The on-chain lifecycle of the U.S. Dollar Payment Token (USDPT)—from mint to burn—is fully controlled by Anchorage Digital Bank, N.A. The overall architecture is defined through three lenses: the division of labor between Anchorage Digital Bank and Western Union, the Solana contract standard, and the Digital Asset Network use case. Western Union Stablecoin USDPT describes the framework from three aspects. Western Union integrates USDPT into its global payments and Digital Asset Network, but the token's credit foundation and reserve assets belong to the issuing bank, not Western Union.

To understand USDPT's issuance mechanism, three distinct roles must be separated: who holds the reserves, who runs the mint and burn, and who handles distribution and cash-out. In cross-border payments, on-chain settlement speed and traditional fiat delivery often involve different parties. USDPT's design explicitly splits bank-grade issuance from Western Union's global agent network as complementary modules.

What Is Anchorage Digital Bank?

Anchorage Digital Bank, N.A. is a federally chartered national trust bank regulated by the U.S. Office of the Comptroller of the Currency (OCC). It is one of the first U.S. bank institutions to secure a federal banking charter for digital asset operations. Within the USDPT framework, Anchorage Digital Bank acts as the sole on-chain issuer, handling SPL token minting, redemption, and end-to-end management of the corresponding U.S. dollar reserves.

| Attribute |

Description |

| Regulatory Status |

OCC-chartered federal national trust bank |

| Issuance Function |

USDPT minting, burning, and reserve management |

| On-Chain Deployment |

Solana SPL Token standard |

| Contract Address |

HVWf8JmLoHs99Lw8Psf3fyqAtA4crWxCPkrmSdNjhNH3 |

| Reserve Model |

Full 1:1 U.S. dollar reserves (no fractional backing) |

The table above captures Anchorage Digital Bank's core role in the USDPT system. A federal banking charter means issuance must satisfy stringent regulatory requirements—capital adequacy, risk management, AML, and KYC—creating a structural distinction from stablecoins issued by pure on-chain protocols or unlicensed entities.

The broader Anchorage Digital group also operates institutional services in trading, custody, and settlement. However, USDPT's issuance and reserve accounts are held by the banking entity Anchorage Digital Bank, N.A., with reserve assets kept separate from Western Union's balance sheet. USDPT vs USDC vs USDT shows the structural differences in issuing entity, chain coverage, and cash-out paths.

How Is Minting Triggered?

