The global cross border payment market has long been dominated by the banking system, and SWIFT has remained a core infrastructure layer within international payment networks. For decades, most international remittances have had to move through bank account systems and correspondent clearing networks, which means cross border payments have essentially functioned as a collaboration network between banks.

However, with the growth of digital payments and the stablecoin market, more companies are beginning to explore blockchain networks for international fund settlement. This shift has also driven the development of on-chain FX infrastructure. Compared with traditional banking networks, which rely on clearing institutions and correspondent banks, on-chain FX places greater emphasis on using stablecoin liquidity and blockchain settlement networks to enable global capital flows. Codex FX is one of the representative projects in this direction.

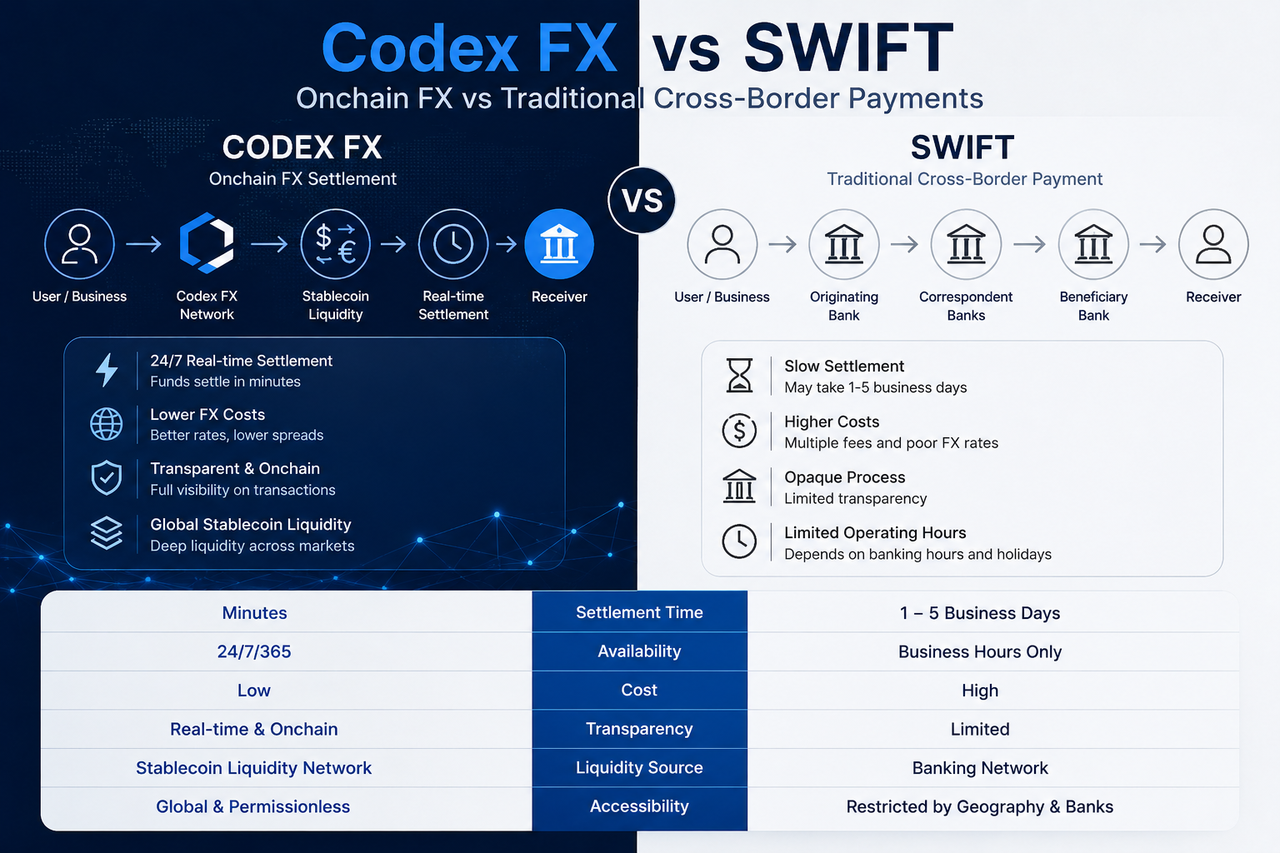

A Brief Look at SWIFT and Codex FX, and How They Differ

SWIFT, or the Society for Worldwide Interbank Financial Telecommunication, is one of the main international payment messaging networks used by banks worldwide. Its core function is to help banks securely exchange payment information so international fund clearing can take place.

In the traditional SWIFT payment system, an international remittance usually passes through multiple banks and correspondent clearing institutions. For example, when a user sends money from one country to another, the funds may need to move layer by layer through a correspondent banking network.

