Cross-border remittances have long depended on intermediaries like correspondent banks and SWIFT, with settlements restricted by business hours and holidays. Payment stablecoins enable round-the-clock transfers on public blockchains, while Western Union offers global agent networks, compliance checks, and local fiat cash-out capabilities. USDPT is positioned as a hybrid structure: "federally chartered bank issuance + Solana public chain + Western Union global cash-out network."

Within the Solana payment stablecoin ecosystem, USDPT, USDC, and USDT all claim a dollar peg, but differ in issuer, regulatory approach, and offline cash-out channels. USDPT vs USDC vs USDT provides a horizontal comparison across three dimensions: issuer, chain coverage, and cash-out path.

What Is USDPT and How Does It Relate to the U.S. Dollar and Stablecoins?

USDPT stands for U.S. Dollar Payment Token. On-chain, it exists as an SPL token with a nominal 1:1 peg to the U.S. dollar. It is a payment-type dollar stablecoin, not a yield-seeking or governance token.

Dollar stablecoins use on-chain tokens to represent off-chain dollar value. USDPT's distinction lies in its issuer—Anchorage Digital Bank, N.A., an OCC-chartered institution—and its integration with the Western Union global remittance and cash-out network.

| Concept |

Meaning |

Relationship to USDPT |

| U.S. Dollar (USD) |

Federal legal tender of the United States |

USDPT reserves and redemptions are denominated in USD |

| Stablecoin |

On-chain token pegged to a fiat currency or asset |

USDPT is a dollar payment stablecoin |

| Payment Token |

Token type focused on transfers and settlements |

The "Payment Token" in USDPT's name emphasizes its payment use case |

The table above distinguishes three layers: the dollar serves as the reserve denomination unit, stablecoin represents the technical form, and payment token highlights cross-border transfer and settlement use.

Who Issues USDPT? How Do Western Union and Anchorage Digital Bank Collaborate?

The on-chain issuer of USDPT is Anchorage Digital Bank, N.A., a federal national trust bank chartered by the Office of the Comptroller of the Currency (OCC). Anchorage Digital Bank handles minting and redemption of USDPT and manages the corresponding dollar reserve assets. Anchorage Digital Bank issues USDPT focuses on mint/burn authority, reserve confirmation, and redemption release, forming the on-chain credit foundation. Western Union does not act as the token issuer directly but serves as an ecosystem partner providing global distribution, compliance, risk management, and offline cash-out networks.

| Role |

Entity |

Core Function |

| Issuer |

Anchorage Digital Bank, N.A. |

Mint/burn USDPT, hold and manage USD reserves |

| Ecosystem Partner |

Western Union |

Digital Asset Network, global agent locations, compliance, and distribution |

| Public Chain Layer |

Solana |

Host SPL token contracts and on-chain transfers |

| User Touchpoints |

Exchanges, wallets, Western Union app |

Acquire, hold, transfer, and cash out USDPT |

The on-chain token's credit foundation rests on bank reserves and the federal regulatory framework. Western Union integrates USDPT into its remittance products, agent settlement, and network cash-out systems.

