TL;DR

- The FOMC maintained the policy rate at 3.50%–3.75%, with one dissenting vote in favor of a rate cut, signaling early internal divergence. Jerome Powell highlighted elevated geopolitical uncertainty in the Middle East, noting the Fed remains data-dependent and open to policy adjustments.

- Industrial production slowed to 0.2%, indicating moderating economic momentum, while the Philadelphia Fed Manufacturing Index reached a six-month high, suggesting selective resilience. However, rising energy costs pose downside risks to margins and the forward outlook.

- Crypto markets remained under pressure, with BTC down 6.8% and ETH down 5.8%, while the Fear & Greed Index fell to 8, entering extreme fear territory, typically associated with late-stage drawdowns or potential capitulation.

- Resolv Labs infrastructure breach, where an attacker used a compromised private key to mint around $80 million of unbacked USR stablecoins. USR briefly depegged to as low as $0.025 before partially recovering.

- Morgan Stanley filed an amended S-1 for a spot Bitcoin ETF, reflecting continued expansion of Wall Street distribution channels into digital assets.

- Grayscale Investments submitted an S-1 for a Hyperliquid ETF, signaling growing competition for HYPE-linked financial products.

- Kalshi raised over $1 billion at a $22 billion valuation, underscoring the rapid institutionalization of prediction markets as an emerging financial vertical.

Macro Overview

Federal Reserve Holds Rates Steady, Industrial Production Slows to 0.2% in February

The FOMC decided to maintain the Fed rate at 3.50–3.75%, with Chair Powell emphasizing a data-dependent approach and mentioning that inflation is showing signs of improvement. The Fed also highlighted uncertainty around how the Middle East situation could affect the U.S. economy. One member, Stephen Miran, dissented and supported a 25 bps rate cut, citing growing concerns about weakness in the labor market. This split suggests there is increasing debate within the Fed about the strength of the economy. Markets are starting to expect possible rate cuts later in 2026 if economic data continues to soften and geopolitical tensions ease. The Fed has signaled that it is prepared to adjust policy if risks become more pronounced.

U.S. industrial production rose 0.2% in February 2026, slowing from a 0.7% increase in January. Manufacturing output also grew 0.2%, while total industrial output was up 1.4% compared to a year ago. Meanwhile, the Philadelphia Fed Manufacturing Index climbed to 18.1 in March from 16.3 in February, reaching its highest level in six months. This points to stronger sentiment in the manufacturing sector despite the softer monthly production data.

The data suggest that growth is cooling from earlier strength but not weakening sharply. The combination of steady year-on-year growth and improving sentiment supports the Fed’s more patient approach, as the manufacturing sector appears able to handle current economic conditions without an immediate rate cut.

The S&P 500 fell 1.9% for the week, while the Nasdaq Composite dropped 2.1% and the Dow also declined 2.1%. The S&P 500 also fell below its 200-day moving average for the first time since June. Oil prices spiked during the week, with Brent crude briefly reaching $119 per barrel before pulling back, and overall prices moving above $100. The market selloff marked a sharp reversal from earlier optimism after the Fed’s decision to hold rates.

Rising tensions in the Middle East pushed energy prices higher, raising concerns about inflation and outweighing the positive signals from recent CPI data. The break below the 200-day moving average also points to weakening market sentiment and growing concerns about economic growth amid rising energy costs.

In the coming week, we will see the release of Core PCE and PMI, with energy prices being the main variable. If the Strait of Hormuz remains closed, higher oil prices could push inflation up and make it harder for the Fed to move toward rate cuts. PMI data will also be important. Manufacturing sentiment has held up so far, but rising energy costs could start to squeeze margins. (1)

DXY

DXY

DXY fell 0.92% to 99.503 as the Fed kept rates unchanged and highlighted uncertainty around the Middle East, lowering expectations for further rate hikes. At the same time, oil prices surged to $119, raising stagflation concerns and weighing on the dollar despite typical safe-haven demand. Markets also began pricing in earlier rate cuts in 2026. (2)