As the on-chain foreign exchange, or on-chain FX, system within the Codex network, Codex FX aims to use stablecoins and an on-chain liquidity network to improve the efficiency of global payments and cross border settlement.

Unlike SWIFT, Codex FX focuses more on using stablecoins to transfer value directly, rather than relying on information synchronization and clearing processes between bank accounts. Its system is built around stablecoin liquidity, real time FX routing, and on-chain settlement, allowing international payments to be completed more quickly.

| Comparison Dimension |

Codex FX |

SWIFT |

| Core structure |

On-Chain stablecoin settlement network |

Bank messaging and clearing network |

| Payment medium |

Stablecoins |

Bank account system |

| Operating hours |

24/7 around the clock |

Mainly business days |

| Intermediaries |

Fewer |

Multiple layers of correspondent banks |

| Settlement speed |

Minutes |

Hours to days |

| FX transparency |

Higher |

Relatively limited |

| Global accessibility |

Stronger |

Limited by regional financial systems |

| Liquidity source |

Stablecoin liquidity network |

Bank clearing system |

What Are the Core Differences Between Codex FX and SWIFT?

Although both Codex FX and SWIFT are involved in international payments, their operating logic is fundamentally different.

SWIFT is essentially a messaging network between banks, while Codex FX is an on-chain stablecoin settlement network. SWIFT depends more on coordination and clearing among financial institutions, while Codex FX focuses on moving funds directly through stablecoins and blockchain networks.

In addition, SWIFT payment speed is usually affected by bank operating hours and correspondent clearing structures, while Codex FX’s on-chain settlement can provide a global payment experience closer to real time.

This also means the two systems differ clearly in payment efficiency, liquidity structure, and user experience.

Why Is on-chain FX Settlement Faster?

Traditional international payments usually pass through several intermediary banks, so funds often take hours or even days to arrive. In some cross border scenarios, delays can become even more obvious because of time zones, holidays, and banking system limitations.

on-chain FX networks can complete settlement directly on-chain through stablecoins. Since blockchain networks can operate around the clock, funds can continue moving between global markets without waiting for bank business hours.

Codex FX places greater emphasis on fast finality and real time liquidity routing, which helps reduce waiting time in traditional payment systems. This structure is especially suitable for scenarios that require efficient capital movement, such as international trade, remittances, and corporate treasury operations.

How Do Codex FX and SWIFT Differ in Liquidity Structure?

SWIFT’s liquidity system is mainly built on bank accounts and correspondent banking networks. Fund movement between different countries and regions usually requires large banks to maintain international clearing capacity.

Codex FX, by contrast, focuses on enabling global payments through stablecoin liquidity pools and on-chain fund routing. This means funds can enter target markets directly through stablecoin networks, without relying on a complex banking intermediary structure.

This difference also gives on-chain FX stronger global accessibility in some emerging markets.

How Do the Risk Structures of on-chain Payments and Traditional Bank Payments Differ?

Although on-chain payments can improve international settlement efficiency, their risk structure is not the same as that of the traditional banking system.

The advantage of the traditional banking system is that its regulatory framework is relatively mature, with more developed compliance and consumer protection mechanisms. Its drawback is lower efficiency and dependence on a complex intermediary structure.

on-chain payment networks place greater emphasis on openness and real time operation, but stablecoin regulation, on-chain liquidity, and fiat on ramp and off ramp systems remain important challenges. For Codex FX, the ability to balance payment efficiency with global compliance will also affect its long term development.

Conclusion

Codex FX and SWIFT represent two different global payment systems. SWIFT is built on traditional banking and correspondent clearing networks, while Codex FX builds a real time payment network based on stablecoins and on-chain liquidity.

As stablecoins gradually enter international trade, corporate treasury operations, and the global payments market, the importance of on-chain FX infrastructure continues to rise. Compared with traditional bank based cross border payment systems, Codex FX places greater emphasis on real time settlement, low friction liquidity, and global stablecoin payment capabilities.

FAQs

What Is the Biggest Difference Between SWIFT and Codex FX?

SWIFT is a payment messaging network between banks, while Codex FX is an on-chain FX network built on stablecoins and on-chain settlement.

Will Codex FX Replace SWIFT?

At present, the two are better understood as payment systems with different structures. Traditional banking networks still occupy the core position in global finance, but stablecoin payments are growing quickly.

Does Codex FX Depend on Banks?

on-chain settlement mainly relies on stablecoin networks, but fiat on ramps and off ramps in the real world still require support from banks and payment channels.

Why Does Codex FX Emphasize Emerging Markets?

Emerging markets often face high cross border payment costs and low settlement efficiency, while stablecoin payments can reduce friction in international capital flows.