#SemiconductorSectorTakesAHit

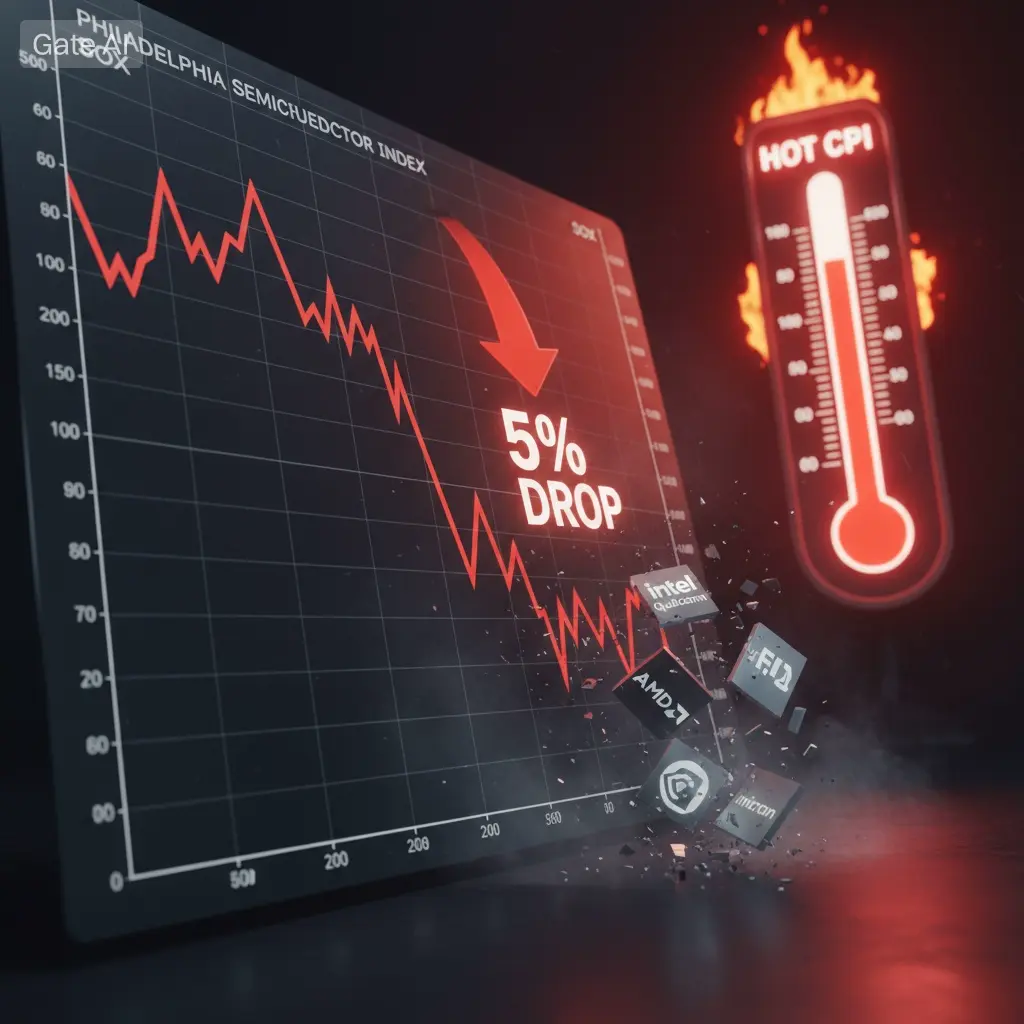

The semiconductor sector did not just experience a normal red day — it experienced a full scale repricing event that may carry major implications for the broader crypto market throughout the rest of May.

The Philadelphia Semiconductor Index collapsing more than 5% intraday sent a loud message across global risk markets. Qualcomm plunged nearly 12%. Intel dropped over 9%. SanDisk lost more than 8%, while ASML, AMD, and TSMC all suffered heavy declines together. This was not isolated weakness. This was coordinated institutional de-risking triggered by one factor the market can no longer ignore: inflation.

The April CPI print at 3.8% completely shifted sentiment. Investors were already nervous about interest rates staying higher for longer, but this number reinforced fears that inflation remains deeply embedded inside the global economy. And when inflation refuses to cool, central banks become aggressive. Aggressive central banks are dangerous for high-growth sectors that depend on future valuation expansion to justify elevated prices.

That is exactly where semiconductors and crypto suddenly intersect.

Most people still treat semiconductors and crypto as separate worlds. In reality, they are becoming deeply connected through AI infrastructure, cloud computing, mining operations, and next-generation data center demand. Companies tied to Bitcoin mining are increasingly transitioning toward AI compute models because the economics of GPU infrastructure are exploding. Hut 8, IREN, and multiple mining firms are now positioning themselves as hybrid AI and energy infrastructure companies rather than simple miners.

