The stablecoin market has long suffered from a structural imbalance: issuers centrally capture reserve interest, while exchanges and payment platforms drive circulation without receiving proportional incentives. USDC and USDT dominate market share, yet their yield distribution logic remains issuer-centric. Launched in November 2024, the Global Dollar Network (GDN) aims to restructure this relationship through a networked collaboration model.

From a blockchain and digital asset perspective, all three are composable assets with a 1:1 dollar peg on-chain, interchangeable across DeFi, payments, and treasury use cases. Their key differences lie in off-chain issuance governance, reserve yield attribution, and regulatory transparency—not in technical standards or peg mechanisms.

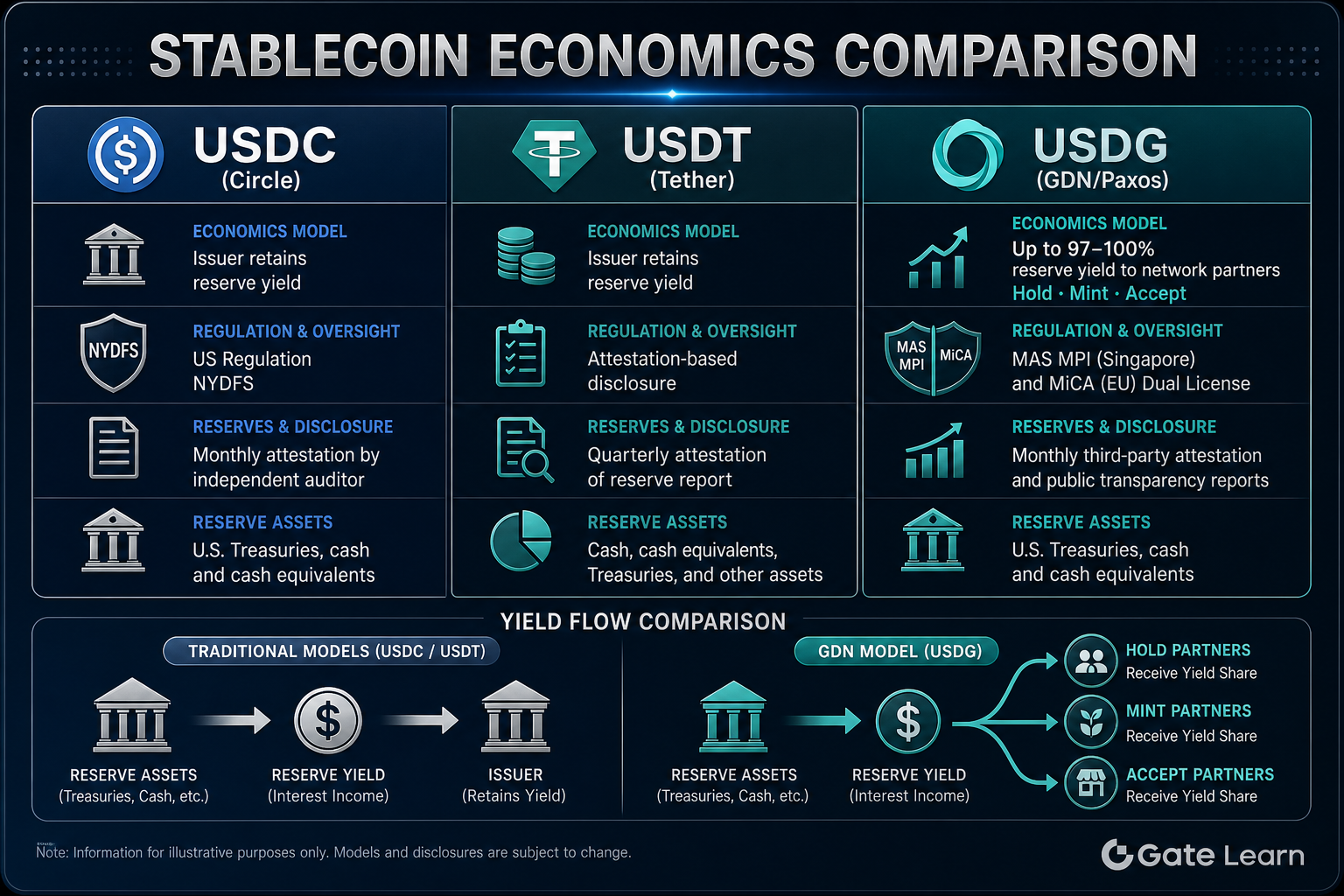

What Is the Stablecoin Economics Model of USDC/USDT?

USDC is issued by Circle, and USDT by Tether Limited. Both follow a standard path: the issuer mints tokens after dollars are deposited, reserves are custodied, tokens circulate on-chain, and are burned upon redemption. Users or institutions deposit dollars into the issuer's designated account, and the issuer mints an equivalent amount of stablecoins on-chain; when redeemed, tokens are burned and dollars returned.