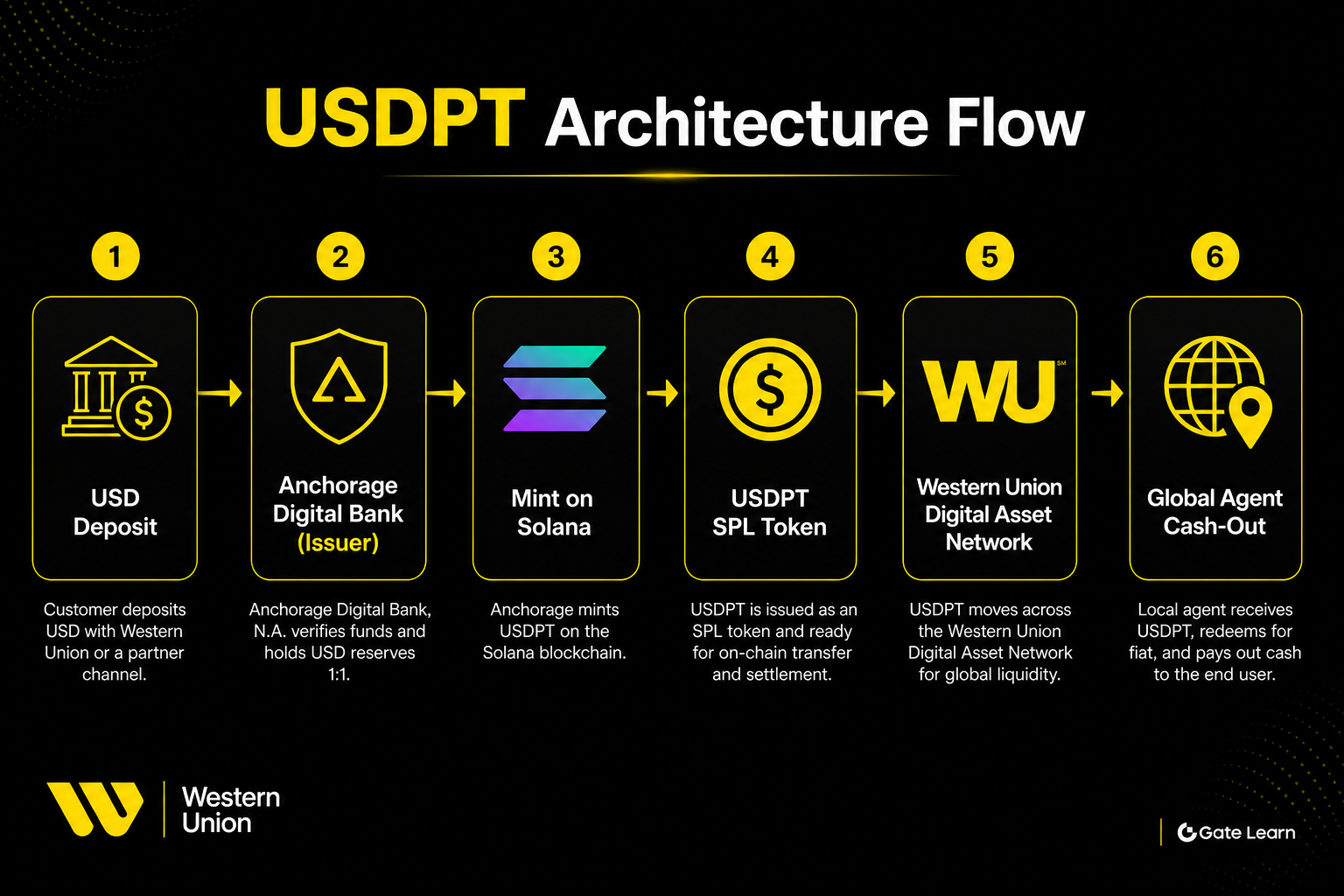

Figure 1. USDPT architecture flow: USD deposits are minted on Solana via Anchorage Digital Bank, then connected to global cash-out channels through the Western Union Digital Asset Network.

Figure 1. USDPT architecture flow: USD deposits are minted on Solana via Anchorage Digital Bank, then connected to global cash-out channels through the Western Union Digital Asset Network.

How Does USDPT Operate on Solana? Contract and On-Chain Standards

USDPT is deployed on the Solana public chain, following the SPL Token standard, and can be transferred between wallets, programs, and exchanges. Solana's high throughput and low latency make it well-suited for the small-value, high-frequency settlement scenarios typical of payment stablecoins.

The Solana contract address for USDPT is HVWf8JmLoHs99Lw8Psf3fyqAtA4crWxCPkrmSdNjhNH3. On-chain operations should verify the contract address and token symbol to avoid confusion with counterfeit tokens. Minting and burning authority is controlled by the issuance program operated by Anchorage Digital Bank. For every new USDPT in circulation, the issuer must hold an equivalent amount of dollar assets in reserve accounts.

Are USDPT Reserve Assets Safe? How to Verify the 1:1 Peg Transparency?

USDPT uses a full-reserve model: for every 1 USDPT issued, Anchorage Digital Bank must hold an equivalent amount of USD reserves. These reserve assets primarily consist of bank demand deposits, U.S. Treasury bills, and similar cash equivalents—highly liquid asset classes with relatively controllable credit risk.

The 1:1 peg reflects a nominal value correspondence, not a government guarantee. USDPT is not FDIC insured nor endorsed by the Treasury or Federal Reserve. Reserve security depends on the bank's asset management, audit disclosures, and regulatory compliance. USDPT reserves and 1:1 peg verifies this across three dimensions: asset classes, mint/burn mechanics, and on-chain supply.

| Verification Dimension |

Observable Information |

Key Points |

| Reserve Composition |

Bank disclosed reports |

Focus on ratios of deposits, Treasury bills, and cash equivalents |

| Supply |

Solana on-chain total supply |

Cross-check with disclosed reserve size |

| Redemption Mechanism |

Anchorage redemption process |

Confirm whether 1:1 USD redemption is supported |

| Regulatory Status |

OCC chartered bank status |

Issuer subject to federal banking regulatory framework |

The table above lists four verification dimensions. On-chain supply is publicly queryable; reserve details depend on issuer disclosures and third-party audits. Evaluation should consider asset quality, redemption liquidity, and disclosure frequency.

