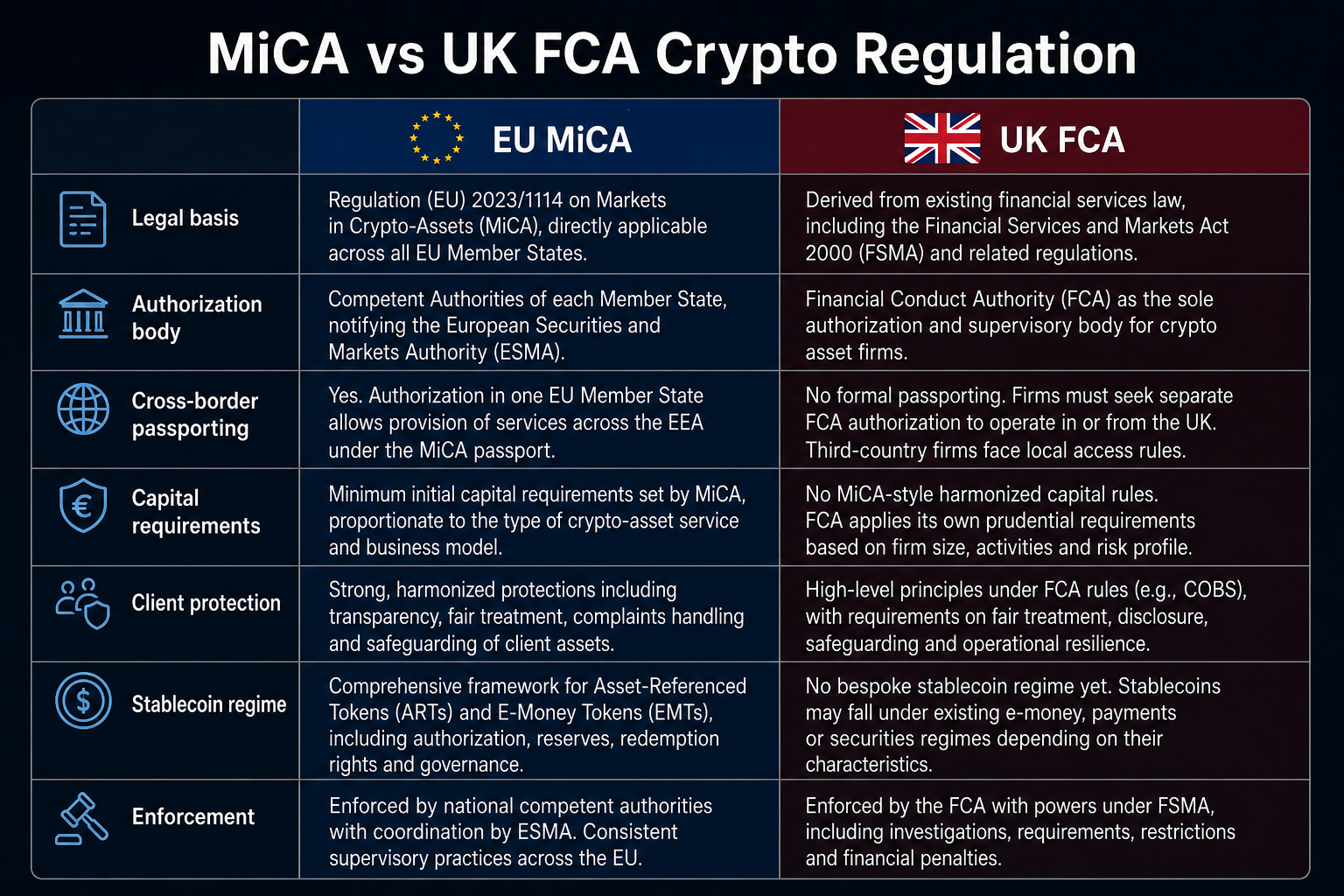

The main distinction between EU MiCA and UK FCA crypto regulation is the legal framework and scope: MiCA provides a unified EU-wide regulatory regime for crypto assets, covering all member states through CASP licensing and the EEA passport mechanism; the UK FCA, following Brexit, operates an independent national regulatory path focused on anti-money laundering registration, financial promotion approval, and subsequent FSMA expansion, without automatic reciprocal recognition.

