In the perpetual contract system, the funding rate is one of the most easily misinterpreted variables. Many trading discussions treat it as a “bullish/bearish button”: high rates mean you should short, low rates mean you should long. While this conclusion may occasionally work in certain stages, it lacks consistency. A more accurate understanding is: the funding rate is the correction cost when the perpetual price deviates from the index, a periodic cash flow mechanism designed to keep contract prices anchored around the index over time. It indicates market structural temperature and willingness to pay for leverage, not a guarantee of future direction.

1. Why Funding Rates Exist: Perpetuals Have No Expiry, So They Need a “Continuous Calibrator”

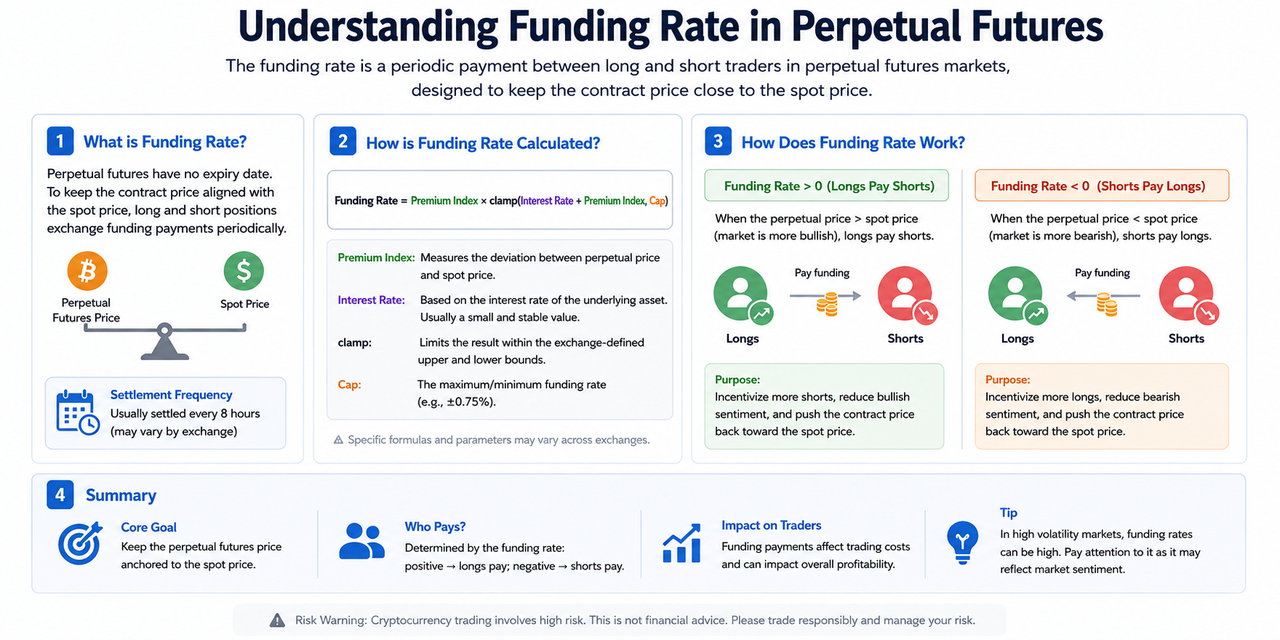

Delivery contracts naturally converge to spot at expiration, but perpetuals lack this mechanism. Without additional constraints, contract prices may drift long-term, deviating from the index and accumulating systemic risk. The function of the funding rate is to turn this deviation into a holding cost:

- When the perpetual price stays above the index for an extended period, longs usually bear positive costs.

- When the perpetual price stays below the index for an extended period, shorts usually bear negative costs.

Essentially, the system attaches a price tag to the “deviation state.” The more obvious and persistent the deviation, the stronger the cost signal tends to be. Thus, funding rate is first a structural variable, and only then a trading variable.

2. High Rates Don’t Mean Immediate Drop: Misjudgments Stem from “Crowding Persistence”

Extreme funding rates are often seen as reversal signals, but market practice shows crowding can persist for a long time, especially when trends are strong, spot supply is tight, and external capital continues to flow in. Even with high rates, prices may keep moving in their original direction.

Common sources of misjudgment include:

- Treating Static Readings as Dynamic Conclusions

A single-point funding rate only describes costs at a specific moment; it doesn’t indicate whether crowding is expanding or easing.

