This crash happened despite SanDisk’s cumulative gain for the year still exceeding 600%. As of July 13, SanDisk’s gain over the past 52 weeks was as high as 3,531.96%—such an enormous prior surge means that any pullback is enough to trigger the market’s deeper question: whether the “AI storage super cycle” has already ended.

Breaking down the underlying logic behind this collective plunge in memory chips from three dimensions—macro interest-rate environment, geopolitical risk, and industry-cycle logic—and answering a core question: is this truly a trend reversal in AI storage, or just a normal release of risk under stretched valuations?

Triple pressure hits at once: Why did SanDisk become one of the semiconductor stocks with the biggest drop?

The July 14 selloff in memory chips was not triggered by a single factor, but by the convergence of three pressures—macro, geopolitical, and industry.

First pressure: the clearest hawkish warning yet from the Fed.

In a public speech on Monday, Fed Governor Christopher Waller delivered what is, so far, the most explicit hawkish signal. He said that if the core inflation data to be released this week were again “hot,” the Federal Open Market Committee (FOMC) would need to consider tightening monetary policy in the near term. Waller specifically pointed out that demand driven by tariffs, energy prices, and AI infrastructure construction has become an important source of upward pressure on inflation.

This comment directly triggered a reassessment of the interest-rate outlook. After Waller’s remarks, the US 10-year Treasury yield jumped in the short term, rising more than 5.2 basis points to 4.6156%; the 2-year Treasury yield rose about 7 basis points to 4.2773%. The CME FedWatch tool showed the probability the market assigns to a 25-basis-point rate hike in July surged from 26% a week earlier to 41%; pricing by some traders put the hike probability even closer to 50%.

For technology growth stocks whose valuations rely on discounting future cash flows, every lift in rate expectations means a direct compression of valuation multiples. Even though memory-chip companies such as SanDisk and Micron have achieved astonishing performance growth driven by AI demand, their stock prices embed very high forward expectations, making them naturally far more sensitive to rate changes than value-oriented sectors.

Second pressure: Middle East geopolitical conflict escalates abruptly.

The same day Waller spoke, tensions in the Iran-U.S. conflict escalated again. US President Donald Trump announced the restart of the blockade of Iranian ports. Starting at 20:00 Greenwich Mean Time on July 14, the US military carried out a maritime blockade on all Iranian ports and the Iranian coastal regions. International oil prices then spiked, and Brent crude briefly broke above $80 per barrel.

The sharp rise in geopolitical risk weighed on technology stocks in two ways: first, higher oil prices directly boosted inflation expectations, reinforcing the policy-hike logic chain; second, a systemic cooling of risk appetite drove capital out of high-beta semiconductor stocks and into defensive sectors such as energy—on the day, the energy sector jumped 3.2% against the trend, with Exxon Mobil up 4.05% and Chevron up 3.29%.

Third pressure: SK Hynix’s earnings outlook missed expectations, triggering a chain reaction of profit-taking.

SK Hynix’s US ADR listing suffered a sharp drop on just its second trading day. A Korean investment securities firm estimated that its second-quarter operating profit was about 8% below market consensus. Combined with HBM using long-term contract pricing while not being fully able to benefit in the short term from a generalized DRAM price rise, the market began to worry that “rising memory prices may not translate proportionally into corporate profits.”

The impact of this logic is that it undermines the industry’s most core investment narrative—that under AI demand, storage chips see both volume and pricing rise together, creating an ongoing virtuous cycle of expanding margins. As the key supplier of Nvidia’s HBM, SK Hynix’s forecast miss was interpreted by the market as a signal that “AI storage demand may not be infinitely strong.” Selling pressure quickly spilled over to Micron, SanDisk, Western Digital, and Seagate.

