1. Starting Point: What Users See as a "Swipe" Is Actually a Settlement Chain in the Backend

Lesson 1 mapped the market by product type. Lesson 2 addresses the following: When a POS terminal or online checkout displays "payment successful," what actually happens to the assets on-chain or within the platform? What does the merchant ultimately receive, and why do issues such as "small losses right after payment" or "different transaction amounts in different regions for the same purchase" sometimes occur?

Crypto payment cards do not transfer Bitcoin directly to the supermarket cashier. Merchants typically still price and settle in fiat currency, and card networks (mainly Visa or Mastercard) still participate in authorization and settlement. The difference is that the cardholder's funding source is digital assets in their payment account, and the issuing partner converts the specified asset into a fiat value usable for card network settlement at the moment of authorization or during clearing according to rules. Understanding this chain is foundational for subsequent discussions on fees, disputes, refunds, and risk management.

2. Participants and Roles: Who Does What in the Process

A typical crypto card transaction involves at least five roles:

-

Cardholder and payment account. Funds are first held in the platform's Payment Account or equivalent module, where users can set a default deduction asset (e.g., USDT) and alternative assets (e.g., BTC, ETH). Spending instructions originate here, not directly from an on-chain wallet address to the merchant.

-

Issuer and card program operator. Responsible for card product rules, cooperation with card networks, risk control strategies, cashback and rewards rules, and connecting platform assets with the funding required by the card network. Gate Card operates under an exchange ecosystem issuance path: spot or trading account → transfer to payment account → card deduction.

-

Card network. Provides a global acceptance network, defines authorization message formats, clearing cycles, and dispute resolution frameworks. User cards commonly display Visa or Mastercard logos, but acceptance does not mean all merchant categories are always unrestricted.

-

Acquirer and merchant. Merchants receive settlement funds in their contracted currency; paying with crypto assets from the cardholder side does not change the underlying structure of "merchant receives fiat."

-

Currency conversion and liquidity provider (possibly embedded in the issuing chain). When the deduction asset differs from the settlement currency, conversion is completed at a quoted rate. This often corresponds to the FX spread felt by users and is a major source of implicit cost.

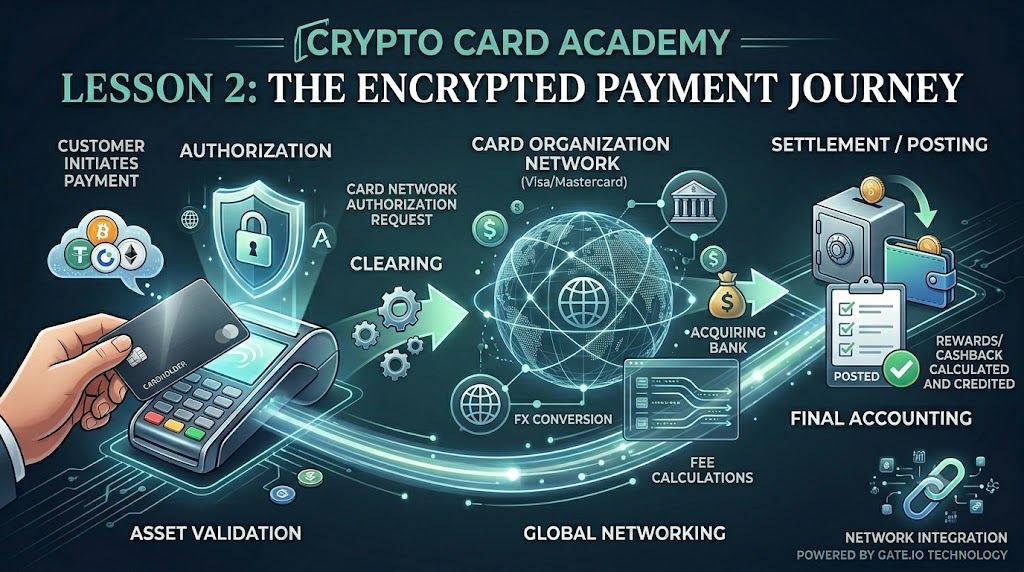

3. Timeline: Authorization, Clearing, and Posting Occur at Different Times

Many users equate a successful swipe with full deduction and locked-in exchange rates, but in reality, a card transaction typically involves three distinct stages—swipe success is only the first step.

-

Authorization. The checkout system sends a request to the issuing network to ask if this deduction is allowed. The issuer responds with approval or denial based on payment account balance, risk rules, single/ daily limits, etc. During authorization, the corresponding amount is usually frozen or reserved, and a Pending record may immediately appear in the app.

-

Clearing. Within the clearing cycle, transaction details are reconciled between card networks and acquirers. The amount may be adjusted slightly from the authorized value due to tips added later, final exchange rates, cross-border fees, etc.