Crypto platforms serving both EU and UK users must separately identify admission obligations and disclosure standards under each regime. MiCA EU crypto regulation outlines MiCA’s structure from CASP licensing, stablecoin classification, and the EU passport mechanism; this article provides a side-by-side comparison of MiCA and UK FCA regarding authorization procedures, capital requirements, stablecoin rules, and cross-border operations. Unlike the transatlantic comparison in MiCA vs SEC, the EU-UK contrast highlights the shift after Brexit from a “unified regulation” to a “national framework.”

Comparison of MiCA and UK FCA crypto regulatory frameworks in scope, licensing, stablecoin rules, and cross-border arrangements.

What is the MiCA framework?

The Markets in Crypto-Assets Regulation (MiCA) is an EU regulation (Regulation (EU) 2023/1114) standardizing crypto asset issuance and services. MiCA categorizes crypto assets into Asset-Referenced Tokens (ART), Electronic Money Tokens (EMT), and other crypto assets, and defines service providers as Crypto-Asset Service Providers (CASP).

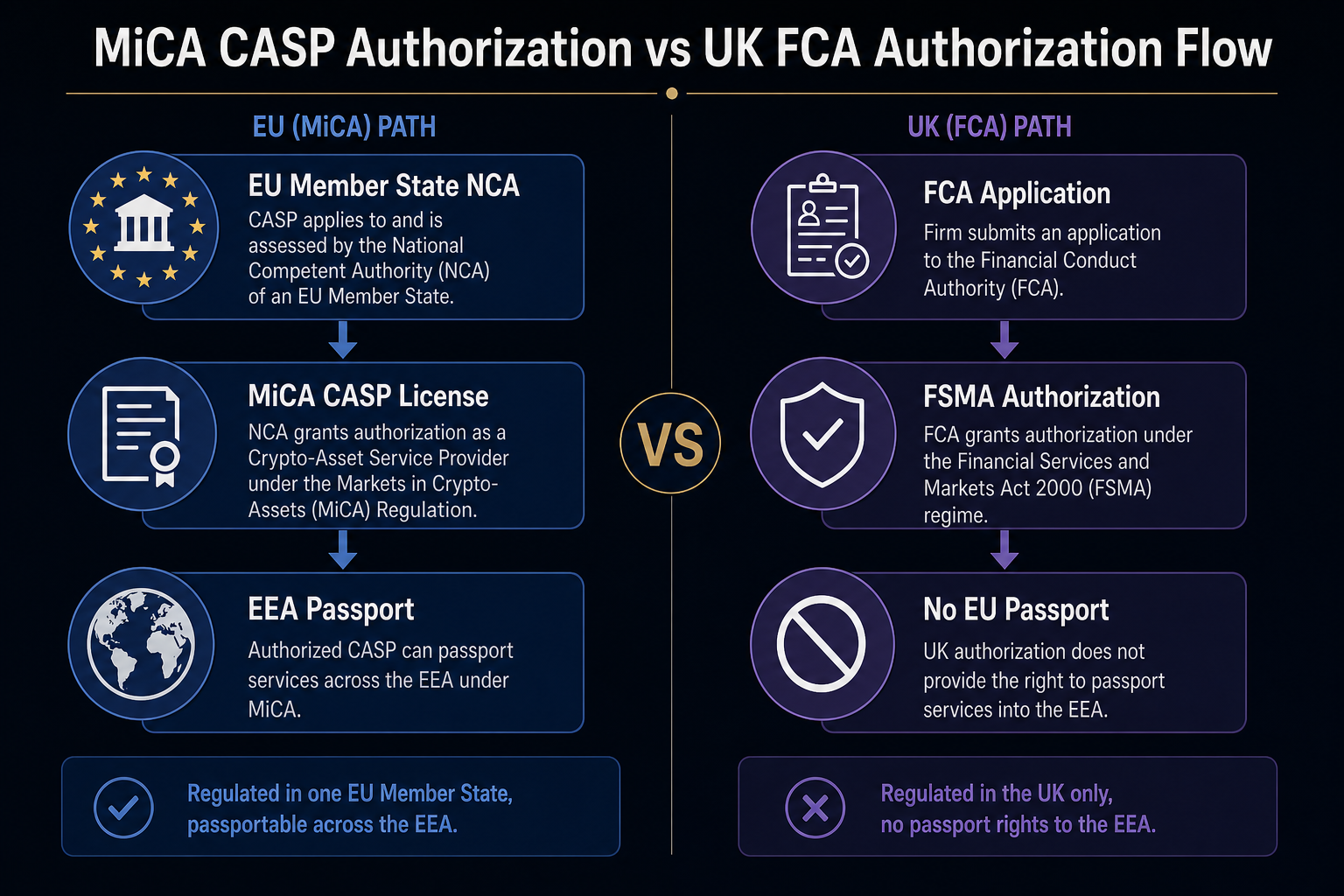

CASPs must apply for authorization from their local National Competent Authority (NCA). Once approved, they can operate across the EEA using the passport mechanism. MiCA also requires issuers to publish a whitepaper before public sale and sets requirements for marketing materials, conflict of interest management, and segregation of client assets.

What is the UK FCA framework?

The UK Financial Conduct Authority (FCA) has developed an independent crypto asset regulatory regime since Brexit, no longer applying MiCA. Key elements include the crypto asset business registration under the Money Laundering Regulations (MLRs) 2017 and financial promotion approval under the Financial Services and Markets Act 2000 (FSMA).

MLRs registration applies to crypto exchanges and custodial wallet providers, focusing on anti-money laundering (AML) and know-your-customer (KYC) compliance. FSMA financial promotion rules require that crypto asset promotions to UK consumers are approved by FCA-authorized persons. The FCA is also expanding formal authorization under FSMA to cover trading, custody, lending, and related activities.

Licensing and authorization process comparison