Reserve assets typically include cash, short-term Treasury bills, and money market instruments, held at banks or custodians. Under both USDC and USDT models, the interest generated by reserves (reserve yield) is primarily retained by Circle and Tether as issuers, covering operating costs, compliance expenses, and business returns. Exchanges, wallets, or merchants that hold or promote large amounts of USDC/USDT generally do not automatically receive a systematic revenue share tied to reserve size—unless separate commercial agreements exist.

This model features a simple structure and centralized decision-making, enabling rapid scaling. However, its limitation is the mismatch between adoption drivers and reserve yield: platforms struggle to receive proportional incentives from reserve returns. USDC is primarily governed by frameworks such as NYDFS and undergoes periodic attestations. USDT discloses reserves through attestations, with a regulatory path that differs from Circle's.

What Is the Stablecoin Economics Model of USDG/GDN?

USDG (Global Dollar) is issued by Paxos Digital Singapore (MAS MPI license) and Paxos Issuance Europe (MiCA framework), with reserves consisting of cash and cash equivalents held in segregated accounts. Like USDC and USDT, USDG supports 1:1 dollar minting and redemption, and ordinary on-chain holders do not directly receive reserve interest.

The Global Dollar Network (GDN) defines the network rules and yield distribution framework on top of Paxos's issuance layer. Approved enterprise partners participate through three roles: Hold, Mint, and Accept. Hold refers to platforms maintaining USDG balances, Mint refers to contributing incremental supply to circulation, and Accept refers to accepting USDG as a payment or deposit method. GDN directs a distributable portion of reserve yield toward these network partners—up to approximately 97%–100%. Exact percentages and role contributions are governed by the network protocol and partner agreements.

This model shifts stablecoin economics from "issuer-exclusive yield" to "yield sharing with adoption drivers." Platforms can access USDG under Paxos's existing MAS and MiCA compliance frameworks without needing to independently obtain a stablecoin license, and they earn returns tied to reserve size or traffic through their GDN roles. Ordinary users still retain the right to 1:1 redemption but do not participate in reserve yield sharing.

Who Gets the Reserve Yield for USDC, USDT, and USDG? A Table Shows Key Differences

The table below compares the economic structures of the three stablecoins across yield distribution, participation thresholds, and holder rights:

| Dimension |

USDC |

USDT |

USDG (GDN) |

| Issuer |

Circle |

Tether |

Paxos (MAS MPI / MiCA) |

| Primary recipient of reserve yield |

Issuer (Circle) |

Issuer (Tether) |

GDN network partners (up to ~97%–100%) |

| Default revenue share for platforms |

None |

None |

Yes (Hold/Mint/Accept roles) |

| Reserve interest for ordinary holders |

Not directly received |

Not directly received |

Not directly received |

| Adoption incentive structure |

Issuer-centric |

Issuer-centric |

Networked partner sharing |

Figure 1. Comparison of stablecoin economic models: USDC/USDT issuer-retained yield vs. USDG GDN partner yield sharing mechanism.

Figure 1. Comparison of stablecoin economic models: USDC/USDT issuer-retained yield vs. USDG GDN partner yield sharing mechanism.

The yield attribution comparison table shows that differences between USDC and USDT are more about issuer identity and disclosure pathways, with both sharing the same economic model of issuer-retained reserve yield. USDG, under the same 1:1 peg and Paxos compliant issuance, redirects reserve returns through GDN to network partners that drive adoption. For institutions, choosing USDG to participate in the GDN partner yield mechanism means potentially receiving reserve-related revenue shares. For ordinary users, all three provide on-chain dollar pegs and redemption rights, but none directly distribute reserve interest.

How Do Regulatory and Transparency Aspects Differ Among USDC, USDT, and USDG?

USDC's issuance and reserve management are governed by U.S. state money transmitter licenses and frameworks such as NYDFS. Circle regularly publishes reserve attestations and composition disclosures. USDT is issued by Tether, which reports reserve balances and composition through attestation reports. Its regulatory path and disclosure standards differ from Circle's, and market commentary on its transparency has historically been a topic of discussion.