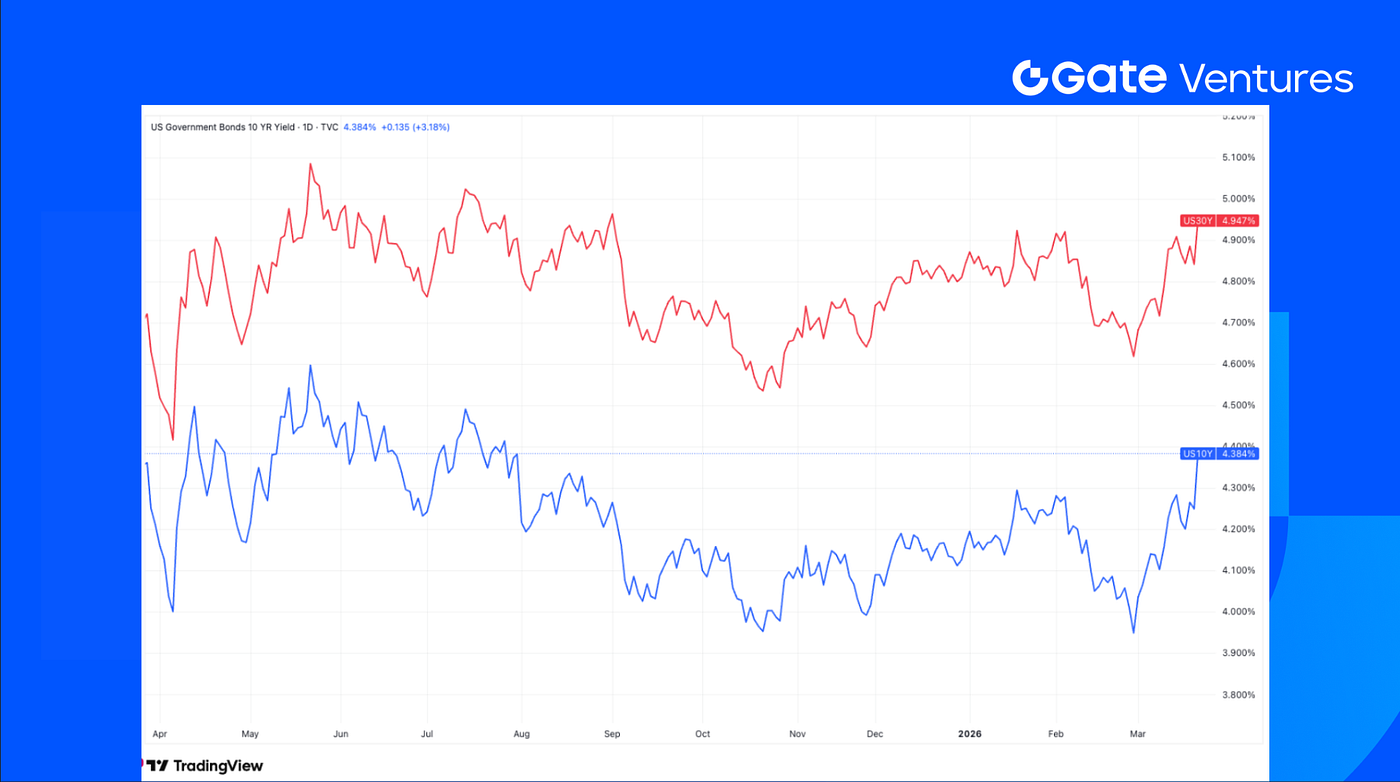

US 10-Year and 30-Year Bond Yields

US 10-Year and 30-Year Bond Yields

Driven by soaring energy prices and Middle East tensions, U.S. Treasury yields have risen significantly. The 10-year yield rose to 4.411%, reflecting heightened inflation concerns. Investors are now recalibrating expectations for Federal Reserve policy, as persistent cost pressures challenge the previous narrative of imminent interest rate cuts. (3)

Gold

Gold

Gold dropped 10.25% to $4,491 per ounce, marking its worst week in 43 years. Despite geopolitical tensions, safe-haven demand weakened as the Fed held rates and markets scaled back expectations for near term cuts. USD weakness offered little support. (4)