Under MiCA, CASPs submit authorization applications to NCAs, covering governance, internal controls, IT, asset safeguarding, and prudential resources. After approval, CASP authorization enables EEA-wide operations via passporting. Under FCA rules, firms must first complete MLRs registration; marketing to UK retail users requires financial promotion approval by FCA-authorized persons. The FSMA expansion will bring core activities under formal FCA authorization.

A firm licensed as a MiCA CASP in any EU country cannot legally operate in the UK based solely on that license; FCA-registered firms entering the EEA must separately obtain MiCA authorization.

Parallel illustration of MiCA CASP licensing and FCA MLRs registration and financial promotion approval.

Capital and client protection comparison

MiCA imposes minimum capital requirements for CASPs, typically €50,000–€150,000 or calculated based on expenses, and requires client asset segregation, whitepaper disclosure, and complaint handling. FCA’s current MLRs registration phase has lower prudential capital requirements than MiCA, focusing on AML and operational resilience; FSMA expansion will introduce prudential requirements aligned with business scale. FCA protects clients by restricting inappropriate marketing to retail users and requiring registered firms to follow asset safeguarding guidelines.

These standards are not automatically equivalent. Firms operating in both jurisdictions must separately calculate capital buffers, segregate accounts, and fulfill disclosure obligations; compliance in one country does not guarantee compliance in the other.

Stablecoin regulation comparison

MiCA applies a dual classification to stablecoins: EMTs must be issued by authorized credit or electronic money institutions; ART issuers must meet reserve, redemption, and governance requirements, with large tokens subject to additional EBA oversight. The UK has a separate legislative approach: the Bank of England sets prudential expectations for systemically important stablecoins, while the FCA oversees issuance and trading. UK classification does not directly match MiCA’s EMT/ART model.

The same token may be classified differently in the EEA and UK; issuance and circulation strategies must be tailored to each jurisdiction.

Cross-border operations and mutual recognition

After Brexit, the UK is no longer part of the EEA, and MiCA’s passport mechanism does not cover the UK. MiCA CASP-authorized firms serving UK clients must separately comply with FCA MLRs registration, financial promotion approval, and FSMA authorization. FCA-registered firms entering the EEA must apply for MiCA CASP authorization from the relevant NCA. There is no mutual recognition between EU and UK crypto regulations.

