With the development of Telegram and the TON ecosystem, an increasing number of users are beginning to engage with on-chain financial services. However, most traditional DeFi products are primarily concentrated on Ethereum and its scaling networks, typically requiring wallet management, cross-chain operations, and complex interaction processes. EVAA’s emergence lowers the barrier for TON users to participate in DeFi, integrating lending services directly into the Telegram experience.

Lending markets are often the most liquidity-efficient component within DeFi ecosystems, and EVAA provides money market support for stablecoins, liquid staking assets, and other digital assets on the TON network, driving improved capital efficiency across the entire ecosystem.

Origins and Development Background of EVAA Protocol

TON was initially designed to build blockchain infrastructure for mass adoption, leveraging Telegram’s vast user base to promote Web3 application adoption. As the TON network gradually formed a complete application ecosystem, market demand for financial infrastructure such as lending, trading, and yield aggregation continued to grow.

EVAA was born in this context, with the goal of establishing a native lending market within the TON network, providing users with secure, efficient, and easy-to-use on-chain financial services. Compared to solutions that rely on external bridges or cross-chain assets, EVAA focuses more on serving TON-native assets and ecosystem participants.

How EVAA Protocol’s Lending Mechanism Works

EVAA operates using a liquidity pool model, rather than a peer-to-peer lending model. Once users deposit assets, the funds enter a common liquidity pool managed by the protocol.

After depositors supply funds to the liquidity pool, they can earn interest based on market borrowing demand. Borrowers, on the other hand, must first deposit collateral of a certain value before they can borrow other assets from the protocol.

The protocol mitigates default risk through an overcollateralization mechanism. For example, a user who deposits $1,000 in collateral may only borrow around $700 in value. The specific loan-to-value ratio is determined by asset risk parameters.

Interest rates are not fixed but fluctuate dynamically based on capital utilization. When borrowing demand increases, borrowing rates rise and deposit yields also increase, encouraging more liquidity to enter the market.

Core Components of EVAA Protocol

Liquidity Pool

The liquidity pool is EVAA’s fund source. All deposited assets are stored collectively in the pool, providing liquidity for borrowing needs.

Depositors

Depositors supply assets to the protocol and earn corresponding yields. The primary source of yield is the interest paid by borrowers.

Borrowers

Borrowers obtain liquidity by pledging digital assets without needing to sell their holdings. This model is widely used in DeFi capital management and leverage strategies.

Risk Management Module

The risk management system monitors collateral ratios, market price fluctuations, and asset health. When a position’s risk exceeds a safety threshold, the system triggers a liquidation process.

Oracle System

The oracle provides on-chain asset price data to the protocol, serving as the basis for calculating borrowing limits and making liquidation decisions.

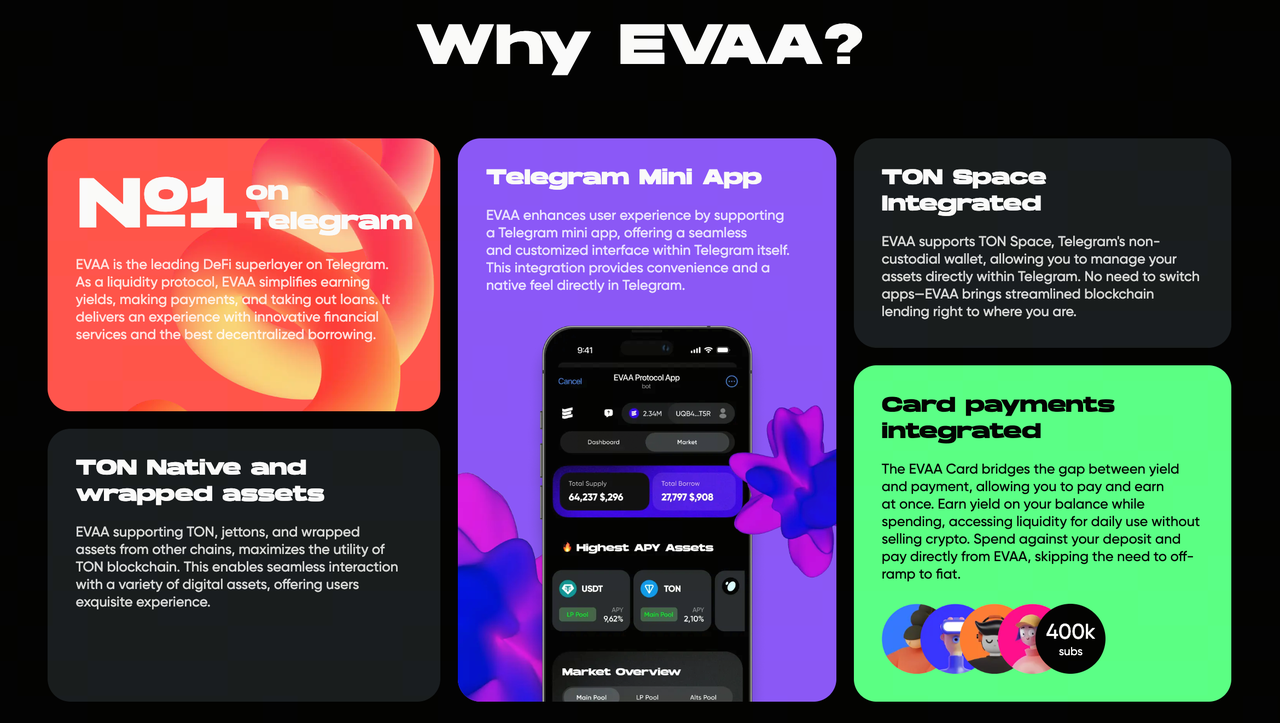

How EVAA Is Deeply Integrated with Telegram and TON

Telegram is regarded as one of the largest user-base social platforms in the Web3 space, while TON serves as its blockchain infrastructure.

