Decentralized exchanges, or DEXs, are one of the most essential pieces of infrastructure in the DeFi ecosystem. Their main function is to enable on-chain asset trading without centralized custody. As blockchain networks have developed, DEX trading models have gradually evolved into different structures. The two most representative models are the order book and the automated market maker, or AMM.

In the early stages of DeFi, limitations in on-chain performance and liquidity made it difficult to directly replicate the traditional order book model on blockchains. The emergence of AMMs lowered the barrier to providing liquidity, allowing users to participate in the market without professional market making. This helped drive rapid growth in on-chain trading.

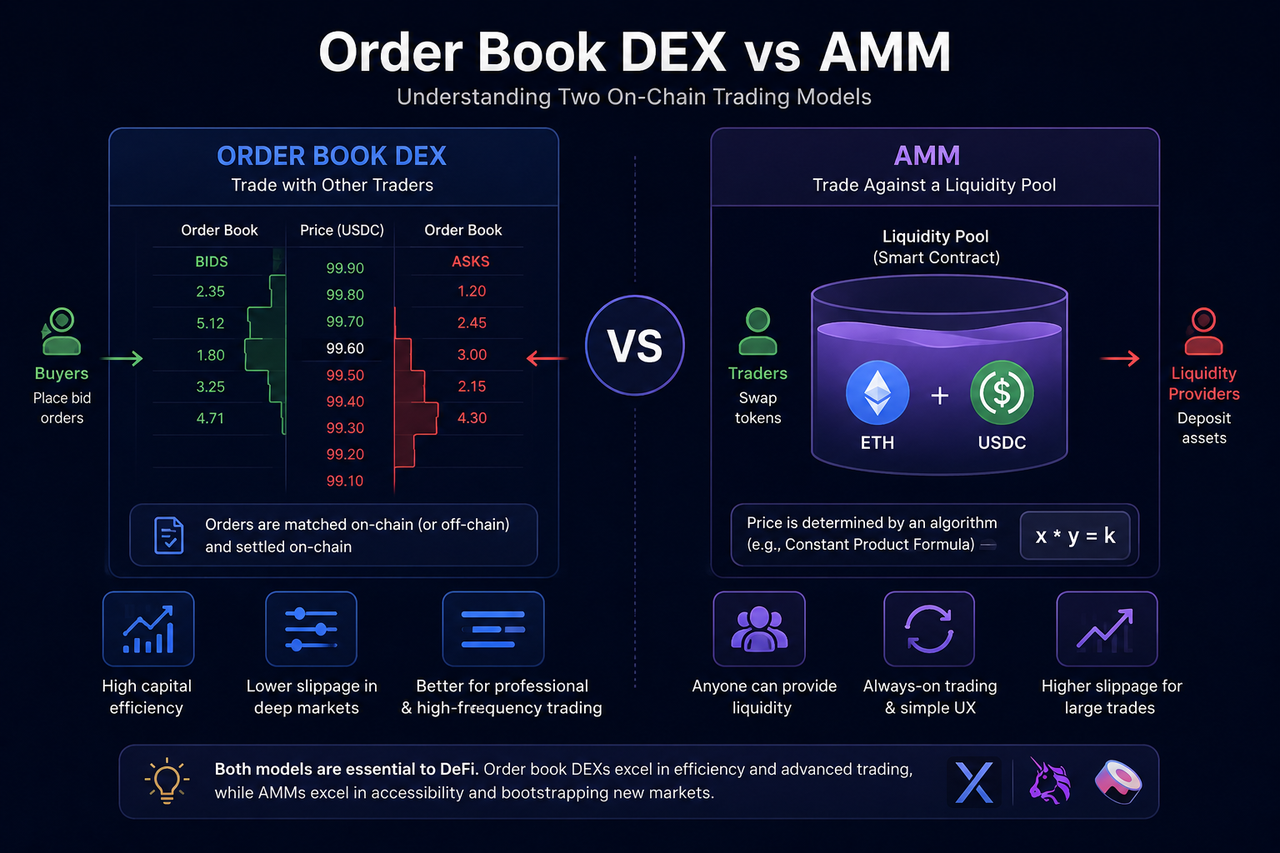

What Is an Order Book DEX?

An order book DEX is a decentralized trading model that matches trades through buy and sell orders placed by market participants. Users can actively set their buy or sell prices, and the system matches orders based on price priority and time priority.

This model is relatively close to traditional financial markets and centralized exchanges, so professional traders usually find its logic easier to understand. An order book displays market depth, bid and ask prices, and order quantities in real time, allowing traders to adjust their strategies based on market conditions.

In an on-chain environment, order book DEXs usually require higher-performance infrastructure because order updates and matching happen far more frequently than in ordinary spot swap scenarios. For this reason, some protocols use a hybrid structure that combines an off-chain order book with on-chain settlement to reduce latency and improve throughput.

What Is an AMM?

An AMM, or automated market maker, is a trading model that uses liquidity pools and algorithms to price assets automatically. Unlike an order book, an AMM does not rely on buy and sell orders placed by users. Instead, it dynamically adjusts asset prices through mathematical formulas.