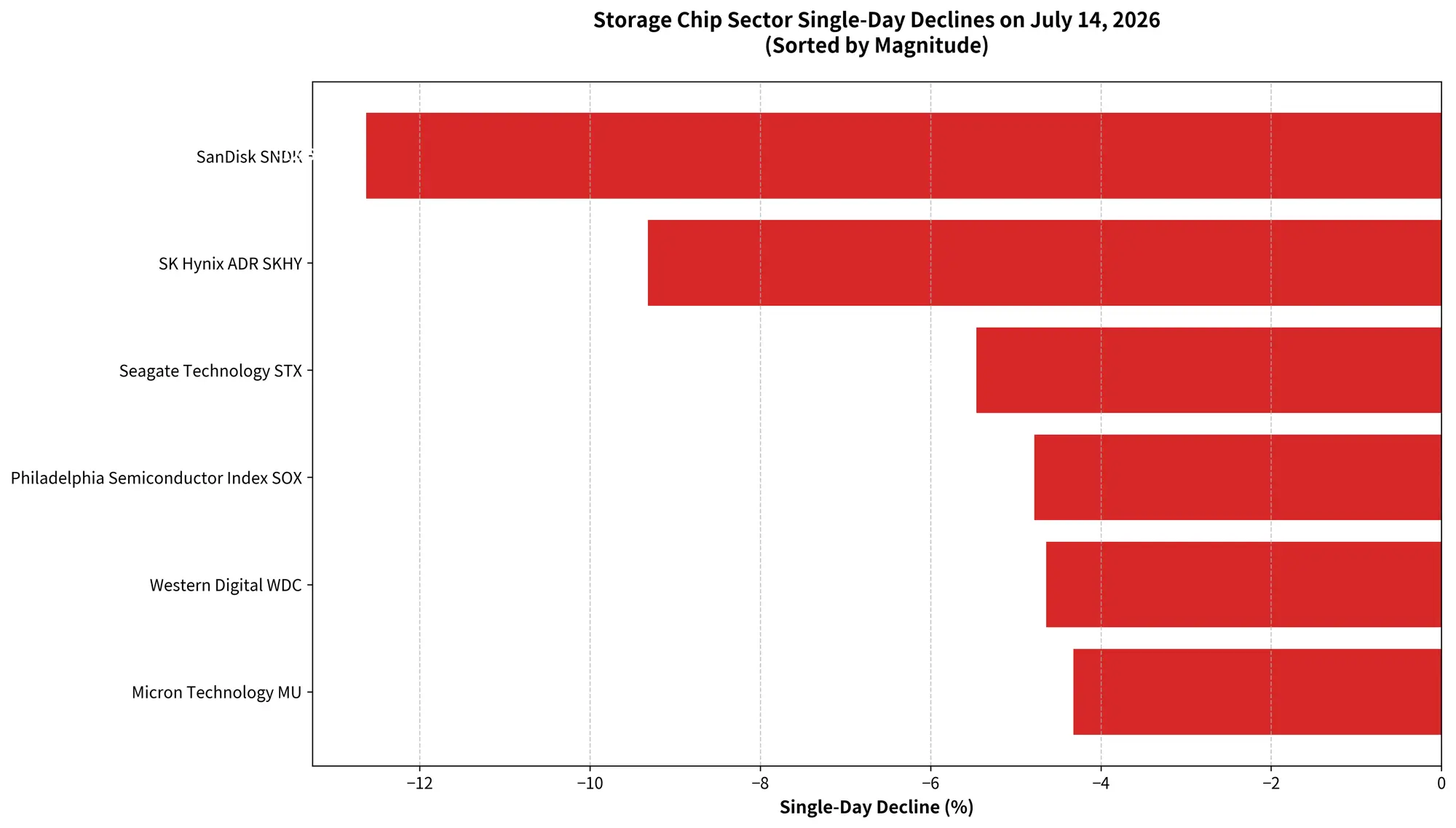

Panoramic view of the memory-chip sector’s losses on July 14

Why SanDisk? The math is inevitable when gains are huge and valuations are stretched

With the entire memory-chip sector dropping, SanDisk led peers with a 12.63% decline. This is not coincidental.

Looking at gains, SanDisk is one of the biggest performers in this AI storage rally. As of July 13, SanDisk’s year-to-date gain in 2026 was still 605.19%. Micron also surged, but its year-to-date gain was around 260%. When facing similar downside shocks, stocks with higher prior gains naturally face heavier pressure for profit-taking—because every 1% drop in share price corresponds to a more substantial amount of market-cap erosion in absolute terms.

From a valuation-logic perspective, SanDisk’s earlier rise had multiple overlapping drivers: a breakout surge in AI server demand for NAND storage, the continued climb in NAND contract prices, and the full recovery of the storage industry following the inventory adjustment cycle in 2023–2024. The market didn’t just price in improving fundamentals—it also priced in the incremental storage demand driven by AI infrastructure investment over the next several years.

However, when the macro environment changes suddenly—higher interest-rate expectations compress valuation multiples, and rising geopolitical risks suppress risk appetite—those stocks that had already “traded too much of the future” become the first targets for adjustment. SanDisk’s 12.63% one-day drop is, at its core, the mathematical inevitability of a high-gain, high-valuation stock facing macro headwinds.

Where is the storage cycle headed? AI demand hasn’t peaked yet, but the market is starting to price “the top”

Does SanDisk’s plunge mean AI storage demand has already peaked? That’s the question investors care about most.