Crypto Markets Overview

1. Main Assets

BTC Price

BTC Price

ETH Price

ETH Price

ETH/BTC Ratio

ETH/BTC Ratio

BTC fell 6.8% last week, while ETH declined 5.8%. Despite the broader pullback, the ETH/BTC ratio rose 1.2% to 0.03, indicating relative outperformance from ETH. On the flows side, spot BTC ETFs recorded net inflows of $767.33 million, while spot ETH ETFs saw net inflows of $160.8 million. (5)

Meanwhile, market sentiment deteriorated further, with the Fear & Greed Index dropping to 8 from 23 the previous week, keeping the market firmly in extreme fear territory. (6)

2. Total Market Cap

Crypto Total Marketcap

Crypto Total Marketcap

Crypto Total Marketcap Excluding BTC and ETH

Crypto Total Marketcap Excluding BTC and ETH

Crypto Total Marketcap Excluding Top 10 Dominance

Crypto Total Marketcap Excluding Top 10 Dominance

Total crypto market capitalization declined 5.5% last week. Excluding BTC and ETH, the market was down 2.9%, while the broader altcoin market, measured excluding the top 10 tokens by dominance, fell 4.4%.

A notable incident last week was the infrastructure breach confirmed by Resolv Labs, in which an attacker used a compromised private key to mint approximately $80 million of unbacked USR stablecoins. Reported realized losses remain limited at around $500K, with roughly $141 million in remaining assets still intact and no collateral reportedly drained. Following the incident, USR briefly depegged and fell as low as $0.025 before partially recovering. (7)