In the AMM model, users can deposit assets into a liquidity pool and become liquidity providers, or LPs. Other users then trade directly against the liquidity pool. Prices adjust automatically as the asset ratios inside the pool change.

The AMM model greatly lowers the barrier to market making and allows decentralized trading without relying on traditional professional market makers. As a result, AMMs are widely seen as one of the key mechanisms behind DeFi’s large-scale growth.

However, because prices depend on the asset ratios inside the pool, AMMs may experience higher slippage in volatile markets or large trades.

What Is the Core Difference Between an Order Book DEX and an AMM?

The biggest difference between an order book DEX and an AMM lies in their liquidity sources and price formation methods.

An order book DEX depends on traders actively placing orders. Prices are determined directly by buying and selling activity in the market, making the model closer to the price discovery mechanism used in traditional markets. AMM prices, by contrast, are automatically calculated by algorithms based on the asset ratios in liquidity pools.

From a trading experience perspective, the order book model usually offers more precise order control, such as limit orders, stop-loss orders, and market depth views. AMMs place more emphasis on instant swaps and simpler operation.

The two also differ clearly in liquidity structure. AMMs are better suited to long-tail assets and lower-liquidity markets, while order books usually require more active trading markets and more frequent market-making activity.

How Do Order Book DEXs and AMMs Differ in Liquidity Structure?

AMM liquidity mainly comes from liquidity pools supplied by users. Any user can deposit assets into a pool and earn returns from trading fees. This mechanism lowers the barrier to market making and gives new assets more flexibility when launching on-chain markets.

By comparison, liquidity on an order book DEX usually comes from professional market makers or high-frequency trading participants. Because order books need continuous order placement to maintain market depth, they require higher liquidity activity.

When market liquidity is weak, an order book may see wider bid-ask spreads and insufficient depth. An AMM, meanwhile, can maintain basic trading functionality through its liquidity pool. However, when trade size is large, AMMs are more likely to create significant slippage as the asset ratios in the pool change.

Why Do Perpetual Contracts Tend to Use Order Books?

Perpetual contract markets usually involve high leverage, high trading frequency, and rapid price fluctuations, so the trading system needs more precise price discovery and risk management capabilities.

Compared with AMMs, the order book model can provide more detailed order control and a lower-slippage experience, making it better suited to professional derivatives trading. In addition, perpetual contract markets usually rely on funding rates, risk engines, and complex margin mechanisms, which are easier to integrate with an order book model.

For this reason, many on-chain derivatives protocols, including dYdX, use an order book architecture rather than a traditional AMM model.

What Are the Use Cases for Order Book DEXs and AMMs?

AMMs are better suited to spot swaps, long-tail asset trading, and low-barrier liquidity provision. Because they do not require support from professional market makers, AMMs can quickly establish on-chain trading markets, which is why they were widely adopted in the early DeFi market.

Order book DEXs are better suited to high-liquidity markets, high-frequency trading, and complex financial products such as perpetual contracts. For professional traders, the order book structure usually provides an operating experience closer to that of traditional financial markets.

At present, there is no single unified trading model across the DeFi market. Different protocols choose structures based on their own goals. In that sense, order book DEXs and AMMs are better understood as two types of trading infrastructure designed for different needs.

Order Book DEX vs AMM Comparison Table

| Comparison Dimension |

Order Book DEX |

AMM |

| Trading Method |

Order matching |

Liquidity pool swaps |

| Price Formation |

Determined by market buying and selling |

Automatically priced by algorithms |

| Liquidity Source |

Market makers and users placing orders |

Liquidity providers |

| Slippage Performance |

Usually lower |

May be higher for large trades |

| High-Frequency Trading Support |

Stronger |

Relatively limited |

| Perpetual Contract Suitability |

Higher |

Weaker |

| User Barrier |

Relatively higher |

Lower |

| Common Use Cases |

Derivatives, high-frequency trading |

Spot swaps, long-tail assets |

Conclusion

Order book DEXs and AMMs are two of the most important trading models in today’s DeFi market. AMMs lowered the barrier to decentralized trading through liquidity pools and helped drive the early expansion of DeFi. Order book DEXs, by contrast, use a more professional trading structure to support perpetual contracts and high-frequency trading scenarios.

As on-chain finance continues to evolve, the two models are also being combined and optimized. Some protocols are experimenting with hybrid matching structures, while others are further improving order book systems through appchains and high-performance infrastructure. In the future, the DeFi market may not rely on a single trading model. Instead, it is likely to develop diversified trading infrastructure based on different assets and use cases.

FAQs

Why Are AMMs Important in DeFi?

AMMs lower the barrier to market making, allowing users to participate in on-chain trading and liquidity provision without professional market makers.

Why Do Perpetual Contracts More Often Use Order Books?

Because order books are better suited to high-frequency trading, lower slippage, and complex risk management needs.

What Risks Do AMMs Have?

AMMs may face issues such as slippage, impermanent loss, and insufficient liquidity.

Which Trading Model Does dYdX Use?

dYdX mainly uses an order book model rather than a traditional AMM liquidity pool structure.