- Ignoring Participant Structure

If dominant forces are institutional funds with higher tolerance, crowding exits tend to be slower than retail leverage unwinding.

- Ignoring Spot-Derivatives Linkage

When spot buying is strong enough, high funding on derivatives may just be a “trend tax,” not a trend endpoint.

Therefore, the correct use of funding signals isn’t to directly take counter trades, but to assess whether systemic fragility is increasing and whether risk budgets need tightening.

3. Three Layers of Funding Rate Meaning: Deviation, Cost, Constraint

To upgrade funding from an “emotional label” to a “structural tool,” break it down into three layers:

- Layer 1: Deviation Meaning

Funding direction usually reflects the main deviation direction between perpetuals and the index—a visible result of basis status.

Funding determines periodic cash flows for leveraged positions. Medium-term positions facing adverse rates over time see their profit thresholds significantly raised.

- Layer 3: Constraint Meaning

The more extreme the funding rate, the greater the system’s correction pressure. If combined with high OI and shallow order books, price becomes more sensitive to shocks.

Together, these three layers determine one thing: funding’s value lies not in “guessing the next candle,” but in “identifying if the system is overheating.”

4. Joint Observation Framework: Funding Must Be Viewed Alongside Basis and OI

Looking at funding alone easily distorts interpretation; a “three-part joint observation” is recommended:

- Basis (Perp-Index)

Observe deviation direction and magnitude—this is the starting point for judging if funding readings are reasonable.

- Funding Strength and Persistence

Assess absolute value, duration, and acceleration to determine if correction pressure is building.

- OI and Trade Structure

Check if open interest is expanding or contracting; combine with volume to judge if crowding is new or existing positions rotating.

Typical combinations (mechanism layer meaning):

- High positive basis + high positive funding + sustained OI expansion

Long crowding heats up, systemic fragility rises, risk management priority increases.

- High positive basis + high positive funding + OI declines

Crowding begins to clear; observe if this is healthy cooling or a precursor to trend reversal.

- Basis converges + funding cools + OI stable

Structure becomes balanced; trend trading and arbitrage opportunities are redistributed.

5. Funding Rate Impacts Different Strategies Differently

Sensitivity to funding varies widely by strategy:

- Ultra-short-term strategies: fee is mostly frictional cost; direction still driven by micro-liquidity and trigger conditions.

- Trend-following strategies: must assess whether “trend returns cover ongoing funding expenses.”

- Medium-term leveraged positions: funding may become the core variable deciding position lifespan.

- Spot-futures/hedging strategies: focus more on whether funding provides stable risk compensation and if channel/execution costs are controllable.

The same funding reading yields different conclusions for different strategies. Later chapters on basis and crowding will further explain matching strategy choices to structural states.

6. Two Common Pitfalls in Trading Execution

Pitfall 1: Translating “Extreme Funding” Directly Into “Inevitable Reversal”

Extreme means fragile—not instant reversal. True reversals are usually triggered by liquidity returning, spot supply-demand shifts, policy/events shocks, or critical price levels causing cascading stops.

Pitfall 2: Only Watching Funding Rate Without Looking at Total Cost Ledger

Actual costs also include fees, slippage, fund transfers, liquidation probability, and opportunity cost. Decisions based solely on funding often result in “direction guessed right but net value doesn’t rise.”

7. From Signal to Action: Funding’s Proper Use Is Risk Management

Actionable takeaways can be summarized in three points:

- During rate heating phases: prioritize lowering leverage density; avoid chasing crowded positions on the same side.

- During high-rate stagnation phases: focus on monitoring OI and order book depth; guard against sudden fragility shifts.

- During rate cooling phases: combine basis convergence and trade structure to judge if it’s trend continuation or structural reversal.

This process emphasizes “identify system temperature first, then decide position strength,” avoiding use of funding as a single-direction signal.

Summary

The core conclusions of this lesson are fourfold:

- Funding rate is a continuous calibrator compensating for perpetuals’ lack of expiry convergence mechanism; its essence is pricing deviation correction cost.

- Extreme rates indicate leverage crowding and rising systemic fragility—not automatic reversal signals.

- Funding must be interpreted jointly with basis, OI, and trade structure; single-indicator conclusions lack stability.

- Funding’s practical value lies mainly in risk budgeting and position management—not as a substitute for directional judgment.

Next lesson will move into the “basis decomposition” module—continuing to break down sources of deviation into supply-demand, liquidity, and arbitrage channels—to build a more complete microstructural decision chain.