I. Can You Buy at Limit Down?

You can place orders to buy at the limit-down price, but you need to understand three distinct layers:

-

Trading Permission: In markets with daily price limits (A-share main board ordinary stocks are mostly ±10%, while the STAR Market and ChiNext are ±20%), a stock hitting its limit-down price is not the same as a trading halt. Trading channels generally remain open, allowing you to submit buy and sell orders as usual. The exchange matches orders based on "price priority, time priority."

-

Order Execution Probability: This is where most people get stuck. If there are enough sell orders at the limit-down price, buy orders are relatively easy to fill. However, if the stock is locked at the limit with a massive sell wall (a "one-word limit down"), buy orders will only queue and may never execute that day—or even for several consecutive days. At limit up, "you want to buy but can't"; at limit down, it's often "you want to sell but can't"—opposite directions, but symmetric logic.

-

Investment Rationality: Just because the rules allow it doesn't mean you should. A limit down is frequently the market's way of pricing in short-term risks: earnings blowups, regulatory penalties, industry policy reversals, or panic-driven selling during a broad market rout. Stories of "buying the dip at limit down" for quick profits are shared widely, but the losses from consecutive limit downs, delisting, and prolonged declines are just as real. An execution only means someone is willing to sell to you at that price—it doesn't mean that's the bottom.

So a more accurate rephrasing of "Can you buy at limit down?" is: How hard is it to get filled? And what's the worst that could happen after you buy? The sections below explore the mechanism, recent earnings cases from a flagship company, and risk control boundaries.

II. What Is a Limit Down? Don't Confuse It with a Trading Halt or Circuit Breaker

A limit down occurs when a stock's decline for the day reaches the maximum percentage allowed by the exchange. After that, no trades can execute at a price below that limit-down price (except for newly listed stocks in their initial period or the first day of resumption, where special rules apply). The purpose is to curb excessive daily volatility and give the market time to digest information, not to cancel trading altogether.

| Concept |

Meaning |

Can Orders Be Submitted Normally? |

| Limit Down |

Stock drops to the daily lower limit |

Usually yes; execution depends on the order book |

| Trading Halt |

Trading suspended by the company or regulator request |

No |

| Temporary Trading Halt |

Triggered by abnormal intraday volatility |

Not during the suspension period |

2026 Rule Update (objective information, not advice): The Shanghai, Shenzhen, and Beijing Stock Exchanges' Trading Rules (2026 Revision) state that the daily price limit range for stocks and ETFs is generally 10%. Starting July 6, 2026, the price limit for risk-warned stocks (*ST) on the main board will be adjusted from 5% to 10%. For stocks with a clear delisting expectation, the daily downward adjustment space expands, potentially compressing the path of "slow limit down then escape." Holders should reassess risks against the rule's effective date and their own liquidity needs, rather than simply thinking "more volatility means easier speculation."

III. How Does Order Matching Work at Limit Down?

Keep two rules in mind: Limit down doesn't prohibit buying, but a locked limit down makes execution difficult. The norm is that selling is hard and buying is easy—the reverse is a red flag.

Scenario 1: Limit Down Opens or Repeatedly Opens

Selling pressure is heavy, but some holders are still willing to sell near the limit-down price, so buy orders can fill relatively easily. This is the most common setting for "buying the dip at limit down"—but it can also be a liquidity trap. You think you're catching a bargain, but larger players may be using your buy orders to reduce their own positions.

Scenario 2: One-Word Limit Down

Sell orders pile up like a "wall" at the limit-down price. Buy orders can only queue, with execution uncertain. If consecutive one-word limit downs follow, queuing buyers may only get executed at even lower prices—the risk of catching a falling knife is real.

Scenario 3: You Want to Sell

Sell orders must join the limit-down queue. If buy orders are insufficient, you can't sell. Anxiety can easily drive you to blindly cut losses during the next day's pre-market auction, often at a higher cost than a pre-planned exit.

Matching follows price priority and time priority. The operational takeaway is: You can buy, but first check the Level 5 order book, the size of the order wall, turnover rate, whether the stock is ST, the company's evening announcements, and industry news. The rules may open the door, but that doesn't mean the market welcomes you in.

IV. Lesson from NVDA's "Earnings Beat, Stock Pullback": A Good Company ≠ A Good Entry Point

Global AI computing leader NVDA reported its quarterly earnings on May 20, 2026: revenue of approximately $81.6 billion, up about 85% year-over-year; data center revenue of about $75.2 billion, up about 92%; EPS beat market expectations. Next quarter's revenue guidance was approximately $91 billion (±2%), and the company announced expanded buybacks, increased dividends, and other shareholder return initiatives.

According to the simple logic that "good earnings should mean a price surge," the stock should have jumped. Instead, it pulled back. Market interpretation centered on: expectations were already fully priced in ("buy the rumor, sell the fact"); the guidance, while high, did not significantly exceed the most optimistic scenario; any "not good enough" is magnified when valuations are stretched; and gross margin and supply chain details introduced noise. Many semiconductor stocks had already rallied ahead of the earnings release, and profit-taking after good news is not uncommon in strong sectors.