What Regulations Govern USDPT? Understanding the Compliance Structure

USDPT's compliance structure centers on federal banking regulation. Anchorage Digital Bank, N.A., as an OCC-chartered national trust bank, must adhere to regulatory requirements including capital adequacy, risk management, anti-money laundering (AML), and customer identification (KYC) for its issuance activities. Western Union bears its own compliance and licensing obligations in the distribution and cash-out phases.

USDPT is not issued, endorsed, or guaranteed by the U.S. government, nor does it qualify for FDIC deposit insurance. "Issued by a regulated bank" and "government guaranteed" are distinct concepts. When Western Union incorporates USDPT into its Digital Asset Network, it leverages global compliance and risk control systems for identity verification and transaction monitoring. Regulatory attitudes vary by country; actual availability depends on each market's licensing.

What Are the Application Scenarios for USDPT? How Will the Western Union Ecosystem Expand?

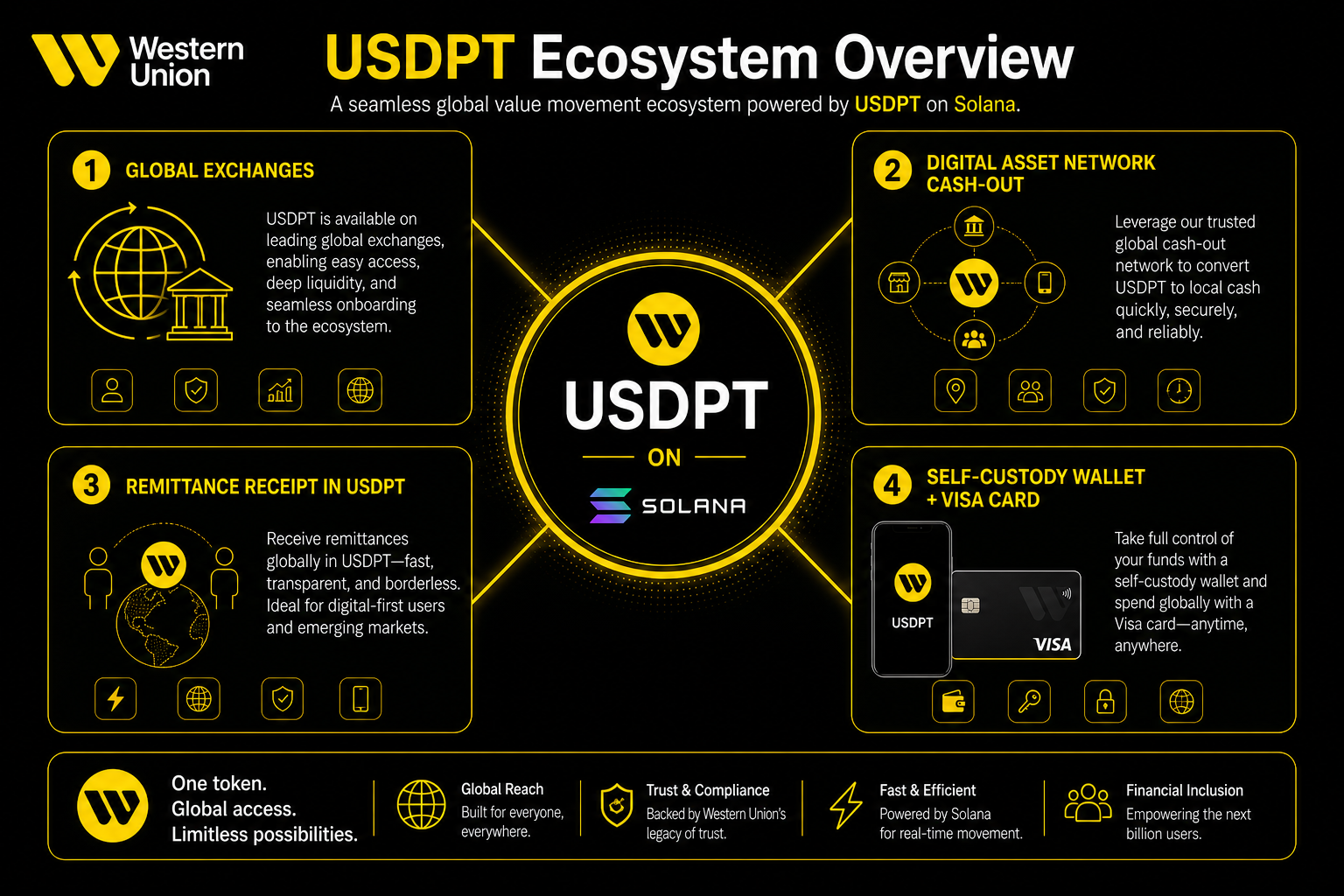

USDPT's planned application scenarios span four main areas: on-chain acquisition, off-chain cash-out, and everyday payments. First, users can purchase and hold USDPT through global virtual asset exchanges to gain on-chain dollar exposure. Second, the Digital Asset Network enables users at partner exchanges in selected markets to cash out USDPT into local fiat currency at Western Union's global agent locations. USDPT mint-to-cashout flow details the repeatable path from exchange acquisition, on-chain holding, to fiat delivery at agent locations.