USDG uses a dual-entity, dual-license structure: Paxos Digital Singapore holds a Major Payment Institution license from MAS, and Paxos Issuance Europe is supervised by FIN-FSA in Finland under the EU MiCA framework. Reserves are custodied primarily with DBS Bank, and Paxos publishes monthly reserve reports with independent third-party attestations.

| Dimension |

USDC |

USDT |

USDG |

| Issuer |

Circle |

Tether |

Paxos (Singapore + Europe dual entity) |

| Primary regulatory framework |

U.S. NYDFS, etc. |

Multi-jurisdiction, attestation disclosure |

MAS MPI + MiCA |

| Reserve type |

Cash and eligible assets |

Cash, Treasuries, etc. (per disclosure) |

100% cash and cash equivalents |

| Disclosure method |

Periodic attestation |

Periodic attestation |

Monthly report + independent attestation |

| Custodian bank |

Multiple partner banks |

Per disclosure |

DBS (primary banking partner) |

The regulatory and transparency comparison shows that all three provide varying degrees of reserve disclosure under a 1:1 redemption commitment, but with different compliance paths and supervisory bodies. USDG's dual MAS MPI and MiCA license setup aligns with Paxos's existing compliance infrastructure in Singapore and Europe. The comparison between USDG, PYUSD, and USDP further illustrates differences in issuance entities and regulatory jurisdictions within the Paxos stablecoin ecosystem. Circle and Tether each rely on U.S. and global operating frameworks. Users and institutions must evaluate based on their jurisdiction, disclosure preferences, and compliance requirements—not using circulation size as the sole criterion.

Which Use Cases Are Best Suited for USDC, USDT, and USDG?

USDC is widely used in DeFi protocols, institutional custody, and cross-border settlements, with mature ecosystem integrations on Ethereum and multiple chains. It suits scenarios requiring high liquidity and broad protocol support. USDT holds a significant position in centralized exchange trading pairs and liquidity in Asia and emerging markets, making it suitable for scenarios demanding deep liquidity and cross-platform transfers.

USDG is better suited for enterprise-level participants who want to drive business with a compliant stablecoin while earning reserve yield through GDN roles. Exchanges can simultaneously take on Hold, Mint, and Accept roles, earning network returns from holding balances, minting increments, and inbound deposit flows. Payment gateways and merchant platforms can use the Accept role to incentivize USDG deposits. For ordinary users who only need an on-chain dollar-pegged asset for transfers or DeFi interactions, all three meet basic needs, but USDG's ecosystem breadth depends on the continued expansion of the GDN partner network.

Scenario differences depend on the participant's role: when institutions evaluate GDN partner sharing and MAS/MiCA compliance paths, USDG offers differentiated value. For individual users prioritizing liquidity and chain support, the existing ecosystem coverage of USDC and USDT still holds advantages.

Summary

USDG, USDC, and USDT are all 1:1 dollar-pegged stablecoins with similar on-chain functionality, but with significant differences in stablecoin economics and regulatory structures. USDC is issued by Circle, USDT by Tether, with reserve yield primarily retained by the issuers. USDG is issued by Paxos under the MAS MPI and MiCA frameworks, and GDN distributes up to approximately 97%–100% of reserve yield to Hold, Mint, and Accept network partners. Ordinary holders do not directly receive reserve interest. Institutional participants should choose based on yield sharing, compliance path, and ecosystem integration needs.

FAQ

What is the biggest difference between USDG and USDC/USDT?

The biggest difference is the reserve yield distribution model. The reserve interest from USDC and USDT is primarily retained by Circle and Tether. USDG, through the Global Dollar Network (GDN), distributes up to approximately 97%–100% of reserve yield to approved network partners. Ordinary holders do not directly receive reserve interest.

Can ordinary users holding USDG receive reserve interest?

No. The USDG whitepaper specifies that ordinary on-chain holders do not directly receive interest generated by reserves. Reserve yield distribution is directed to approved Hold, Mint, and Accept partners within the GDN. Holders retain the right to 1:1 dollar redemption but do not participate in reserve return sharing.

Who receives the reserve yield from USDC and USDT?

USDC's reserve yield is primarily retained by Circle as the issuer. USDT's reserve yield is primarily retained by Tether as the issuer. Exchanges or platforms that facilitate USDC/USDT circulation generally do not automatically receive a systematic revenue share tied to reserve size.

How does USDG's regulatory framework differ from USDC and USDT?

USDG is issued by a dual entity—Paxos Digital Singapore (MAS MPI license) and Paxos Issuance Europe (MiCA framework)—with reserves custodied by DBS and subject to periodic attestations. USDC is primarily governed by frameworks such as NYDFS in the U.S. USDT is issued by Tether, which discloses reserves through attestations, with a regulatory path that differs from Circle's.

How do GDN network partners earn reserve yield?

Approved enterprise partners in GDN participate through Hold, Mint, and Accept roles: they receive reserve yield shares based on USDG balances held (Hold), minting volume (Mint), or inbound traffic (Accept), with potential shares up to approximately 97%–100%. The exact percentages and access conditions are governed by the GDN network protocol and partner agreements.

Can the three stablecoins be used interchangeably in DeFi?

All three are 1:1 dollar-pegged assets under ERC-20 and similar standards on-chain, usable within supported DeFi protocols, wallets, and cross-chain bridges. Differences lie in issuance governance, reserve yield attribution, and regulatory transparency. Before use, verify the contract is the official deployment on the target chain.