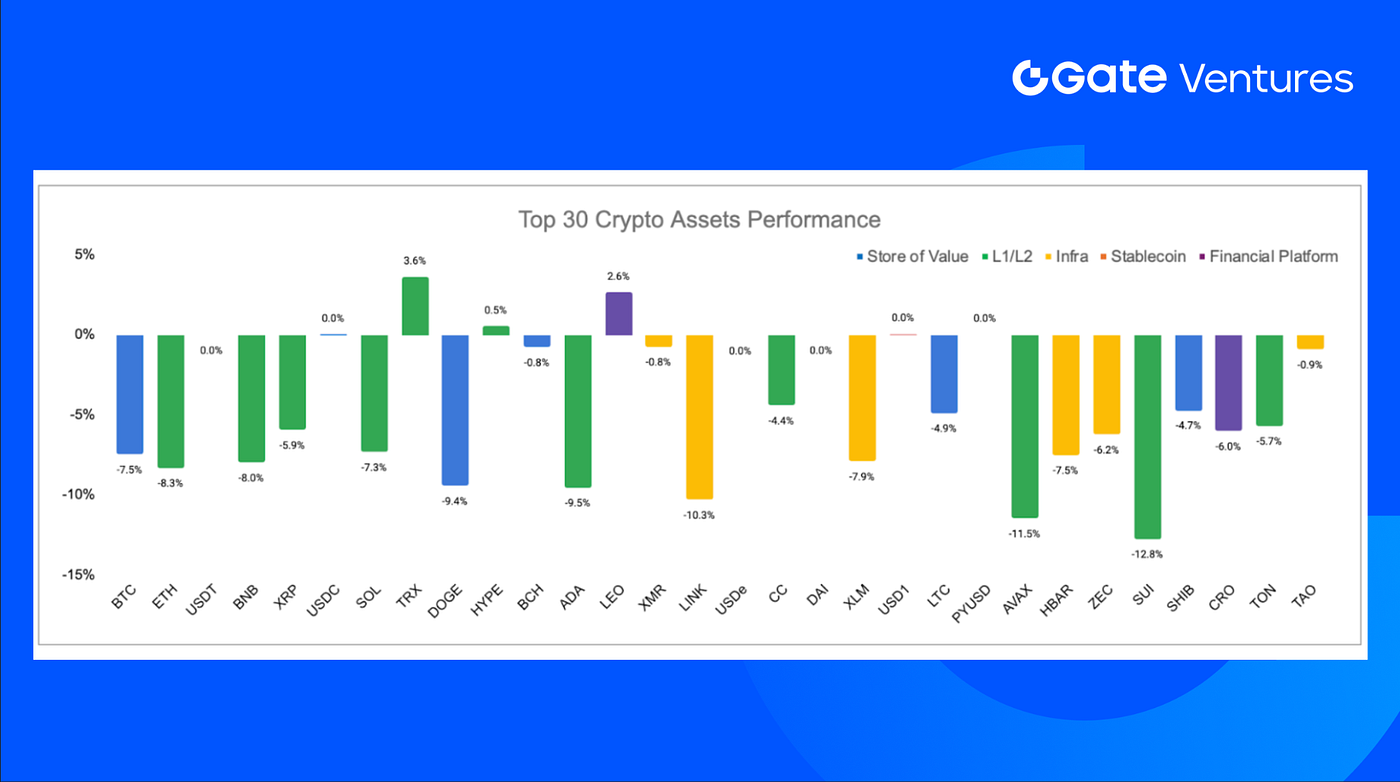

Source: Coinmarketcap and Gate Ventures, as of 23th Mar 2026

Source: Coinmarketcap and Gate Ventures, as of 23th Mar 2026

Among the top 30 assets, prices declined ~4.5% on average, only TRX, LEO, and HYPE posted price gain.

4. New Token Launched

Katana (KAT) is the native token of Katana Network, a DeFi-focused chain designed to concentrate liquidity and align users with the economic activity of core applications such as Morpho and Sushi. The token captures ecosystem utility through fee participation and incentive direction, and could eventually play a broader role in network security and chain-level value accrual. (8)

KAT began trading at around $0.013, peaked at roughly $0.018 shortly after launch, and is currently hovering around $0.011–$0.012, implying an approximate fully diluted valuation of $120 million. KAT was listed on major exchanges including Binance, OKX, Coinbase,etc

The Key Crypto Highlights

1. Morgan Stanley files amended S-1 for spot Bitcoin ETF as Wall Street distribution expands

Morgan Stanley has filed a second amended S-1 for its proposed spot Bitcoin ETF, the Morgan Stanley Bitcoin Trust (MSBT), bringing the product closer to a potential NYSE Arca listing pending regulatory approval. The filing outlines a $1 million seed raise through 50,000 initial shares, with proceeds to be used to purchase Bitcoin for the fund, and names Jane Street, Virtu Americas and Macquarie Capital as authorized participants to support creation and redemption activity and keep the ETF trading close to NAV. The move is notable because Morgan Stanley is shifting from mainly distributing third-party Bitcoin ETFs to launching its own product, which would let it capture management-fee economics directly while leveraging its large adviser network for distribution. (9)

2. Grayscale files S-1 for Hyperliquid ETF as competition for HYPE-based products builds

Grayscale has filed an S-1 with the SEC for a spot Hyperliquid ETF, joining Bitwise and 21Shares in seeking to launch an exchange-traded product tied to the HYPE token. The proposed fund, Grayscale HYPE ETF, would trade under the ticker GHYP on Nasdaq if approved and would use Coinbase as custodian, though Grayscale has not yet disclosed the management fee. Unlike Bitwise’s amended filing, Grayscale’s current proposal does not include staking, but it said staking could be added later if conditions allow, which would open the door for yield generation on top of token price exposure. (10)

3. NYSE exchanges remove crypto ETF options cap as institutional trading flexibility expands

NYSE Arca and NYSE American have removed the 25,000-contract position and exercise limits on options tied to 11 Bitcoin and Ether ETFs, with the SEC allowing the rule changes to take effect immediately rather than waiting the standard 30 days. The amendments also permit these products to trade as FLEX options, which gives institutions more customizable terms such as non-standard strike prices, expirations and exercise styles. The affected funds include major spot crypto ETFs such as BlackRock’s IBIT, Fidelity’s FBTC and ETH fund, ARK 21Shares’ ARKB, Grayscale’s Bitcoin and Ethereum trust products, and Bitwise’s Bitcoin and Ethereum ETFs. (11)

Key Ventures Deals

1. Bluesky discloses $100M Series B as open social infrastructure scales beyond the core app

Bluesky has disclosed a $100 million Series B led by Bain Capital Crypto, including participation from Alumni Ventures, True Ventures, Anthos Capital, Bloomberg Beta and Knight Foundation, and the capital has been used to expand the team and continue developing both the Bluesky app and the underlying AT Protocol. The announcement matters because Bluesky is increasingly positioning itself not just as an alternative social app, but as the leading open social infrastructure layer, with user growth rising from 13 million to more than 43 million globally, an ecosystem now holding around 20 billion public records, over 400,000 monthly SDK downloads and more than 1,000 ATProto-based apps used each week. (12)