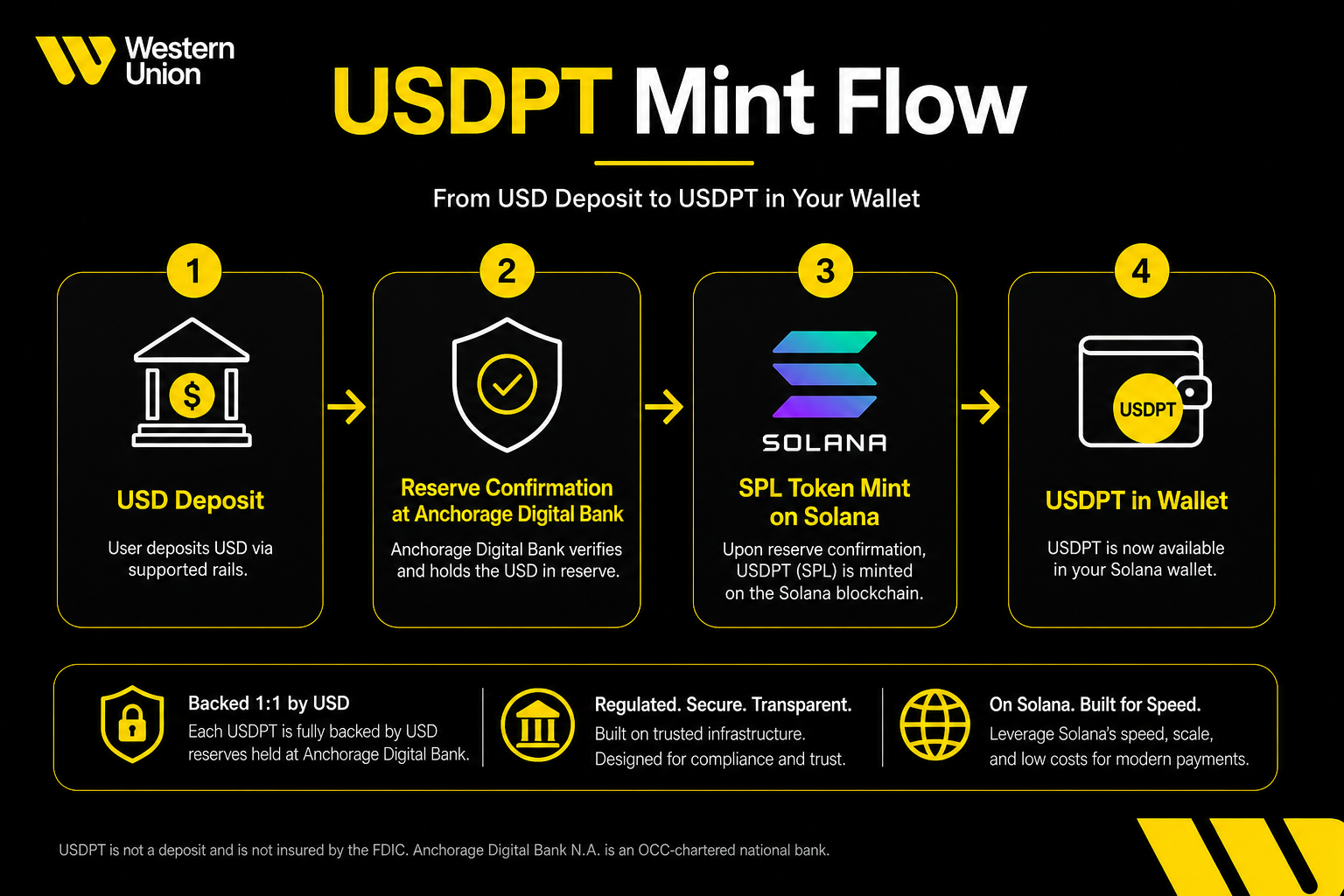

USDPT minting follows a "reserves first, then on-chain" principle: Anchorage Digital Bank executes a Solana mint only after confirming receipt of an equivalent amount of U.S. dollars, ensuring the on-chain circulating supply mirrors bank reserves at a 1:1 ratio.

A typical minting path involves four stages. Stage one: An eligible participant—such as a partner exchange, institutional client, or authorized party—submits a U.S. dollar deposit or equivalent settlement instruction to Anchorage Digital Bank. Stage two: The bank completes KYC/AML checks, confirms fund receipt, and credits the reserve account. Reserve assets primarily include bank demand deposits, U.S. Treasury bills, and similar highly liquid cash equivalents. Stage three: Anchorage Digital Bank calls the mint instruction via its controlled Solana issuance program, generating new SPL tokens at contract address HVWf8JmLoHs99Lw8Psf3fyqAtA4crWxCPkrmSdNjhNH3. Stage four: The newly minted USDPT is transferred to the requester's specified Solana address, increasing the total on-chain supply.

| Stage |

Executing Entity |

Key Action |

| 1. Deposit Request |

Eligible Participant |

Submit USD deposit and compliance materials |

| 2. Reserve Confirmation |

Anchorage Digital Bank |

KYC/AML review, USD credited |

| 3. On-Chain Minting |

Anchorage Digital Bank |

Solana mint program executed |

| 4. Token Delivery |

Anchorage Digital Bank |

SPL tokens sent to designated address |

Minting is triggered only after bank-side reserve confirmation—not by creating tokens on-chain first and backfilling reserves later. This sequencing aligns with the full-reserve model: for every new USDPT in circulation, the issuer must hold $1 in equivalent assets in the reserve account. Solana's high throughput and low latency enable minting to occur quickly after reserve confirmation, making it well-suited for the high-frequency, low-value settlement typical of payment stablecoins.

