WULF stock is categorized within the Bitcoin mining sector, and its performance is typically shaped by both “token price signals” and “cost constraints.” Fluctuations in Bitcoin price directly impact unit hashrate revenue, but stock valuations also account for post-halving output changes, network-wide hashrate competition, and the quality of electricity contracts. By viewing TeraWulf (WULF) stock as a business system that converts electricity into hashrate and hashrate into cash flow, investors can better trace the causal chain behind stock price movements.

Why Is WULF Stock So Closely Tied to the Bitcoin Cycle?

Bitcoin mining companies’ revenues are inherently linked to the block reward mechanism, making their cyclical correlation stronger than that of most traditional industries. The value of WULF stock fundamentally represents the discounted value of future sustainable mining cash flows, which are primarily dictated by Bitcoin price and network output rules.

In the context of stock valuation, BTC price is not the only variable. The market also evaluates “how much BTC can be mined per unit of hashrate,” “the electricity and operating costs per BTC,” and “whether the company can expand or maintain production during downturns.” When these three variables align, stock price elasticity is typically greater; when they diverge, the stock price may decouple from the token price.

This cyclical linkage is also reflected in financing. Mining companies often rely on capital markets to fund equipment upgrades and site expansion, so Bitcoin market conditions indirectly affect financing costs and equity dilution risk. The connection between WULF stock and the Bitcoin cycle is both a matter of operating cash flow transmission and balance sheet repricing.

How Does BTC Price Influence Mining Company Profits and Valuations?

BTC price movements first affect the unit output value of mining companies. If all else remains equal, a higher token price raises revenue expectations for mining machines and improves gross margins; a lower price squeezes margins, making companies more dependent on energy efficiency and cost controls.

The next transmission occurs through cash flow and the balance sheet. Improved profits enhance a company’s ability to self-fund; when profits are under pressure, companies may resort to refinancing, slowing expansion, or reallocating assets to keep operating, prompting the market to reassess risk premiums.

A third layer appears in valuation multiples. Mining stocks are often priced based on both “upside elasticity” and “downside survivability,” so different companies can have different valuation medians even at the same token price. That’s why both WULF’s business model and cost structure must be considered: revenue elasticity and the unit cost base determine how much profit ultimately remains from token price changes.

Why Does Halving Change WULF Stock’s Profitability Threshold?