Direct implications for A-share limit downs:

- Good financials ≠ short-term price direction upward; a deep drop ≠ sufficient margin of safety.

- Institutions price expected future cash flows and expectation gaps. If retail investors look only at "it fell today, it's cheap," they can easily mistake a price change for a value discount.

- NVDA doesn't have an A-share style 10% daily limit down; its daily swings can be larger. In A-shares, a limit down may look like "one day's drop is enough," but it could actually be just the first day of risk release.

Other semiconductor players like AMD and ARM also see sharp swings with earnings seasons. Familiar brand names don't replace position discipline and stop-losses. First ask why it's falling, then ask whether to buy—this rule matters more than any "limit down buying tip."

V. Which Limit Downs Are More Dangerous?

Not all limit downs are equal:

- Sentiment and Index Co-Movement

The broader market or sector declines systematically, dragging a stock to limit down. If the company's fundamentals haven't deteriorated and the limit down opens with sufficient turnover, a rebound may be possible—but you need logical and data-driven verification, not a "it's fallen a lot" bet.

- Earnings or Policy Shock

Earnings blowups, regulatory penalties, or industry policy shifts. A limit down may be the start of a revaluation, possibly followed by consecutive limit downs or prolonged declines.

- ST, Delisting, or Illegality (Extremely High Risk)

Stocks on the path to ST, major violations leading to mandatory delisting, etc. Limit downs may be accompanied by trading halts for investigation, risk warning announcements, or face-value delisting. After July 2026, when ST price limits widen to 10%, the speed of price adjustment toward intrinsic value could accelerate.

- Liquidity Drying Up

Small caps, high pledge ratios, incomplete major shareholder reduction plans. Even small sell orders at limit down can lock the price. Buyers may face an "easy to buy, hard to sell" situation.

- Theme Fading

Stocks that have surged on pure concept hype. A limit down often marks the distribution phase, not simply "major player shaking off weak hands."

VI. If You Insist on Trading Near Limit Down: A Discipline Checklist

If you still consider buying near the limit-down price, turn impulse into a testable process (losses remain possible; the following cannot eliminate risk):

- Read Announcements First: Look for earnings forecast revisions, regulatory investigations, lawsuits, changes in actual controller, major share reductions, etc. If there are no company announcements, also assess whether it's a sector-wide sell-off.

- Check the Order Wall and Turnover Rate: One-word limit down with a massive order wall → default to not chasing. Limit down opens with sufficient turnover → still consider the trend; don't assume a bottom just because it opened.

- Position Limit: A single stock should be a very small percentage of your total assets. Never use margin to go all-in on a falling knife.

- Dollar-Cost Averaging and Stop-Loss: You can buy in batches, but set a strict price or time stop-loss. A-shares are T+1; shares bought today can only be sold the next trading day, and a gap down overnight is common.

- Distinguish Speculation from Investment: Investment looks at multi-year cash flows and competitive moats; speculation follows capital and sentiment. Don't bear speculative-level risk under the guise of investment.

- Beware of Narratives, Focus on Your Position: Online "limit down suicide squads" are mostly survivorship bias. If you already hold a limit-down stock, prioritize whether you can sell and whether you need to cut losses during the auction period, rather than "buying more to average down." Averaging down in a downtrend can amplify losses.