Figure 1. USDPT minting process: After USD deposit reserve confirmation by Anchorage Digital Bank, SPL tokens are minted on Solana.

Figure 1. USDPT minting process: After USD deposit reserve confirmation by Anchorage Digital Bank, SPL tokens are minted on Solana.

Western Union can guide users to acquire USDPT during distribution—for instance, via partner exchanges or the Digital Asset Network. But on-chain minting authority and reserve crediting remain solely with Anchorage Digital Bank; Western Union does not directly call the Solana issuance program. The path from USDPT minting to agent cash-out outlines a four-stage repeatable route from exchange acquisition to fiat delivery at agent locations.

How Does Redemption Correspond to Reserve Release?

USDPT redemption is the reverse of minting: on-chain token burning and USD reserve release must occur simultaneously to maintain the 1:1 peg. USDPT reserves and the 1:1 peg details the verification approach across reserve asset types, on-chain circulating supply, and redemption channels.

Redemption typically follows these steps. Step one: The holder submits a redemption request to Anchorage Digital Bank or its authorized access point, specifying the amount of USDPT to be destroyed and the receiving bank account. Step two: The bank verifies the applicant's identity and token source, confirming that the on-chain USDPT has been transferred to the issuer's burn address or that the burn instruction has been executed. Step three: The corresponding amount of SPL tokens is permanently destroyed on Solana, reducing the total on-chain supply. Step four: Anchorage Digital Bank releases an equivalent amount of U.S. dollars from the reserve account to the applicant's designated bank account, completing the 1:1 redemption. The burn must occur before or simultaneously with the reserve release; the bank will not release reserves early while on-chain tokens remain outstanding.

Users can also cash out USDPT into local fiat at agent locations through Western Union's Digital Asset Network. This path involves Western Union's distribution and compliance network, but the ultimate responsibility for on-chain burn and reserve release remains with Anchorage Digital Bank.

Division of Responsibilities: Issuer vs. Western Union

In the USDPT ecosystem, Anchorage Digital Bank and Western Union perform distinctly different functions. Confusing the two roles is one of the most common misunderstandings about this stablecoin.