-

Settlement / Posting. Pending transactions become completed; the payment account is debited for the final amount, and cashback or rewards are calculated based on this. For Gate Card products, points or cashback confirmation typically occurs "several days after transaction completion," which relates directly to the distinction between Pending and Posted.

Instructionally, remember: Authorization success does not mean the final deduction amount is fully determined; disputes, refunds, or partial reversals mostly occur at different stages around clearing.

4. Deduction Asset and Auto FX: Why Default Currency Matters

Using Gate Card's interface as an example: The payment account can display balances in USDT, BTC, ETH, GT, etc., along with approximate fiat valuations. Users can select a Default deduction asset.

If USDT or other stablecoins are set as default, conversion volatility is relatively low—closer to spending with USD purchasing power. If BTC or ETH is set as default, asset prices may fluctuate between authorization and posting: while fiat transaction amounts are fixed, the number of tokens deducted may vary with market changes. This is not due to extra deductions by the card network but reflects volatility in the deduction asset itself.

"Automatic conversion" means users don't need to manually sell crypto for fiat before spending; the system handles asset-to-settlement conversions in the backend. This does not mean zero cost or zero spread, nor does it guarantee that rates always match spot market best prices.

5. Where Prices Come From: Authorization Price, Clearing Price, Display Price

Users may see three related but different figures across interfaces:

-

Merchant's listed price and authorization request amount—based on local fiat or acquiring currency (e.g., $100).

-

Payment account deduction amount—mapped to USDT or other deduction assets per issuer's FX rate and fee rules; conversion fees or spreads may apply.

-

In-app fiat valuation—shows approximate USD value that updates with market rates for reference only; not necessarily equal to each transaction's final clearing rate.

For cross-border transactions, there may be additional layers: issuer FX fees, card network cross-border fees, dynamic currency conversion (DCC) choices (if merchants ask about settling in local currency). All these can result in different net values shown in your account for the same listed price.

6. Online, Offline, and ATM: Same Pathway, Different Friction

Offline POS (insert/tap), online card number entry or Apple Pay / Google Pay binding all follow similar authorization logic; differences mainly lie in risk control and failure rates.

Online subscriptions may repeatedly run small test authorizations before actual charges; Pending records may persist longer. Some offline merchants pre-authorize then settle later (e.g., hotels, car rentals), so final charges can exceed authorized amounts.

ATM cash withdrawals (if supported) are usually charged separately: withdrawal fee, FX fee, possibly no cashback or rewards. Support status, limits, and rates are subject to current Gate Card terms. Cash withdrawal essentially turns digital assets into cash—costs are usually higher than regular spending.

7. Failures, Chargebacks & Duplicate Charges: Mechanism-Level Causes

Common reasons for payment failures include: insufficient payment account balance (including Pending holds), exceeding single/ daily limits, risk interception (unusual regions/merchant categories), inactive or expired card, network timeout leading to unconfirmed authorization.

Duplicate charges or apparent double deductions sometimes result from pre-authorization plus final settlement records; other times from canceled authorizations followed by re-posting—distinguished by reconciliation cycles and merchant types. Long-standing Pending holds can be checked per issuer instructions or customer service processes.

Unlike traditional bank cards, most crypto card disputes are still handled within card network frameworks; however, since funds originate from payment accounts, refunds may return as stablecoins or original deduction assets—timelines and rates are subject to rules. As highlighted in Lesson 1: this is not bank deposit insurance—relief paths differ.

8. Gate Card's Position in the Mechanism Chain

Based on Gate's public product information: Users transfer USDT and other assets into their Payment Account; virtual cards can be activated instantly; spending deducts from selected assets with backend conversion for settlement with card networks; cashback can reach about 5%, paid in BTC, ETH, USDT, USDC according to promotions and tier rules.

Mechanistically, Gate Card uses a custodial account deduction model: assets circulate within the platform ecosystem; the card serves as a spending interface—not direct on-chain payments. The advantages are a shorter pathway and lower barriers for existing Gate users; what needs understanding are FX rules, Pending vs confirmation cycles, and how deduction asset volatility affects net costs.

9. Lesson Summary

This session reduces crypto card payments to three chains: timeline (authorization–clearing–posting), roles (payment account–issuer–card network–acquirer/merchant), and costs (deduction asset selection–FX–various backend fees). Users should distinguish between authorization success, final deduction amount, and cashback confirmation timing; using stablecoins versus high-volatility assets as default will significantly affect token-based losses for the same spend amount. With this mechanism mastered, Lesson 3 will cover net cost calculation of fees and cashback; Lesson 4 will compare with traditional debit cards.