The key business model concept for SK Eternix is Build-to-Own. It can be understood as "self-developed, self-constructed, self-operated, and held for the long term," rather than pursuing a quick exit after project completion. From a business analysis framework, this model shifts company valuation and risk assessment more toward "operating asset management" rather than "single-project transactions."

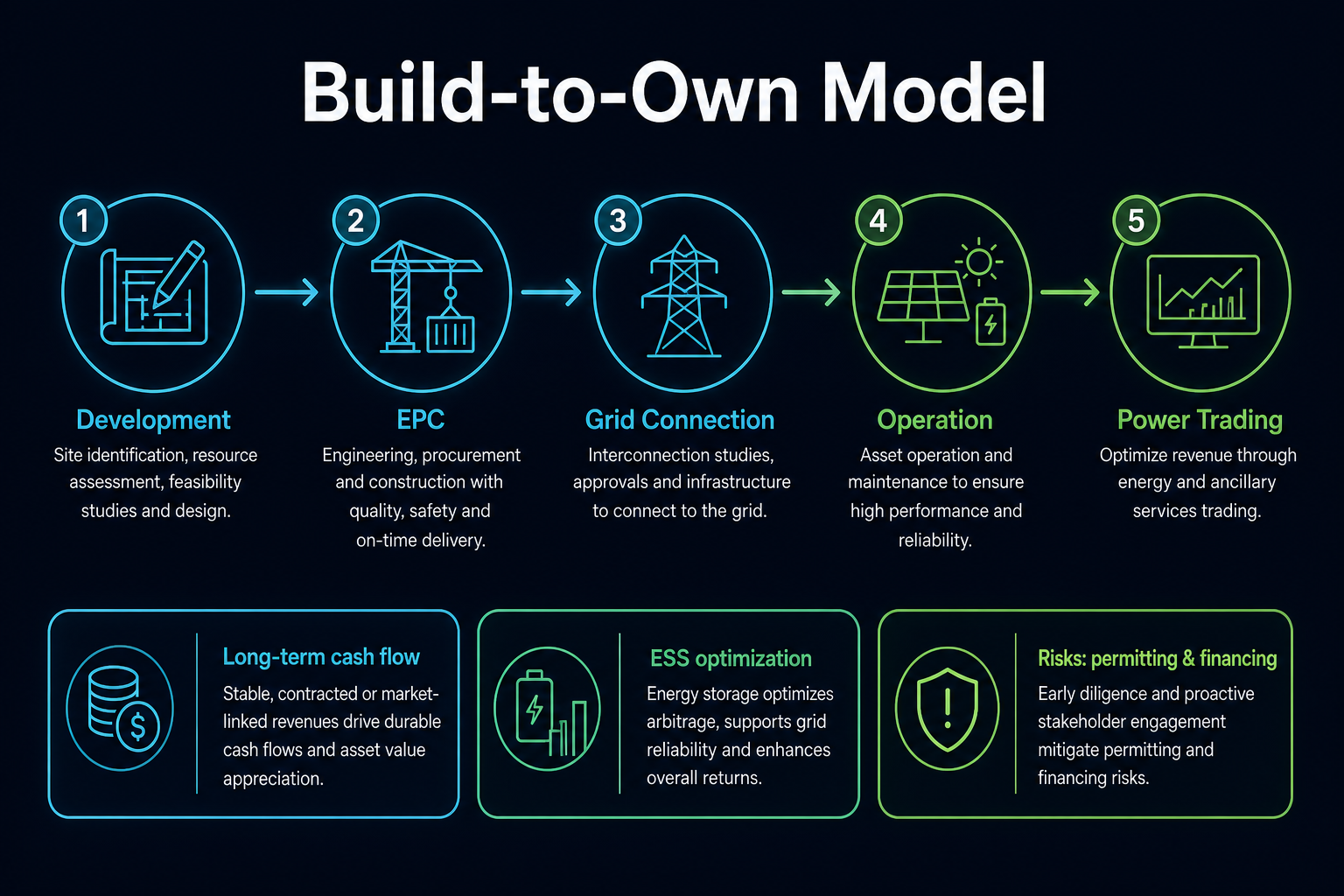

SK Eternix's business does not focus solely on whether a particular renewable energy project is completed, but rather on whether the full chain—from development and construction to grid connection, operation, and power trading—can operate sustainably. Solar, wind, fuel cells, and ESS each play distinct roles in this chain, while power trading capabilities determine how the electricity generated by these assets enters the settlement system.

What Is Build-to-Own? Why Is It SK Eternix's Core Path?

The primary difference between Build-to-Own and Build-to-Sell lies in how profits are realized. The latter emphasizes short-term gains from project exits, while the former prioritizes long-term returns from power generation and operations. SK Eternix's adoption of the former implies a greater reliance on stable operational capabilities, asset management efficiency, and capital cost control.

Figure 1. Build-to-Own model: Development, EPC, grid connection, operation, and power trading together form a long-term asset lifecycle.

Figure 1. Build-to-Own model: Development, EPC, grid connection, operation, and power trading together form a long-term asset lifecycle.

How Is Build-to-Own Different from Build-to-Sell?