Third, Western Union's remittance products plan to let recipients in selected markets receive cross-border remittances in USDPT, enabling 24/7 settlement. USDPT vs Western Union traditional remittance compares the structural differences between these two paths in fund flow, intermediate steps, and settlement time. Fourth, a combination of a self-custody wallet and a Visa payment card is planned to allow users in some markets to spend USDPT at Visa-accepting merchants. The specific availability of these scenarios varies by market.

Figure 2. USDPT ecosystem panorama: covers planned scenarios including global exchanges, Digital Asset Network location cash-out, remittance receipt, and self-custody wallet with Visa card.

Figure 2. USDPT ecosystem panorama: covers planned scenarios including global exchanges, Digital Asset Network location cash-out, remittance receipt, and self-custody wallet with Visa card.

The logic behind the Western Union ecosystem expansion is to connect on-chain dollar liquidity with its existing agent network. The Digital Asset Network bridges crypto platforms and offline cash-out capabilities. On-chain settlement offers continuity and programmability, but fiat delivery still depends on country-specific agents and banking partners.

What Are the Advantages and Risks of Using or Holding USDPT?

Advantages: Solana offers high-throughput on-chain transfers; Anchorage Digital Bank provides federally chartered bank-grade issuance and reserve management; Western Union delivers agent locations and compliance networks across more than 200 countries and regions.

Limitations: Availability is constrained by market licensing; not all Western Union locations support USDPT cash-out; on-chain transfers depend on Solana network status; private key loss is irreversible in self-custody scenarios.

Risks: In extreme cases, redemption delays or liquidity pressure may occur; changes in stablecoin policies across countries may affect usability; the Solana contract address must be verified to avoid counterfeit tokens; security incidents at exchanges or wallet platforms could result in asset loss.

When evaluating USDPT, one should distinguish between the token reserve mechanism and the risks inherent in the user's chosen acquisition, storage, and cash-out channels.

Summary and FAQ

U.S. Dollar Payment Token (USDPT) is issued by Anchorage Digital Bank, N.A. on Solana, with Western Union integrating it into the Digital Asset Network and global remittance system. Key points include the division of roles between issuer and ecosystem partner, the SPL on-chain standard, full reserves with 1:1 redemption, the federal banking regulatory framework, and planned scenarios such as exchanges, location cash-out, remittance receipt, and Visa cards. USDPT is not FDIC insured or guaranteed by the U.S. government.

What is USDPT?

U.S. Dollar Payment Token (USDPT) is a dollar-pegged payment stablecoin issued by Anchorage Digital Bank, N.A. on the Solana blockchain, redeemable 1:1 for U.S. dollars and integrated with the Western Union global payment network.

Who issues USDPT? Is Western Union the issuer?

The issuer of USDPT is Anchorage Digital Bank, N.A., an OCC-chartered federal national trust bank. Western Union is the ecosystem partner responsible for Digital Asset Network distribution, compliance, and global cash-out; it does not directly mint on-chain tokens.

What is the Solana contract address for USDPT?

The Solana contract address for USDPT is HVWf8JmLoHs99Lw8Psf3fyqAtA4crWxCPkrmSdNjhNH3. On-chain operations should verify the address and token symbol to avoid confusion with counterfeit tokens.

Is USDPT protected by FDIC deposit insurance?

No. USDPT is not a bank deposit, is not FDIC insured, and is not guaranteed by the U.S. Treasury or Federal Reserve. Its value backing comes from the dollar reserve assets held by Anchorage Digital Bank.

What are the main use cases for USDPT?

Planned scenarios include: purchasing and holding via global virtual asset exchanges; cashing out into local fiat currency at Western Union agent locations through the Digital Asset Network; receiving cross-border remittances in USDPT in selected markets; and spending via a self-custody wallet with a Visa card. Specific availability varies by market.

How does USDPT differ from USDC and USDT?

All three are dollar-pegged stablecoins, but they differ in issuer, regulatory approach, and ecosystem integration. USDPT is issued by OCC-chartered bank Anchorage Digital Bank and is deeply integrated with the Western Union remittance network, focusing on cross-border payments and offline cash-out, rather than general DeFi liquidity. USDC is natively issued by Circle's regulated entities on multiple chains, while USDT is widely circulated across many chains by Tether; both typically have broader coverage in DeFi and exchange scenarios.