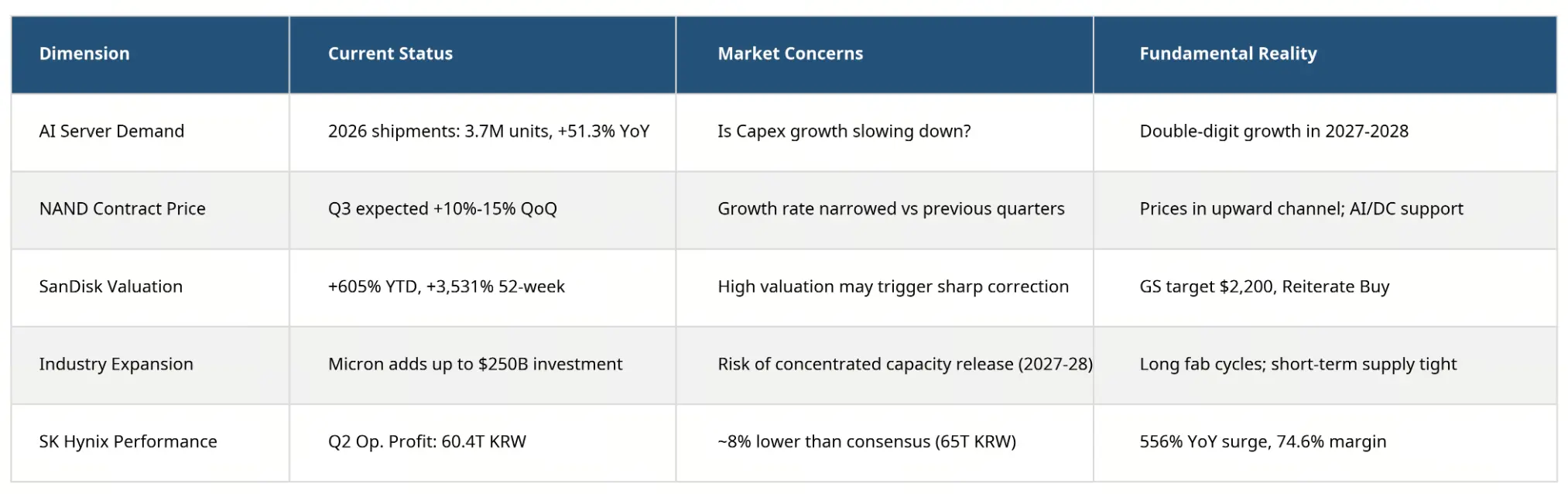

Based on fundamental data, AI storage demand is still growing rapidly. According to statistics from Isaiah Consulting, global AI server shipments in 2026 will reach about 3.7 million units, up 51.3% year over year. In terms of storage-capacity demand, the year-over-year growth in DRAM demand from AI servers in 2026 could reach 105%, while HBM demand’s year-over-year growth could reach 110%. It is expected that by 2028, AI servers will account for 50–55% of global DRAM demand.

In the NAND Flash segment, AI inference and the construction of large data centers remain the key demand supports. As inference workloads surge, AI servers’ demand for storage capacity has already become more than triple that of traditional servers. It is expected that in 2026, enterprise SSDs will surpass smartphones and become the largest application area in the NAND Flash market.

Cloud service providers such as Microsoft, Google, Amazon, and Meta continue to expand GPU clusters and data-center investments. The underlying logic of AI capital expenditure growth did not change meaningfully on July 14.

But the market’s pricing logic is undergoing subtle shifts.

TrendForce data shows that although NAND Flash contract prices are still rising supported by AI demand, the forecast for overall NAND Flash contract prices in the third quarter is a quarter-on-quarter increase of 10% to 15%, but the upside is clearly smaller than in previous quarters. In the NAND Flash wafer space, demand in consumer-level applications—retail, USB flash drives, and memory cards—has remained lackluster. Module manufacturers’ customers have also seen demand stay weak because upstream costs are high and downstream end markets cannot absorb higher prices.

More importantly, supply-side changes are emerging. Micron recently announced that its investment commitment in the US before 2035 will be raised from $200 billion to more than $250 billion. With SK Hynix, Samsung Electronics, and Micron simultaneously stepping up capital expenditures, the market is beginning to worry about the risk of capacity coming online in concentrated fashion a few years down the line—something that is a typical precursor to multiple past cycle turning points in the storage industry.

Therefore, the crash on July 14 is not the market denying AI storage demand; it is the market beginning to price in a “cycle top”—even if that top may still be some distance away.

Storage-chip cycle position and valuation risk matrix

Storage-chip cycle position and valuation risk matrix

From “AI concept rallies across the board” to “finding the true profit earners”

The sector’s collective pullback actually reflects an important differentiation within the AI investment theme.

In the early phase of the AI boom (2024–2025), the market granted extremely high valuation premiums to almost every semiconductor company tied to AI. The logic was simple: AI needs GPUs, needs HBM, needs NAND storage, and needs data-center storage equipment—so the entire supply chain benefits.

