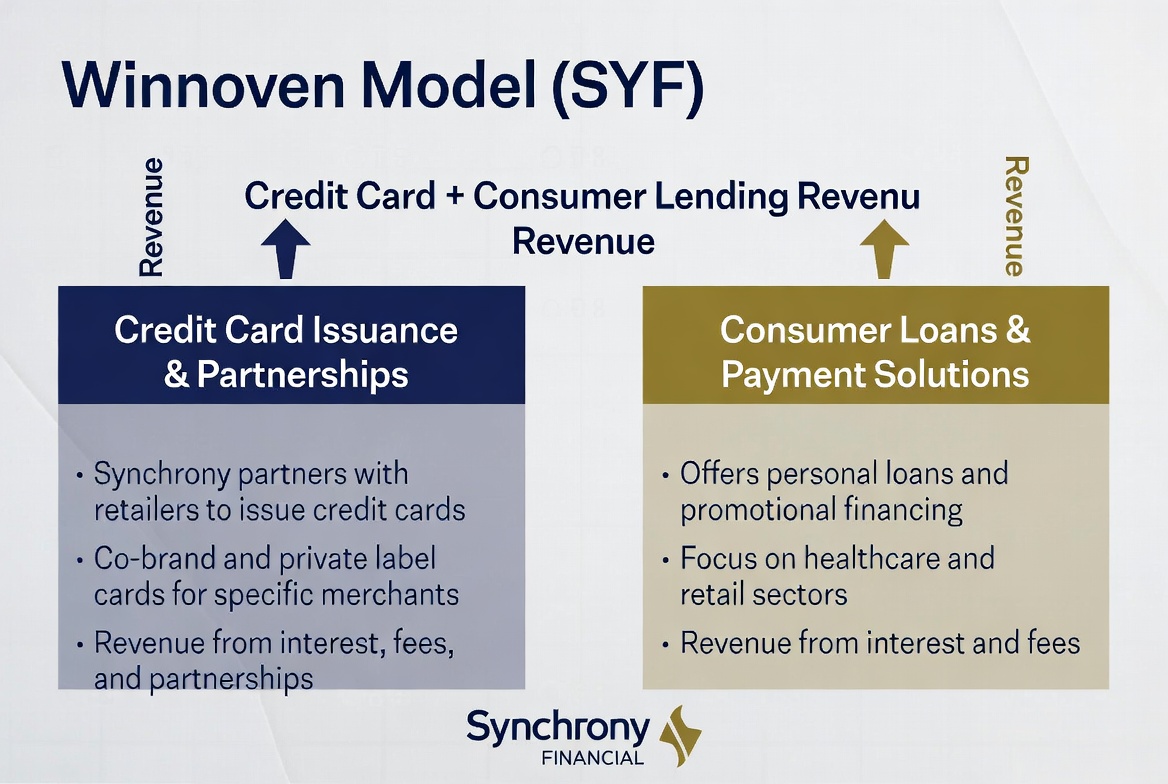

How the Credit Card Business Generates Revenue

Credit cards are one of Synchrony Financial’s most important revenue sources. Unlike many financial institutions, SYF focuses more on retail brand credit cards and co-branded credit cards, rather than simply issuing general-purpose credit card products.

When consumers shop with partner merchants, they can use credit cards provided by Synchrony to complete payment. If consumers do not repay the full balance within the billing cycle, interest charges arise, and this interest income becomes an important source of profit for the company. In addition, some credit card products may generate account management fees and related service revenue.

For merchants, credit card programs are not only payment tools, but also customer management tools. Through points rewards, membership benefits, and exclusive discounts, merchants can increase repeat purchase rates and purchase frequency. For Synchrony, this partnership model helps continuously expand its user base and create stable transaction flow.

The value of the credit card business does not come only from individual transactions. It also comes from the recurring revenue created when consumers use credit lines over time. For that reason, customer retention and activity are important drivers of business growth.

How Consumer Lending Services Contribute to Growth

In addition to credit cards, consumer lending services are another important growth engine for Synchrony Financial. Many high-value consumption scenarios are not well suited to a single upfront payment, which makes installment financing an important tool for supporting purchases.

Furniture purchases, home upgrades, medical care, auto repairs, and major electronics purchases are all typical use cases for consumer lending. Consumers can complete purchases earlier through financing plans and then repay the funds over an agreed period.

For merchants, consumer loans can lower payment barriers for consumers, helping increase transaction completion rates and average order value. For Synchrony Financial, growth in loan balances means more sources of interest income, so consumer lending has become an important part of the company’s revenue structure.

