Interest rates are one of the core variables in global asset pricing. In the crypto market, “rate hikes are bearish, rate cuts are bullish” is a common conclusion, but also the easiest way to lose money. The market often sees situations where “no rate hike but prices fall” or “rates remain high but crypto prices rebound,” such as:

- The market starts trading “future rate-cut paths” ahead of time;

- Strong structural capital inflows exist (such as ETFs, institutional allocations);

- Strong narrative cycles emerge within crypto.

The key reason is: price trading targets not a single rate point, but the future rate path and expectation differentials.

This lesson focuses on three questions:

- First, what do policy rates, nominal rates, and real rates respectively represent;

- Second, why do real rates provide better explanatory power for crypto valuations;

- Third, how to convert rate signals into position and rhythm management.

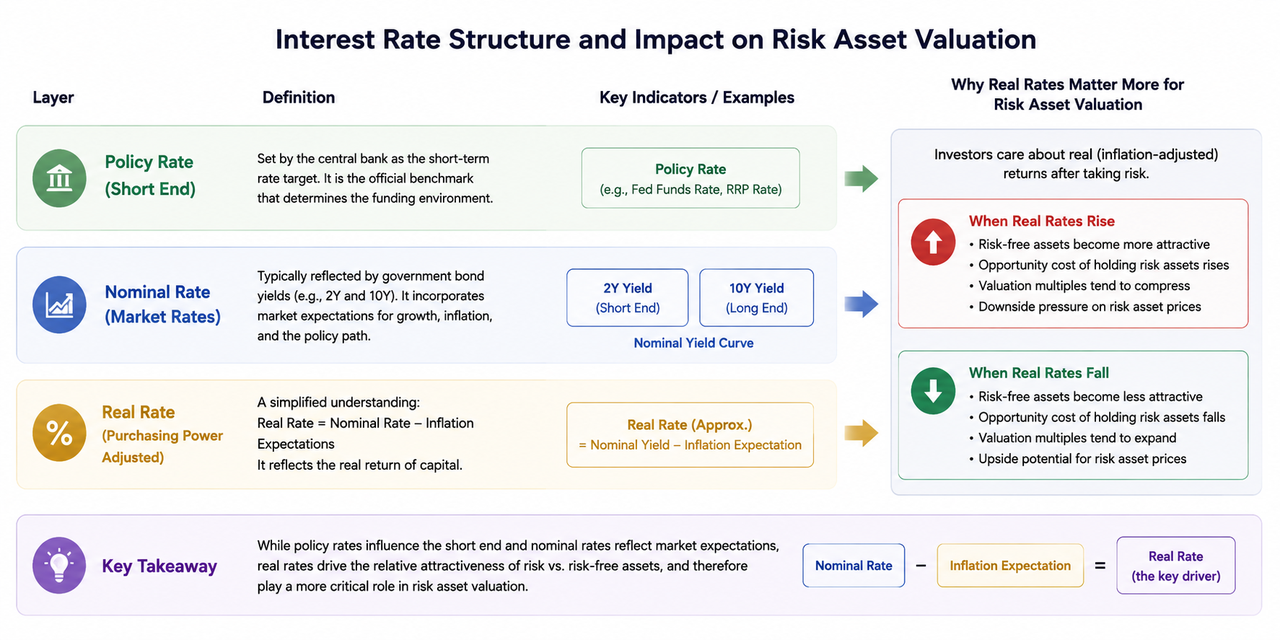

I. Three-Tier Rate Structure: Policy Rate, Nominal Rate, Real Rate

The policy rate is the short-term rate target set by central banks, serving as the official benchmark for the funding environment.

Nominal rates are typically reflected in government bond yields, such as 2Y (2-year US Treasury) and 10Y, capturing market expectations for growth, inflation, and policy trajectory.

Real rates can be simply understood as nominal rates minus inflation expectations, representing the true level of capital returns.

In risk asset valuation, real rates are usually more important than nominal rates. The reason is that capital allocation focuses on real return comparisons after accounting for volatility. When real rates rise, risk-free assets become more attractive and risk asset valuation space compresses; when real rates fall, risk asset valuation elasticity is easier to unlock.