Build-to-Own leans toward "asset accumulation," whereas Build-to-Sell leans toward "project turnover." The former requires a longer payback period and places greater importance on grid connection, operational efficiency, and financing; the latter is more concerned with project development, construction handover, and sale windows.

| Dimension |

Build-to-Own |

Build-to-Sell |

| Core Objective |

Hold and operate assets long-term |

Transfer or sell after project completion |

| Source of Returns |

Power generation, electricity sales, operational optimization, power trading |

Project development and sale gains |

| Core Capabilities |

Asset management, financing, dispatching, O&M |

Project development, construction, buyer resources |

| Main Risks |

Grid connection delays, capital costs, policy and regulatory changes |

Project sale windows, development cycles, delivery risks |

This table shows that Build-to-Own is not a "simpler" model; rather, it shifts risks from the sale phase to the long-term operations phase. Consequently, the focus of analysis for SK Eternix shifts from individual project profits to portfolio asset quality and sustained operational capability.

How Does SK Eternix Generate Revenue?

It can generally be broken down into three tiers:

- Power Generation and Electricity Sales Revenue: Continuous cash flow from renewable energy assets after grid connection.

- Operations and Efficiency Gains: Improving asset returns through O&M and dispatching.

- Trading and Synergy Gains: Enhancing revenue stability by combining power trading with ESS.

The strength of this structure is its sustainability; the drawback is higher upfront capital expenditure and greater pressure from investment cycles. Relevant variables can be further tracked against the SK Eternix Risk Indicator Checklist.

The revenue generation process can be understood as the "assetization of projects." Project construction completion is only the first half; what truly affects operational quality is whether the assets can generate power stably after grid connection, complete settlements, control O&M costs, and improve asset utilization efficiency under electricity pricing and dispatching rules.

Why Is Power Trading Capability Important?

For renewable energy companies, generating power is only the first step; the second is achieving optimal settlement under market rules. Trading capability determines how electricity is priced, how it aligns with load, and how volatility is hedged. By placing trading capability at the core, SK Eternix is essentially enhancing "asset monetization efficiency."

Power trading capability also influences the volatility resilience of renewable energy assets. Solar and wind power are intermittent, meaning generation peaks may not align perfectly with demand peaks. If a company has stronger capabilities in trading, dispatching, and energy storage synergy, its generation assets can more easily transform from "pure power supply" to "portfolio operations."

What Role Does ESS Play in the Business Model?

ESS is not an isolated business unit; it is a critical link between power generation and trading. Its typical benefits include peak shaving, valley filling, enhanced dispatch flexibility, and mitigating renewable energy intermittency. For Build-to-Own companies, ESS often directly affects the smoothness of the asset yield curve.

Within an asset portfolio, ESS has both technical and financial significance. While energy storage systems increase upfront investment, they can also improve dispatch flexibility and settlement efficiency. Evaluating ESS requires a holistic view that considers electricity pricing mechanisms, equipment costs, O&M capabilities, and safety regulations.

What Are the Advantages and Limitations of This Model?

Advantages:

- Greater cash flow sustainability once assets are accumulated

- Better resilience to project-level volatility through cross-business synergies

- Continuous potential for operational optimization

Limitations:

- Higher sensitivity to financing costs and interest rate cycles

- Grid connection delays and project postponements directly impact return realization

- More immediate impact from policy and market rule changes

When evaluating whether this model provides a competitive advantage over peers, it is also worth consulting the Korean Renewable Energy Stock Comparison Framework.

Key Metrics for Analyzing SK Eternix's Business Model

Business model analysis should focus on "whether assets can operate continuously" rather than simply counting projects. More explanatory metrics include the progress of projects under construction, grid connection pace, operational availability, power generation efficiency, capital costs, operating cash flow, and changes in power trading rules.

These metrics fall into three categories: project metrics—to evaluate whether assets are commissioned as planned; operational metrics—to assess whether they generate stable cash flow once operational; and financial metrics—to determine if the long-term holding model imposes excessive capital pressure. Analyzing all three groups together yields a more comprehensive understanding of Build-to-Own quality.

It is also important to consider the interdependencies among these metrics. If projects are commissioned on time but operational availability is low, asset quality requires further verification; if operating cash flow improves while capital expenditures also rise, capital demand remains elevated; changes in power trading rules may alter the settlement quality of the same asset. No single metric can cover the complete business model.

Common Misconception: Does Build-to-Own Mean Low Risk?

Build-to-Own does not equate to low risk. While long-term asset holding can enhance cash flow visibility, it also exposes the company to extended periods of financing, O&M, grid connection, and policy risks. Project delays or rising capital costs can put pressure on the long-term operational model as well.

A more accurate view is that Build-to-Own shifts the location of risks. Risks are no longer concentrated on "whether the project can be sold," but rather on "whether the assets can be reliably commissioned, generate power, settle, and cover capital costs." This distinction lies at the heart of the difference between SK Eternix and project-sale-focused companies.

Summary

SK Eternix's business model can be encapsulated as "long-term ownership of renewable energy assets, combined with operational optimization and trading synergies." Understanding this company hinges not on short-term performance fluctuations, but on whether asset commissioning pace, operational quality, and power trading capabilities are advancing in concert.

FAQ

What does Build-to-Own mean for company analysis?

It implies that returns are more a function of long-term operational performance, and valuation is more heavily influenced by asset quality and cash flow stability.

Why does power trading capability affect valuation?

Because the same volume of power generation can yield different cash flow quality depending on settlement efficiency.

Is ESS a cost center or a profit center?

That depends on project structure and market mechanisms; however, in a platform model, it typically serves both efficiency and revenue functions.

Is Build-to-Own suitable for direct comparison with pure EPC companies?

Not entirely. Build-to-Own is more akin to operating asset management, whereas pure EPC companies focus on engineering delivery. Their revenue recognition cycles and risk exposures are fundamentally different.