But as share prices kept rising and market expectations kept getting elevated, investors started asking tougher questions: which companies’ AI-related revenue can continuously convert into stable earnings growth? Which companies have already had their valuation fully—or even excessively—reflect future growth expectations? When capex growth slows, which companies will be hit first?

The answers to these questions are driving the AI theme from a “rising across the board” phase into a new stage of “structural differentiation.”

Take SanDisk as an example. On July 13, Goldman Sachs raised its price target from $1,200 to $2,200, reiterating a “Buy” rating, and predicted that its results for the fourth quarter of fiscal 2026 would be “very strong.” Evercore ISI analyst Amit Daryanani raised his target price sharply from $1,400 to $3,100, believing investors have “underestimated the durability of SanDisk’s future earnings and free cash flow,” as well as underestimating the company’s ability to further raise prices if supply-demand imbalances persist through 2027. Citigroup also reaffirmed a $2,500 target.

Wall Street optimism contrasts sharply with market panic. This divergence precisely reflects the delicate position the memory-chip sector is in right now: fundamentals remain strong, but valuations already embed extremely high expectations.

From a more macro perspective, the industry’s improving conditions are still in an upward channel, but the phase with the fastest growth may already be behind. For investors, future performance of memory stocks will increasingly depend on one core variable: whether sustained AI demand growth can keep translating into growth in corporate profits—not just staying at the level of revenue expansion.

What should investors watch next?

In the short term, the market will focus heavily on the following key variables:

The Fed’s July policy path. The US Bureau of Labor Statistics will release June CPI on July 15. The market expects the year-over-year increase to slow from May’s 4.2% to 3.8%. If inflation data comes in cooler than expected, rate-hike expectations could cool again, giving tech stocks room to breathe. If core inflation turns hot again, the probability of hikes will rise further. The Fed will announce its next interest-rate decision on July 29.

Semiconductor earnings season. TSMC’s July 16 earnings report will be the first major window to test the strength of AI chip demand. Micron’s subsequent guidance, as well as SanDisk’s fiscal 2026 fourth-quarter report scheduled for August 5, will be key checkpoints for the market to reassess the fundamentals of the memory segment.

AI capex trend. Cloud providers’ capex plans, order status in Nvidia’s supply chain, and how quickly data-center investments translate into real spending will directly affect market expectations for storage demand.

Conclusion

SanDisk’s 12.63% one-day crash and the Philadelphia Semiconductor Index’s 4.78% drop look more like a concentrated release of risk accumulated under high expectations, high valuations, and high price gains—not a trend reversal in AI storage demand.

AI infrastructure investment is still expanding, and the supply-demand fundamentals for memory chips have not deteriorated fundamentally. But the market has already sent a clear signal: the era of “indiscriminate” upside for AI themes is ending, replaced by a pricing environment that is more selective and more focused on the ability to deliver realized profits.

For memory-chip companies, future stock performance will increasingly hinge on one simple—and unforgiving—criterion: whether growth in AI demand can keep translating into growth in profits. Companies that can prove this will regain market recognition after the volatility; those that rely only on industry beta may face a longer valuation-digestion process.

Has the storage industry’s super cycle already reached a turning point? The answer may not be a straightforward “yes” or “no”—a more accurate phrasing is that the market is moving from trading “the story of the cycle” to trading “the numbers of the cycle.”

FAQ

Q: How much exactly did SanDisk’s stock drop on July 14?

SanDisk (SNDK) closed at $1,673.97 on July 14, down $241.95 from the prior trading day, a decline of 12.63%. Trading value was $23.315 billion, the third-largest single stock by trading value that day among US stocks.

Q: Besides SanDisk, which other memory stocks fell in sync?

Micron Technology fell 4.32% to $937, SK Hynix ADR fell 9.32%, Seagate Technology fell 5.46%, and Western Digital fell 4.64%. The Philadelphia Semiconductor Index dropped 4.78% on the day.

Q: How much cumulative gain has SanDisk had since 2026?

As of July 13, SanDisk’s year-to-date gain in 2026 was still 605.19%, and its cumulative gain over the past 52 weeks was as high as 3,531.96%.

Q: How do Fed rate-hike expectations affect semiconductor stocks?

Rate hikes raise the risk-free rate and compress valuation multiples for growth stocks based on discounted future cash flows. Semiconductor companies typically have high growth and high valuations, making them most sensitive to changes in interest rates. After Waller’s speech, the market’s pricing for a July rate hike rose to nearly 50%.

Q: Has AI storage demand really peaked?

From fundamental data, AI storage demand is still growing rapidly—2026 AI server shipments are expected to rise 51.3% year over year, and DRAM and HBM demand will both double. The drop on July 14 is more about valuation adjustments and sentiment release rather than a fundamental reversal.