This means semiconductor weakness can directly impact sentiment around crypto-related growth narratives.

The market is beginning to question whether the AI boom became overheated too quickly. Micron’s recent 147% rally before its sharp reversal became a perfect example of excessive momentum colliding with macroeconomic reality. Investors chased AI exposure aggressively for months under the assumption that future growth would overpower interest rate pressure. The CPI shock interrupted that belief instantly.

Another major layer involves geopolitics.

Qualcomm executives traveling alongside Trump to China during a period of severe market weakness creates an unusual backdrop. Markets are now balancing two opposing forces simultaneously: economic pressure from inflation and potential optimism surrounding future trade negotiations. Any signal of easing tensions between Washington and Beijing could stabilize semiconductor sentiment temporarily, but uncertainty remains extremely high.

For crypto traders, the lesson is becoming increasingly clear.

Liquidity conditions still control everything.

Bitcoin, Ethereum, AI tokens, and high-beta altcoins all perform best when monetary policy supports risk appetite. When inflation rises and bond yields climb, capital becomes selective. Speculation weakens. Valuation multiples compress. Narratives alone stop carrying markets upward.

This does not mean the long-term crypto thesis is broken.

It means short-term survival depends on discipline, patience, and intelligent positioning. The traders who survive difficult macro periods are usually the ones who understand that preserving capital during uncertainty matters more than chasing every momentum wave.

The semiconductor crash may ultimately become one of the first warning shots signaling that markets are entering a much more selective phase after months of aggressive AI-driven optimism.

Risk management is no longer optional.

It is becoming the entire game.

#GateSquare #ContentMining

#GateSquareMayTradingShare

The semiconductor sector did not just experience a normal red day — it experienced a full scale repricing event that may carry major implications for the broader crypto market throughout the rest of May.

The Philadelphia Semiconductor Index collapsing more than 5% intraday sent a loud message across global risk markets. Qualcomm plunged nearly 12%. Intel dropped over 9%. SanDisk lost more than 8%, while ASML, AMD, and TSMC all suffered heavy declines together. This was not isolated weakness. This was coordinated institutional de-risking triggered by one factor the market can no longer ignore: inflation.

The April CPI print at 3.8% completely shifted sentiment. Investors were already nervous about interest rates staying higher for longer, but this number reinforced fears that inflation remains deeply embedded inside the global economy. And when inflation refuses to cool, central banks become aggressive. Aggressive central banks are dangerous for high-growth sectors that depend on future valuation expansion to justify elevated prices.

That is exactly where semiconductors and crypto suddenly intersect.

Most people still treat semiconductors and crypto as separate worlds. In reality, they are becoming deeply connected through AI infrastructure, cloud computing, mining operations, and next-generation data center demand. Companies tied to Bitcoin mining are increasingly transitioning toward AI compute models because the economics of GPU infrastructure are exploding. Hut 8, IREN, and multiple mining firms are now positioning themselves as hybrid AI and energy infrastructure companies rather than simple miners.

This means semiconductor weakness can directly impact sentiment around crypto-related growth narratives.

The market is beginning to question whether the AI boom became overheated too quickly. Micron’s recent 147% rally before its sharp reversal became a perfect example of excessive momentum colliding with macroeconomic reality. Investors chased AI exposure aggressively for months under the assumption that future growth would overpower interest rate pressure. The CPI shock interrupted that belief instantly.

Another major layer involves geopolitics.

Qualcomm executives traveling alongside Trump to China during a period of severe market weakness creates an unusual backdrop. Markets are now balancing two opposing forces simultaneously: economic pressure from inflation and potential optimism surrounding future trade negotiations. Any signal of easing tensions between Washington and Beijing could stabilize semiconductor sentiment temporarily, but uncertainty remains extremely high.

For crypto traders, the lesson is becoming increasingly clear.

Liquidity conditions still control everything.

Bitcoin, Ethereum, AI tokens, and high-beta altcoins all perform best when monetary policy supports risk appetite. When inflation rises and bond yields climb, capital becomes selective. Speculation weakens. Valuation multiples compress. Narratives alone stop carrying markets upward.

This does not mean the long-term crypto thesis is broken.

It means short-term survival depends on discipline, patience, and intelligent positioning. The traders who survive difficult macro periods are usually the ones who understand that preserving capital during uncertainty matters more than chasing every momentum wave.

The semiconductor crash may ultimately become one of the first warning shots signaling that markets are entering a much more selective phase after months of aggressive AI-driven optimism.

Risk management is no longer optional.

It is becoming the entire game.

#GateSquare #ContentMining

#GateSquareMayTradingShare