As consumer demand for flexible payment options increases, consumer lending services have gradually moved from being a supplementary tool to becoming an important part of the modern consumer finance ecosystem.

How the Retail Partner System Expands the Customer Base

Synchrony Financial’s retail partnership network is an important competitive advantage that sets it apart from traditional banks. The company has long focused on building partnerships with brands and retail companies, embedding itself into consumption scenarios through co-branded credit cards and financing services.

Under this model, consumers usually do not directly search for a financial institution. Instead, they encounter financial products offered by partner merchants during the shopping process. For example, when consumers make purchases at furniture stores, healthcare institutions, or electronics retailers, they may come across financing services supported by Synchrony.

This customer acquisition method is highly efficient. Merchants gain sales growth, consumers gain payment convenience, and Synchrony gains new financial customers. As the number of partners continues to grow, the company can cover more consumption scenarios and expand its market share.

The partnership network built over many years has become one of Synchrony Financial’s most important moats and a key driver of continued business expansion.

Why Risk Management Affects Profitability

The core challenge in consumer finance is not customer acquisition, but risk control. Because SYF provides credit lines to a large number of individual consumers, credit risk management directly determines the company’s profitability.

If default rates rise, the company must set aside more provisions for bad debts, which affects profit performance. Conversely, if the credit review system can effectively identify higher-risk customers, the company can improve asset quality and strengthen profitability. For this reason, risk management capability is viewed as one of the most important core competencies for consumer finance companies.

Synchrony Financial has long invested in data analytics and credit assessment systems, using consumer behavior data, credit records, and payment history to assess risk. This capability affects not only loan approval efficiency, but also long-term operating performance.

From an industry perspective, growth speed matters for consumer finance companies, but risk control often determines whether a company can maintain stable profitability over the long term. Risk management has therefore become an important part of Synchrony Financial’s business model.

How to Buy SYF (Synchrony Financial) Stock

SYF is the ticker symbol for Synchrony Financial, which is listed and traded on the New York Stock Exchange. Traditionally, investors can buy SYF through a securities account that supports U.S. stock trading, allowing them to participate in the development of the U.S. consumer finance industry.

Because Synchrony Financial’s business covers credit cards, consumer loans, and retail financial services, its operating performance is usually affected by consumer spending, interest rate levels, and consumer credit conditions. Many market participants regard SYF as one of the important companies for observing the U.S. consumer finance market.

As digital asset markets and traditional financial markets gradually converge, more trading tools linked to stock price movements have appeared in the market. For example, some platforms offer CFD products linked to stock prices, allowing users to participate in the market through price changes without directly holding the underlying stock assets.

Taking Gate TradFi as an example, users can follow different markets, including digital assets, stocks, ETFs, indices, and commodities, within the same account environment. Some markets also provide Gate CFD products, offering more options for cross-market asset allocation and price observation.

Regardless of how they participate in the market, investors should fully understand the product structure, trading rules, and regulatory requirements in their region.

Conclusion

Synchrony Financial’s business model is built on the consumer finance ecosystem. Through its credit card business, consumer lending services, and broad retail partner network, the company can continuously connect consumers and merchants while generating revenue from consumption activity. At the same time, risk management capability determines asset quality and profitability, making it an important source of Synchrony Financial’s long-term competitiveness. As digital payments and consumer finance continue to develop, SYF has become one of the most representative companies in the U.S. consumer finance market.

FAQs

What Businesses Does SYF Mainly Rely on to Make Money?

Synchrony Financial mainly earns revenue through credit card interest income, consumer lending income, and financial service programs carried out with retail partners.

Is Synchrony Financial a Bank?

Synchrony Financial provides certain banking functions, but its core positioning is as a consumer finance company, with a business focus on credit cards and consumer lending services.

Why Can the Credit Card Business Become a Major Revenue Source?

The credit card business can continuously generate interest income and related service revenue while maintaining high customer stickiness, making it an important profit source for consumer finance companies.

Why Is the Retail Partnership Model Important?

Retail partnerships allow Synchrony to directly access consumer spending scenarios, improving customer acquisition efficiency and expanding its customer base.

Why Does Risk Management Affect Consumer Finance Company Profits?

Credit risk directly determines bad debt levels. If default rates rise, companies must absorb more losses, so risk control capability affects overall profitability.

How Is Synchrony Financial Different from Capital One?

Synchrony Financial focuses more on retail finance partnerships and financing tied to consumer spending scenarios, while Capital One is a diversified financial institution with a broader business scope.