2. Kalshi raises over $1B at a $22B valuation as prediction markets move deeper into mainstream finance

Kalshi has reportedly raised more than $1 billion in a new funding round led by Coatue Management at a $22 billion valuation, roughly doubling its valuation from the $11 billion level reported in its December round. The raise matters because it shows that investors are still aggressively backing prediction-market infrastructure despite mounting political and legal scrutiny, betting that Kalshi’s federally regulated exchange model can become a major financial venue rather than just a niche retail speculation platform. Kalshi has expanded rapidly on the back of sports and event contracts, drawn major trading firms and data-distribution partners into its ecosystem, and sits at the center of a wider institutionalization trend in prediction markets even as state-level legal battles and manipulation concerns remain a meaningful overhang. (13)

3. RoboForce raises $52M to scale industrial “robo-labor” as physical AI moves toward real-world deployment

RoboForce has raised $52 million in an oversubscribed round, bringing total funding to $67 million, with the new capital led by YZi Labs and joined by investors including Jerry Yang alongside existing backers such as Myron Scholes, Gary Rieschel and Carnegie Mellon University. The company is focused on deploying general-purpose physical AI robots for industrial environments where labor is scarce and tasks are repetitive, hazardous or physically demanding, targeting sectors such as solar, data centers, mining, shipping, manufacturing and logistics. The funding is being directed not just toward robot hardware, but toward the full commercialization stack: advancing RoboForce’s robot foundation model, building a data flywheel from real-world fleet and simulation data, scaling manufacturing readiness and converting pilot programs into recurring revenue deployments. (14)