A key feature of EVAA is embedding DeFi services directly into the Telegram user experience. Users can perform lending operations through the Telegram Mini App without needing to visit complex web applications.

This model differs significantly from traditional DeFi products. Users in the Ethereum ecosystem typically need to install separate wallets, connect to multiple apps, and pay higher network fees, whereas the integration of TON and Telegram simplifies the process.

For users new to blockchain financial products, EVAA offers an experience closer to Web2 applications.

What Is the Role of the EVAA Token

The EVAA Token is a key component of the protocol ecosystem, primarily serving governance and incentive functions.

Protocol Governance

Token holders can participate in protocol governance, voting on risk parameters, asset support ranges, and future development directions.

Community Participation Incentives

The protocol uses token incentives to encourage users to contribute to ecosystem growth, including providing liquidity, participating in governance, and providing long-term support for network development.

Protocol Revenue Distribution

Part of the protocol’s value may be returned to ecosystem participants through governance decisions, thereby forming a long-term incentive mechanism.

Foundation for DAO Development

One of EVAA’s long-term goals is to gradually transition to community governance, enabling key decisions to be driven by a decentralized autonomous organization (DAO).

Main Use Cases of EVAA in the TON Ecosystem

Stablecoin Lending

Users can utilize stablecoins to obtain liquidity or earn deposit yields, offering more options for capital management.

On-Chain Liquidity Management

Investors can access funds without selling their assets, thereby maintaining market exposure.

Yield Optimization Strategies

Lending protocols often serve as the underlying building blocks for yield aggregators, leveraged staking, and other DeFi strategies.

TON Financial Infrastructure

EVAA provides money market support for other applications within the TON network, facilitating the circulation of assets within the ecosystem.

How EVAA Differs from Other DeFi Lending Protocols

| Dimension |

EVAA |

Aave |

Compound |

| Underlying Network |

TON |

Ethereum & Multi-Chain |

Ethereum |

| User Entry |

Telegram + Web App |

Web3 Wallet |

Web3 Wallet |

| Core Users |

Telegram Ecosystem Users |

DeFi Users |

DeFi Users |

| Asset Base |

TON-Native Assets |

Multi-Chain Assets |

Ethereum Assets |

| Ecosystem Positioning |

TON Financial Infrastructure |

General-Purpose Lending Market |

General-Purpose Lending Market |

Compared to Aave and Compound, EVAA’s biggest differentiator is not innovation in lending logic, but its deep integration with Telegram and TON.

This design makes EVAA more accessible to a broad base of mainstream users, rather than being limited to crypto-native users familiar with DeFi processes.

Potential Risks and Limitations of EVAA

All DeFi lending protocols face certain risks, and EVAA is no exception.

First is liquidation risk. When the price of collateral assets declines, a borrower’s position may be automatically liquidated.

Second is smart contract risk. Even after an audit, there may still be potential vulnerabilities or unforeseen issues in the code.

Third is liquidity risk. During periods of high market volatility, the liquidity pool may face short-term capital pressure.

Additionally, the stage of TON ecosystem development and asset diversity can also affect the lending market scale and capital efficiency.

Summary

EVAA Protocol is an important lending infrastructure within the TON ecosystem, building a decentralized money market through liquidity pools, overcollateralization, and dynamic interest rate mechanisms. The protocol not only provides lending functions but also offers liquidity support for stablecoin circulation, yield strategies, and on-chain financial activities.

Compared to traditional DeFi lending protocols, EVAA’s most distinctive feature is its Telegram-native experience. Leveraging the Telegram Mini App, TON Connect, and the TON blockchain infrastructure, EVAA is lowering the technical barrier for ordinary users to access DeFi and driving further integration between social networks and on-chain finance.

FAQs

Is EVAA a centralized platform?

EVAA is a decentralized finance (DeFi) protocol. User assets are managed by smart contracts, and the lending process is executed through on-chain rules rather than being controlled by a centralized entity.

Why did EVAA choose the TON network?

TON offers high performance, low cost, and deep integration with Telegram. By choosing TON as its infrastructure, EVAA can more conveniently serve the Telegram user base and promote DeFi adoption.

Does EVAA lending require collateral?

EVAA uses an overcollateralized lending model. Borrowers must first provide a sufficient value of collateral assets before they can borrow other digital assets.

What is the use of the EVAA Token?

The EVAA Token is primarily used for protocol governance, community incentives, ecosystem participation, and DAO decision-making. Holders can vote on important protocol parameters and development directions.

What is the difference between EVAA and Aave?

Both EVAA and Aave are DeFi lending protocols, but EVAA primarily serves the TON and Telegram ecosystems, whereas Aave targets the Ethereum and multi-chain DeFi market. EVAA emphasizes social entry points and a Telegram-native user experience.