II. Why Crypto Markets Are Highly Sensitive to Interest Rates

Crypto assets are characterized by high volatility and expectation-driven dynamics, with valuations relying more on liquidity and discounted future narratives. Rate changes act simultaneously through three channels: “funding cost—valuation discount—risk appetite”:

- Funding cost channel: rising rates increase leverage costs and put pressure on risk positions;

- Discount channel: higher discount rates compress future expectation valuations;

- Appetite channel: in high-rate environments, defensive assets are relatively favored.

Therefore, on-chain narratives do not have the same effect at all stages. When liquidity is favorable, narratives spread more easily and turn into trends; when liquidity tightens, narratives often only trigger brief rebounds.

III. The Market Trades the “Path” Rather Than the “Current Outcome”

The core of rate trading is not “whether there is a hike this time,” but “how the path over the next 6-12 months is repriced.” Common focus points include:

- Whether the starting point for cuts is pushed back;

- Whether the total number of cuts for the year is reduced;

- Whether the terminal rate is revised higher;

- Whether entering a “higher for longer” phase.

Even if policy rates remain unchanged temporarily, as long as path expectations turn hawkish, risk assets may still pull back. Conversely, even if current rates remain high, as long as path expectations turn dovish, risk assets can recover ahead of time. As a high-beta sector, crypto assets react faster and more dramatically to such expectation differentials.

IV. Key Observation Combinations: 2Y, 10Y & 10Y Real Rate

Looking at a single indicator can easily lead to misjudgment; observing combinations offers more practical value.

- 2Y US Treasury yield: most sensitive to policy expectations; commonly used as a short-to-medium term policy thermometer;

- 10Y US Treasury yield: reflects medium-to-long term growth and inflation expectations;

- 10Y real rate (TIPS): the key anchor for valuation pressure.

Three common combination signals:

- 2Y rising + real rate rising: typically corresponds to strengthening tight policy expectations; risk asset valuations are pressured.

- 2Y falling + real rate falling: usually signals warming easing expectations; probability of risk asset recovery increases.

- Nominal rate falling but real rate not falling: often caused by simultaneous drop in inflation expectations; risk assets may not benefit—interpret cautiously.

V. Layered Crypto Responses to Rate Changes

Under the same rate shock, different assets respond asynchronously:

- BTC: deep liquidity and high institutional participation; often the macro capital’s preferred pricing benchmark;

- ETH: adds ecosystem growth attributes; strong elasticity in tailwind periods;

- High-beta altcoins: stand out when risk appetite rises; retreat faster in headwind periods.

At the initial stage of an improved rate environment, capital usually first flows back to core assets; after further confirmation, elastic capital spreads to high-beta sectors. Conversely, during tightening rate path stages, high-beta assets usually come under pressure first.

VI. Rate Trading in Event Windows: FOMC & CPI

FOMC and CPI often bring high volatility—but the core is not “guessing data,” but “comparing outcomes to expectation differentials.” A three-step process can be used:

- Before the event: record market consensus expectations (number of cuts, dot plot bias, core inflation direction);

- After the event: observe whether 2Y and 10Y real rates show repricing direction;

- Next 1–3 trading days: check whether prices continue; distinguish noise shocks from trend shifts.

If headline news is bullish but real rates don’t cooperate, chasing gains carries higher risk; if headline is neutral but path expectations clearly turn dovish, follow-through is more worth attention.

VII. From Logic to Execution: Rate-Driven Positioning Framework

To translate rate signals into trading actions, follow these principles:

- Real rates keep rising with a strong dollar: reduce total positions and leverage exposure;

- Real rates turn down and risk appetite improves: gradually restore risk exposure;

- During signal conflict: lower trading frequency and prioritize drawdown control;

- Any macro judgment never replaces stop-loss rules: macro handles odds; risk management handles survival.

Stable returns don’t depend on being right every time but on losing less in headwinds and amplifying profits effectively in tailwinds.

Summary

The core conclusions of this lesson are as follows. First, rate analysis must upgrade from “point thinking” to “path thinking”—the market trades future expectations rather than current outcomes. Second, real rates usually explain crypto valuation changes better than nominal rates. Third, rate signals need validation through dollar strength and risk appetite; single-indicator judgments can easily be distorted. Fourth, on execution, rate frameworks should be converted into position rules and risk budgets—not emotional short-term chasing.

If this structure is consistently applied to FOMC, CPI and other key windows, macro variables will shift from being “post-event explanatory tools” to “pre-event decision frameworks.”