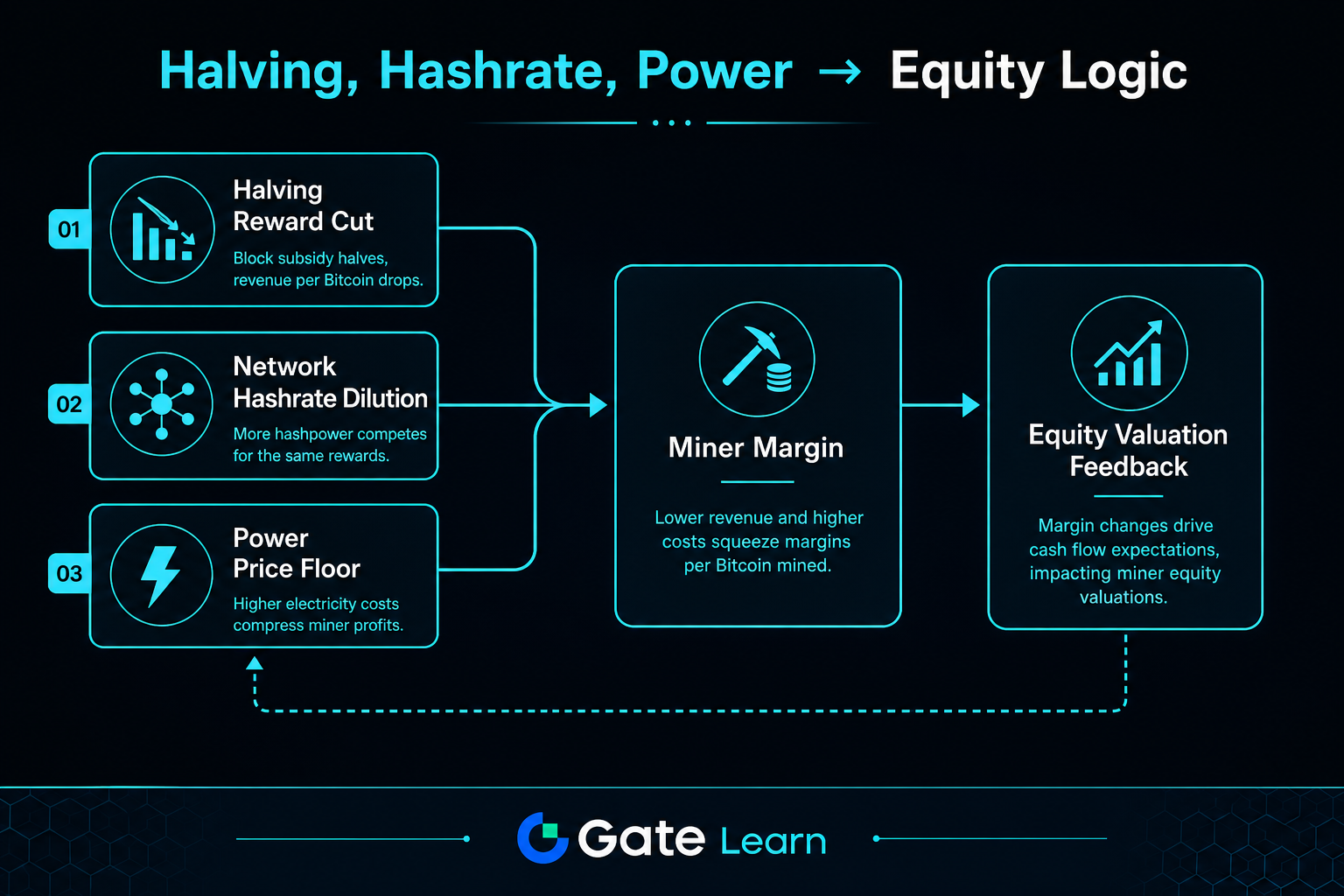

Bitcoin halving directly reduces block rewards per unit time, compressing output under the same hashrate. This protocol-driven constraint raises the breakeven point across the industry.

For WULF stock, the key is whether efficiency gains can offset the drop in unit revenue. Companies typically respond by upgrading mining machines, optimizing energy use, and adjusting electricity procurement; if efficiency gains lag behind output cuts, profit margins will be squeezed, making the stock more vulnerable to risk discounts.

Halving also intensifies competitive sorting. Companies with lower electricity costs and higher equipment efficiency are more likely to sustain positive cash flow, while those with weaker cost structures are more prone to contraction. The market typically reprices mining stocks accordingly.

How Does Rising Network Hashrate Impact WULF’s Unit Output?

An increase in total network hashrate means greater competition, so a single company’s share may decrease. Even if a company’s own hashrate remains stable, its share of block rewards per unit time can be diluted, directly reducing unit hashrate revenue.

This explains why rising BTC prices don’t always translate into higher mining profits. If higher prices attract more hashrate, difficulty adjustments can offset some of the gains, so profit elasticity is often lower than expected.

When analyzing WULF stock, hashrate should be viewed as a dynamic competitive factor, not just a static metric. A more effective approach is to examine whether hashrate growth, difficulty changes, and cost improvements are aligned.

How Does Electricity Price Set the Cost Floor for WULF Stock?

Electricity is one of the most critical variable costs for Bitcoin miners and determines their ability to survive downturns. With the same token price and hashrate, companies with more stable electricity contracts and lower unit power consumption are more likely to maintain resilient cash flows.

Cost analysis for stocks like WULF should consider not just nominal electricity prices but also load management, peak-valley price differentials, and site utilization rates. Higher electricity prices raise unit mining costs, while optimized electricity structures can buffer against token price volatility.

| Transmission Link |

Main Variables |

Typical Profit Impact |

Common Valuation Feedback |

| Revenue Side |

BTC Price, Post-Halving Rewards |

Sets the upper limit on unit hashrate value |

Affects growth expectations and risk appetite |

| Competition Side |

Network Hashrate, Difficulty Adjustment |

Dilutes single-company output share |

Affects sustainability of profits |

| Cost Side |

Electricity Contracts, Energy Efficiency |

Sets the floor for unit cash costs |

Affects survival premium in downturns |

| Financial Side |

Financing Costs, Debt Structure |

Amplifies or buffers profit swings |

Affects discount rates and multiples |

This table underscores that mining stock prices are shaped by multiple interacting variables, not just one factor. Placing all four components in a unified framework reduces the bias of interpreting stocks solely through token price movements.