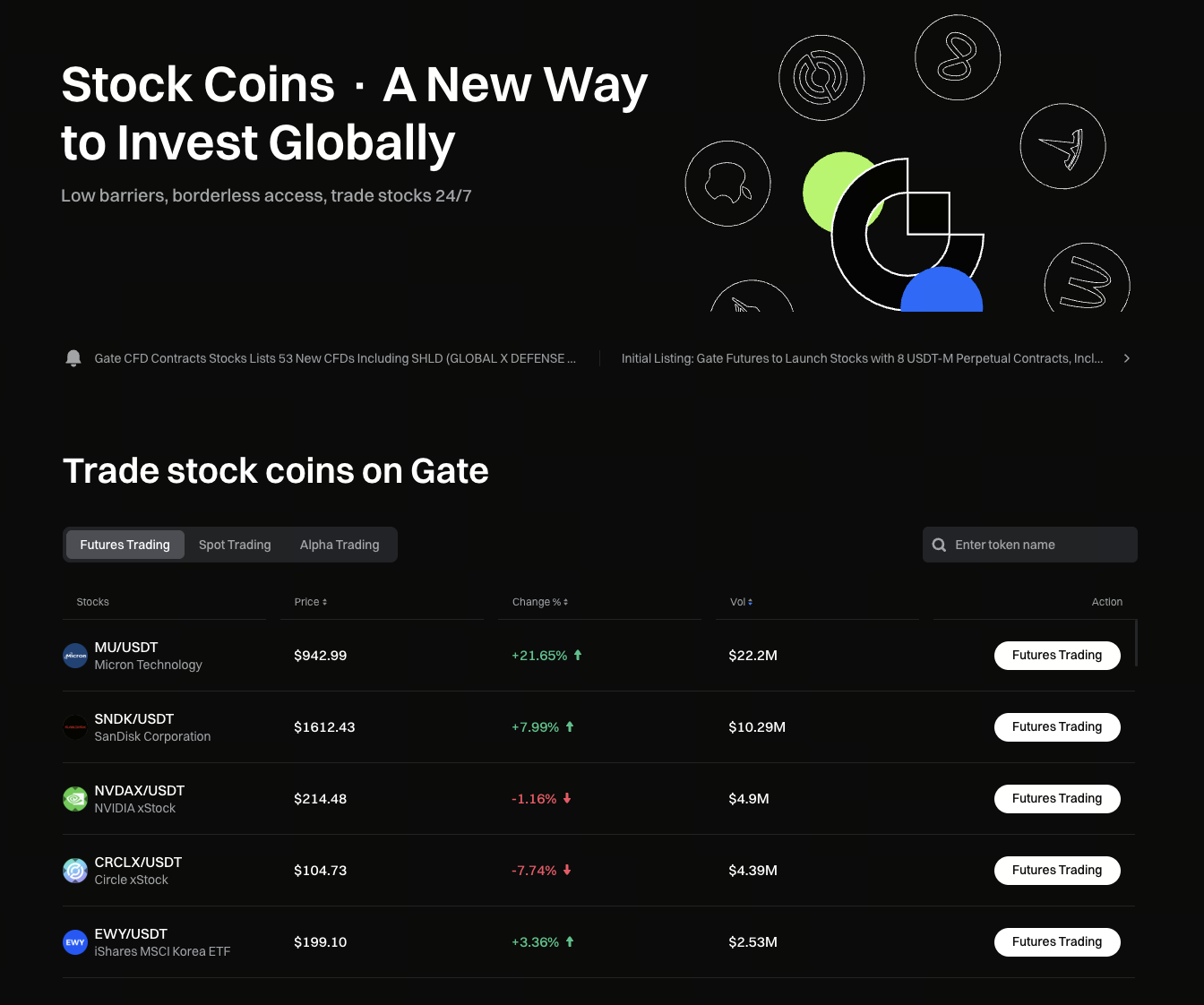

VII. What Are Gate Tokenized Stocks?

Gate Tokenized Stocks are tokens that mirror the share prices of listed companies on the platform (e.g., NVDAX tracks NVIDIA). You buy and sell them with USDT, and they support 7×24 trading. They track price, not the actual shares—generally no voting rights or dividends. And this is not the same as "can you buy at limit down in A-shares" — here there are no daily price limits, so volatility can be higher.

Common uses: hold tokens spot; trade futures contracts long or short (with leverage, higher risk). During earnings seasons, holidays, etc., the tokens may still trade when the underlying market is closed; prices can deviate from the underlying, and liquidity may thin.

VIII. Quick Q&A

-

Q1: Can you buy and sell at both limit up and limit down?

Generally, both can be submitted as orders. At limit up, buy orders are hard to fill, sell orders easy. At limit down, sell orders are hard to fill, buy orders relatively easier (depending on the order book).

-

Q2: If I buy at the limit-down price, can I sell the same day?

A-shares are T+1: shares bought today can only be sold the next trading day.

-

Q3: If I buy at limit down near the close, will it rebound the next day?

No fixed pattern. It depends on whether the negative news is fully priced in, whether capital is willing to step in, and the broader market environment.

-

Q4: Can this be compared to a big drop in overseas leaders like NVDA?

Trading mechanisms differ, but the psychology of expectation gaps and "buy the rumor, sell the fact" is similar. Do not assume that any A-share limit down will V-shape reverse just because a few global leaders have strong long-term trends.

-

Q5: How does the July adjustment to ST rules affect buying at limit down?

After the price limit expands from 5% to 10%, daily price discovery speeds up. The risk structure of blindly bottom-fishing *ST stocks is changing; you need to reassess, not rely on old experience.

IX. Risk Warning and Disclaimer

This article is an educational overview of securities concepts, compiled from publicly available information and general trading rules. It does not constitute any investment advice, return guarantee, or buy/sell recommendation. The stock market carries the risk of principal loss. Buying near the limit-down price may lead to rapid losses, inability to sell due to insufficient liquidity, special treatment, and delisting. Investors should assess their own risk tolerance, read company announcements and exchange rules, and consult licensed professional institutions when necessary. Past cases and recent market conditions do not represent future performance. References to NVDA, AMD, ARM, NVDAX, etc. in this article are solely examples of market phenomena and do not indicate a bullish or bearish view on any target. Tokenized stocks and futures trading carry extremely high risk and may result in a total loss of principal.