| Dimension |

Anchorage Digital Bank |

Western Union |

| Issuer? |

Yes, sole on-chain issuer |

No, not an issuer |

| Reserve Management |

Holds and manages USD reserves |

Does not handle USDPT reserves |

| On-Chain Mint/Burn |

Executes minting and burning |

Does not control the issuance program |

| Distribution & Cash-Out |

Indirect participation via authorized access points |

Digital Asset Network, global agent locations |

| Compliance Responsibilities |

Bank-level AML/KYC, OCC regulation |

Remittance compliance, country licenses, risk control |

| Application Scenarios |

Reserve and redemption infrastructure |

Exchange integration, agent cash-out, remittance collection |

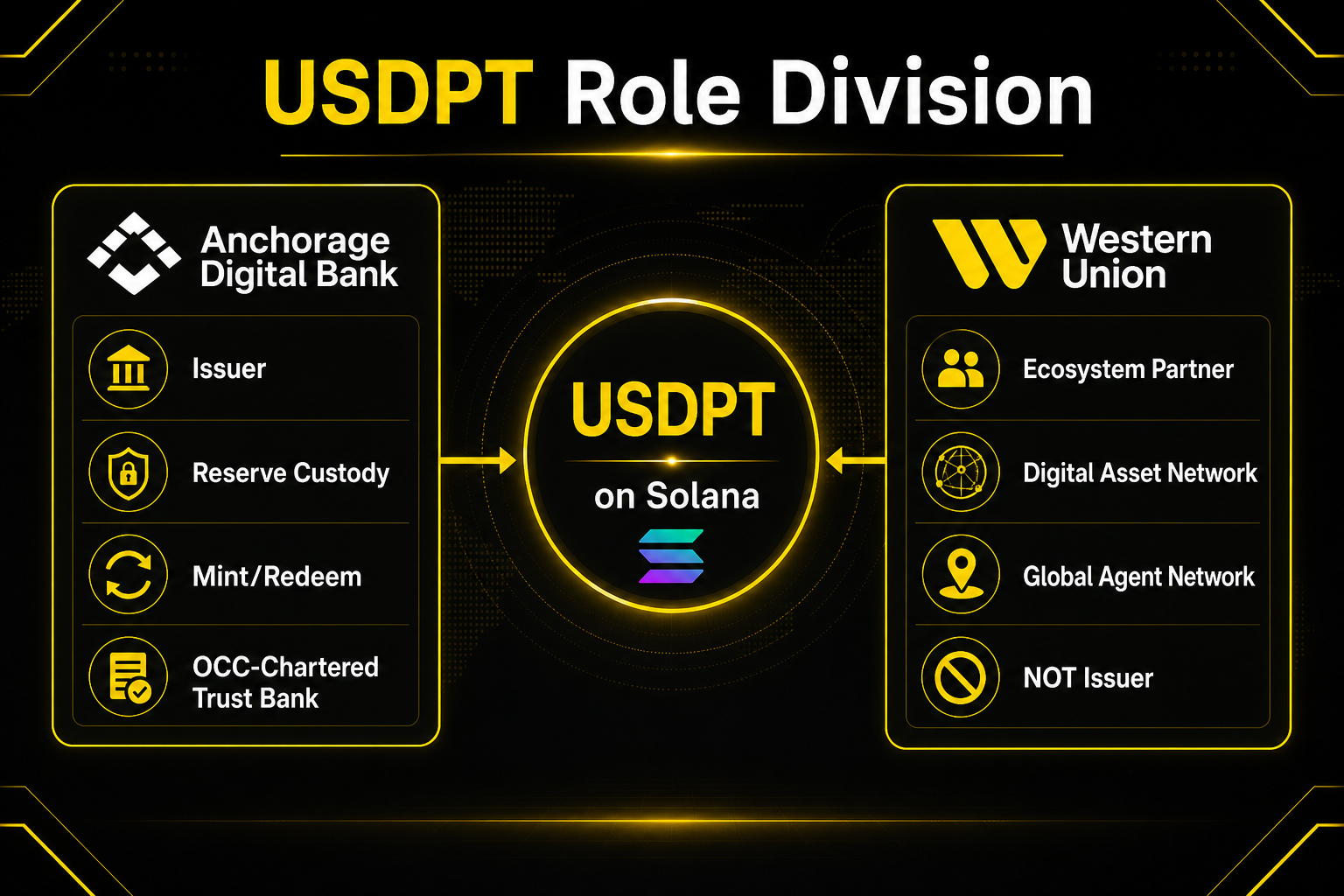

Anchorage Digital Bank provides the "token credit foundation": reserve assets, mint/burn authority, and the federal banking regulatory framework. Western Union provides the "value delivery network": connecting on-chain USDPT to agent systems in over 200 countries and territories, partner exchanges, and remittance products. Western Union uses USDPT for agent settlement, treasury operations, and consumer product plans like Stable by Western Union—but the token's issuance and reserve lifecycle remain outside Western Union's control.

This division mirrors a traditional finance "issuer–distributor" structure: a bank issues certificates of deposit or money market shares, and a third-party platform handles sales and redemption. USDPT replaces the issuer with a federally chartered bank and the distribution network with Western Union's global payment infrastructure.

Figure 2. USDPT role division: Anchorage Digital Bank serves as issuer and reserve manager; Western Union handles distribution and global cash-out network.

Figure 2. USDPT role division: Anchorage Digital Bank serves as issuer and reserve manager; Western Union handles distribution and global cash-out network.

What Responsibilities Does the Issuer Bear Under the Regulatory Framework?

As an OCC-chartered bank, Anchorage Digital Bank assumes multiple regulatory and operational duties in USDPT issuance and management. These obligations form the institutional backbone of the token's credibility.