Ventures Market Metrics

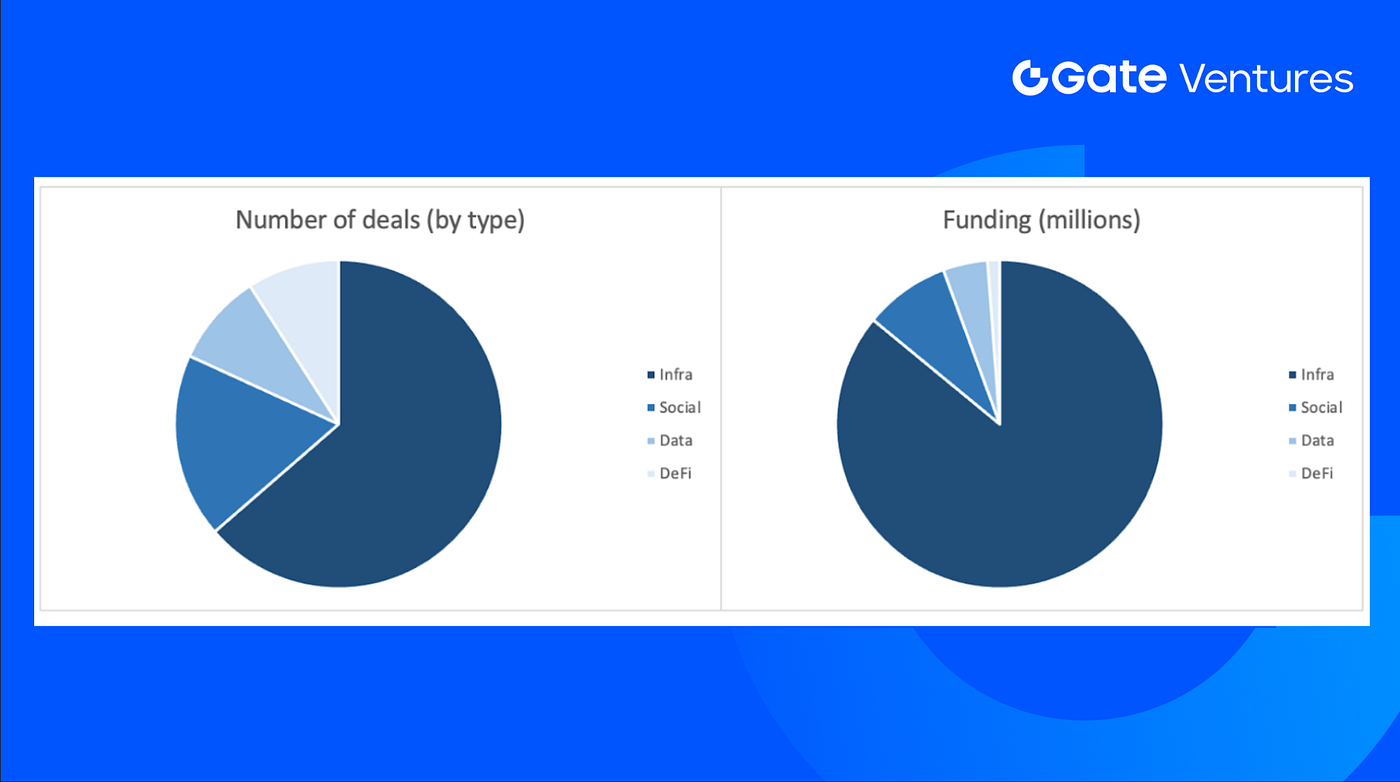

The number of deals closed in the previous week was 11, with Infra having 7 deals, representing 64% of the total number of deals. Meanwhile, Social had 2 deals, Data and DeFi had 1 deal respectively.

Weekly Venture Deal Summary, Source: Cryptorank and Gate Ventures, as of 23th Mar 2026

Weekly Venture Deal Summary, Source: Cryptorank and Gate Ventures, as of 23th Mar 2026

The total amount of disclosed funding raised in the previous week was $1.18B, 4 deals in the previous week didn’t announce the raised amount. The top funding came from the Infra sector with $1.02B. Most funded deals: Kalshi ($1B).

Weekly Venture Deal Summary, Source: Cryptorank and Gate Ventures, as of 23th Mar 2026

Weekly Venture Deal Summary, Source: Cryptorank and Gate Ventures, as of 23th Mar 2026