MiCA vs FCA core differences at a glance

| Comparison Dimension |

MiCA (EU) |

FCA (UK) |

| Legal hierarchy |

EU regulation, applies to all member states |

MLRs registration + FSMA promotion + FSMA expansion |

| Main admission |

CASP authorization (NCA) |

MLRs registration + promotion approval; FSMA authorization expansion |

| Cross-border mechanism |

EEA passport, single authorization, multi-country business |

No passport; no mutual recognition with MiCA |

| Minimum capital |

€50,000–€150,000 or expense ratio |

Lower at MLRs stage; increases with FSMA expansion |

| Client protection |

Whitepaper, asset segregation, complaint handling |

Promotion approval + safeguarding guidelines |

| Stablecoins |

EMT/ART classification, separate issuer authorization |

Independent framework; Bank of England supervises systemic stablecoins |

| Enforcement body |

NCA unified enforcement |

FCA as sole national regulator |

This table presents MiCA and FCA structural differences across legal hierarchy, admission, cross-border, capital, client protection, stablecoins, and enforcement. It does not judge which is superior, but checks obligations by dimension for each jurisdiction.

What this means for users

For retail and institutional users, “where the platform is licensed” is more important for applicable rules than “whether the platform brand is international.” MiCA-licensed CASPs must meet unified standards for whitepaper disclosure, client asset segregation, and capital; FCA-registered firms must comply with UK AML and promotion rules, and FSMA expansion will structurally align protection standards with MiCA, though specific parameters remain set by the FCA.

When reviewing platform compliance, users should confirm: EU MiCA CASP licensing or UK FCA registration, whether approved promotion content is provided in their region, and whether stablecoin products meet local classification requirements. For global trading platforms, Gate global compliance layout explains how license networks are organized by region.

Summary

MiCA covers CASP licensing, stablecoin classification, and EEA passporting under a unified EU regulation; the UK FCA, post-Brexit, operates independently via MLRs registration, financial promotion approval, and FSMA expansion, without cross-border mutual recognition. Comparison should be made across authorization, capital and client protection, stablecoin rules, and cross-border operations, avoiding assumptions that compliance in one country equates to admission in another. Users should choose platforms based on actual licensing status in their target jurisdiction.

FAQ

How do MiCA and UK FCA crypto regulations differ?

MiCA is a unified EU regulation, covering all member states via CASP licensing and EEA passporting; the UK FCA applies an independent MLRs registration and FSMA promotion approval regime post-Brexit, with no EEA passport and no mutual recognition. MiCA emphasizes unified licensing and EMT/ART stablecoin classification; FCA emphasizes national autonomy and staged legislative expansion.

Can a UK FCA-registered firm provide services in the EU?

Not automatically. FCA MLRs registration is not MiCA CASP licensing; firms must apply for MiCA authorization from the relevant NCA to serve EEA users. There is no mutual recognition between the UK and EU post-Brexit.

Can a MiCA CASP license enable business in the UK?

MiCA licensing is only valid within the EEA via passporting and does not cover the UK. Serving UK clients requires FCA MLRs registration, financial promotion approval, and FSMA authorization, with separate admission in the UK.

How do MiCA and UK stablecoin regulations differ?

MiCA classifies stablecoins as EMT and ART, with issuer qualifications, reserve, and redemption requirements; the UK uses an independent framework, with FCA responsible for authorization and the Bank of England supervising systemic stablecoins. Classifications do not automatically correspond. The same stablecoin may be subject to different rules in each jurisdiction.

How should users check platform compliance?

Verify whether the platform has MiCA CASP licensing or FCA registration in the target region, check if promotion content is FCA-approved, and see if stablecoin products meet local EMT/ART or UK stablecoin classification. Product scope and protection standards may vary by jurisdiction; do not assume one country’s license extends to another.

What are the structural differences in client protection between MiCA and FCA?

MiCA requires CASPs to maintain minimum capital, segregated client asset accounts, whitepaper disclosure, and complaint handling, with unified standards across the EEA. FCA currently focuses on MLRs registration and promotion approval, with asset safeguarding subject to FCA guidelines; after FSMA expansion, UK prudential and governance requirements will structurally align more closely with MiCA, but specific parameters remain set by the FCA.