Figure 1. How halving, hashrate dilution, and electricity costs flow into mining company profits and feed back into stock valuation logic.

How Can Halving, Hashrate, and Electricity Price Be Unified into a Stock Price Logic Chain?

In practice, observe four steps: “revenue elasticity, cost threshold, cash flow cushion, valuation feedback.” First, see if BTC price and post-halving unit output create net revenue gains; second, determine if hashrate competition and electricity prices erode those gains; third, check if the company’s cash flow covers both operating and capital expenses; fourth, see if the market assigns a higher or lower valuation multiple.

This chain also clarifies the key differences in WULF vs. MARA vs. RIOT. Different miners prioritize electricity sourcing, expansion, and capital structure differently, so stock performance within the same Bitcoin cycle can diverge. The key is not price prediction, but verifying if token price gains translate into profits, profits into cash flow, and cash flow into valuation upgrades.

What Are the Advantages, Risks, and Limitations of Using a Cyclical Framework to Analyze WULF Stock?

The advantage is that key variables are traceable: Bitcoin price, network difficulty, unit power consumption, and electricity contract structure can all be monitored. The cyclical framework puts network rules and corporate cost curves in the same context, reducing the bias of narrative-driven analysis.

Risks arise mainly from variable resonance. If falling token prices coincide with rising difficulty and electricity costs, profit shocks are sharper than in single-factor scenarios; tighter financing amplifies pressure to maintain production. The framework can only explain mechanisms, not guarantee the sequence of outcomes or serve as a buy/sell recommendation.

Summary

The relationship between WULF stock and the Bitcoin cycle can be summarized as a transmission chain: BTC price and halving affect unit output value; network-wide hashrate reallocates output share; electricity price and energy efficiency set the cost floor; and cash flow and financing conditions ultimately map to valuation and stock price. This framework explains both “why elasticity differs even during synchronized moves” and “why stock prices may diverge even when token prices rise.” Understanding stocks through this mechanism-based lens better reflects mining company operations than relying on single-point metrics.

FAQ

Why Can’t WULF Stock Be Judged Solely by Bitcoin Price?

While WULF stock is heavily influenced by Bitcoin price, profits also depend on post-halving output, network-wide hashrate competition, and electricity costs. If rising token prices are offset by higher difficulty and costs, profit gains narrow. Stock valuation requires a multi-factor approach.

Will Mining Company Profits Necessarily Fall After Bitcoin Halving?

Halving reduces block rewards per unit time, compressing revenue. Whether profits fall depends on whether companies can offset the impact through energy efficiency upgrades, electricity price optimization, and operational management. Different cost structures mean different outcomes.

What Does Rising Network Hashrate Mean for WULF Stock?

Rising network-wide hashrate typically increases mining difficulty and dilutes a single company’s output share. Even if a company’s hashrate is unchanged, unit hashrate revenue may be pressured, prompting the market to reassess profit sustainability.

Why Do Electricity Price Changes Amplify Mining Stock Volatility?

Electricity is the core variable cost for miners. Rising electricity prices increase unit costs and compress profits. If electricity contracts are unstable, cash flow volatility becomes more pronounced, and valuations reflect higher risk discounts.

How Can WULF Stock’s Valuation Logic Be Understood as a Single Chain?

It can be viewed as “BTC price and halving affect revenue, hashrate affects share, electricity price affects costs, and cash flow affects valuation.” When all four links are aligned, stock price direction is more consistent; if any link is broken, stock performance may diverge from token price.

What Are the Main Risks in the Correlation Between WULF Stock and the Bitcoin Cycle?

The main risks are simultaneous declines in token price, increased difficulty, and higher electricity costs, which pressure both profits and cash flow and raise reliance on refinancing. The cyclical framework highlights risk sources but cannot eliminate operational uncertainty or predict stock price paths.