Reserves and Capital: The issuer must maintain full USD reserves equal to the circulating USDPT and meet OCC requirements for capital adequacy, liquidity coverage, and asset quality. Reserve asset selection (deposits, Treasury bills, cash equivalents) must follow bank asset management standards.

Issuance and Redemption Operations: From deposit confirmation to mint execution, and from burn confirmation to reserve release, the entire process must have auditable operating procedures and internal controls. Changes in on-chain supply and off-chain reserves should be cross-verifiable.

Compliance and Risk Management: The bank must perform AML, KYC, sanctions screening, and suspicious transaction reporting. All access parties involved in minting and redemption must fall within the bank's compliance framework. Anchorage Digital Bank must also follow OCC risk management guidelines for digital asset operations.

Information Disclosure: Reserve composition, circulating supply, and audit-related information depend on periodic disclosure by the issuer. The supply at the on-chain contract address HVWf8JmLoHs99Lw8Psf3fyqAtA4crWxCPkrmSdNjhNH3 is publicly queryable and can be compared with disclosed reserve figures.

It is critical to note that OCC bank regulation does not mean USDPT is guaranteed by the U.S. government. USDPT is not protected by FDIC deposit insurance, nor is it backed by the Department of the Treasury or the Federal Reserve. "Issued under federal bank regulation" and "government credit guarantee" are two separate concepts. The issuer's regulatory obligations address "who supervises reserves and operations"—not "the token is equivalent to U.S. dollar cash."

Summary

The issuance and management of the U.S. Dollar Payment Token (USDPT) are executed by Anchorage Digital Bank, N.A. on Solana, while Western Union handles ecosystem distribution and the global cash-out network. The core mechanism can be summarized as: after USD deposit confirmation, SPL tokens are minted 1:1; upon redemption, on-chain tokens are burned and equivalent reserves are released; the issuer holds full USD reserves under OCC bank regulation; Western Union is not the issuer; USDPT is not FDIC-insured or U.S. government-guaranteed. When evaluating USDPT, examine the bank's reserves and mint/burn mechanism, Solana on-chain contract risk, and the compliance and operational conditions of the chosen acquisition and cash-out channels separately.

FAQ

Is Anchorage Digital Bank the issuer of USDPT?

Yes. Anchorage Digital Bank, N.A. is the sole on-chain issuer of USDPT, responsible for minting, redemption, and USD reserve management. Western Union is an ecosystem participant handling Digital Asset Network distribution and global cash-out but does not directly mint on-chain tokens.

What conditions are required for USDPT minting?

Minting requires Anchorage Digital Bank to confirm receipt of an equivalent amount of USD first. Eligible participants complete KYC/AML checks and deposit funds; the bank then executes mint via the Solana issuance program, and new tokens are sent to the designated address. For each new USDPT, the reserve account must hold $1 in equivalent assets.

How are reserves released during USDPT redemption?

On redemption, Anchorage Digital Bank verifies identity and executes an on-chain burn, destroying the corresponding SPL tokens, then releases an equivalent amount of USD from the reserve account to the applicant's account. The decrease in on-chain supply and the reserve release must maintain a 1:1 correspondence.

Can Western Union directly mint USDPT?

No. Western Union is not the USDPT issuer and does not control the Solana mint program or reserve accounts. Western Union participates in distribution and cash-out through the Digital Asset Network, partner exchanges, and agent locations; on-chain issuance authority belongs to Anchorage Digital Bank.

What is the Solana contract address for USDPT?

The USDPT contract address on Solana is HVWf8JmLoHs99Lw8Psf3fyqAtA4crWxCPkrmSdNjhNH3. Always verify the address and token symbol before on-chain operations to avoid confusion with counterfeit tokens.

Is USDPT protected by FDIC deposit insurance?

No. USDPT is not a bank deposit, is not FDIC-insured, and is not guaranteed by the U.S. Department of the Treasury or the Federal Reserve. Its value is backed by the USD reserve assets held by Anchorage Digital Bank and the OCC banking regulatory framework.