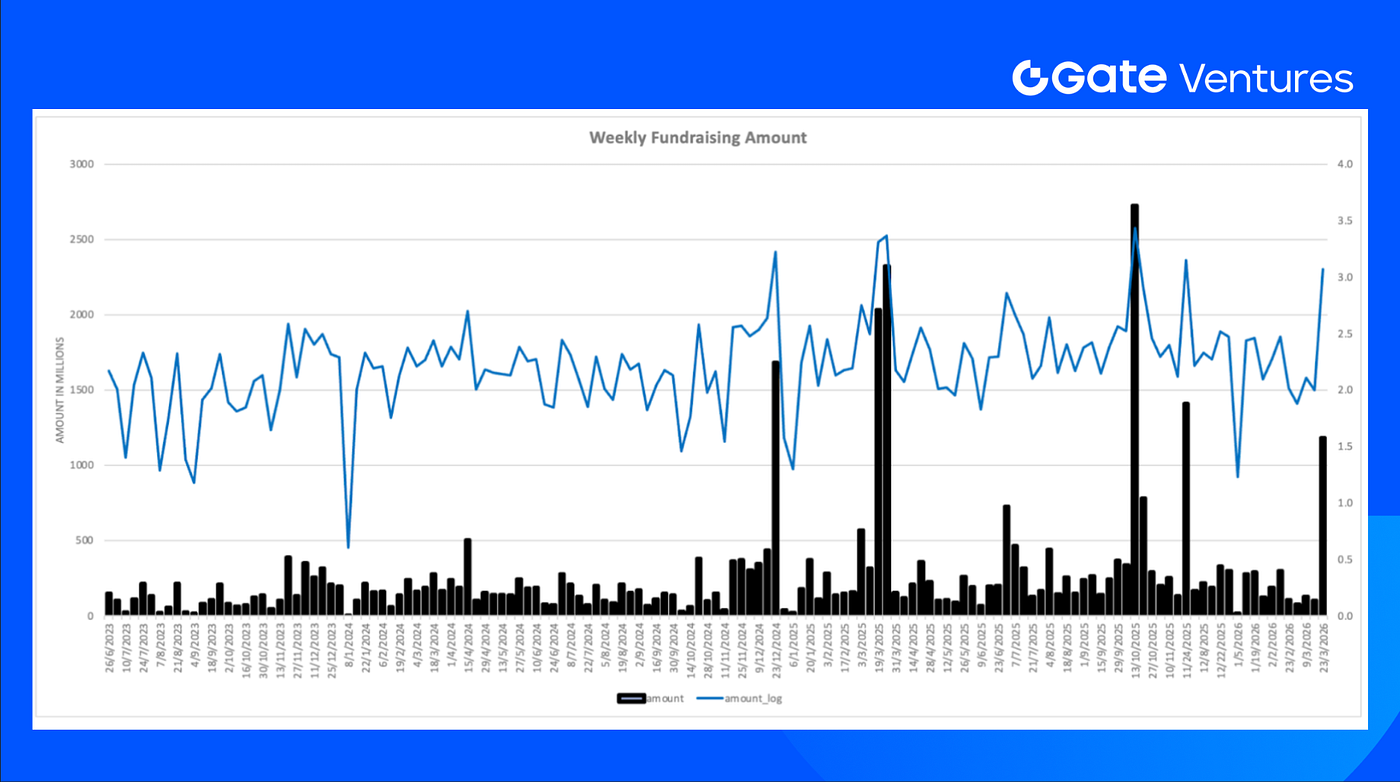

Total weekly fundraising surged to $1.18B for the fourth week of Mar-2026, an increase of 1079% compared to the week prior.

About Gate Ventures

Gate Ventures, the venture capital arm of Gate.com, is focused on investments in decentralized infrastructure, middleware, and applications that will reshape the world in the Web 3.0 age. Working with industry leaders across the globe, Gate Ventures helps promising teams and startups that possess the ideas and capabilities needed to redefine social and financial interactions.

Website | Twitter | Medium | LinkedIn

The content herein does not constitute any offer, solicitation, or recommendation*.* You should always seek independent professional advice before making any investment decisions. Please note that Gate Ventures may restrict or prohibit the use of all or a portion of the services from restricted locations. For more information, please read its applicable user agreement.

Reference

- S&P Week Ahead Economic Preview, https://www.spglobal.com/market-intelligence/en/news-insights/research/2026/03/week-ahead-economic-preview-week-of-23-march-2026

- DXY Index, TradingView, https://www.tradingview.com/chart/z1UD772v/?symbol=TVC%3ADXY

- US 10 Year Bond Yield, TradingView, https://www.tradingview.com/chart/B9cgEklh/?symbol=TVC%3AUS10Y

- Gold Price, TradingView, https://www.tradingview.com/chart/z1UD772v/?symbol=TVC%3AGOLD

- BTC & ETH ETF Inflow, https://sosovalue.com/tc/assets/etf/us-btc-spot

- BTC Greed and Fear Index, https://alternative.me/crypto/fear-and-greed-index/

- Resolv confirms that the platform has been attacked and has suspended all protocol functions, https://www.chaincatcher.com/en/article/2253582

- Katana tokenomics, https://katana.network/blog/the-network-is-katana-the-token-is-kat

- Morgan Stanley files amended S-1 for spot Bitcoin ETF as Wall Street distribution expands, https://cointelegraph.com/news/morgan-stanley-msbt-spot-bitcoin-etf-s1-amendment

- Grayscale files S-1 for Hyperliquid ETF as competition for HYPE-based products builds, https://cointelegraph.com/news/grayscale-files-sec-papers-for-hyperliquid-etf-joining-bitwise-21shares

- NYSE exchanges remove crypto ETF options cap as institutional trading flexibility expands, https://cointelegraph.com/news/nyse-exchanges-scrap-crypto-options-cap

- Bluesky discloses $100M Series B as open social infrastructure scales beyond the core app, https://techcrunch.com/2026/03/19/bluesky-announces-100m-series-b-after-ceo-transition/

- Kalshi raises over $1B at a $22B valuation as prediction markets move deeper into mainstream finance, https://www.bloomberg.com/news/articles/2026-03-19/kalshi-gets-1-billion-in-new-funding-at-22-billion-valuation

- RoboForce raises $52M to scale industrial “robo-labor” as physical AI moves toward real-world deployment, https://www.roboforce.ai/news/roboforce-fundraising-announcement-2026-03