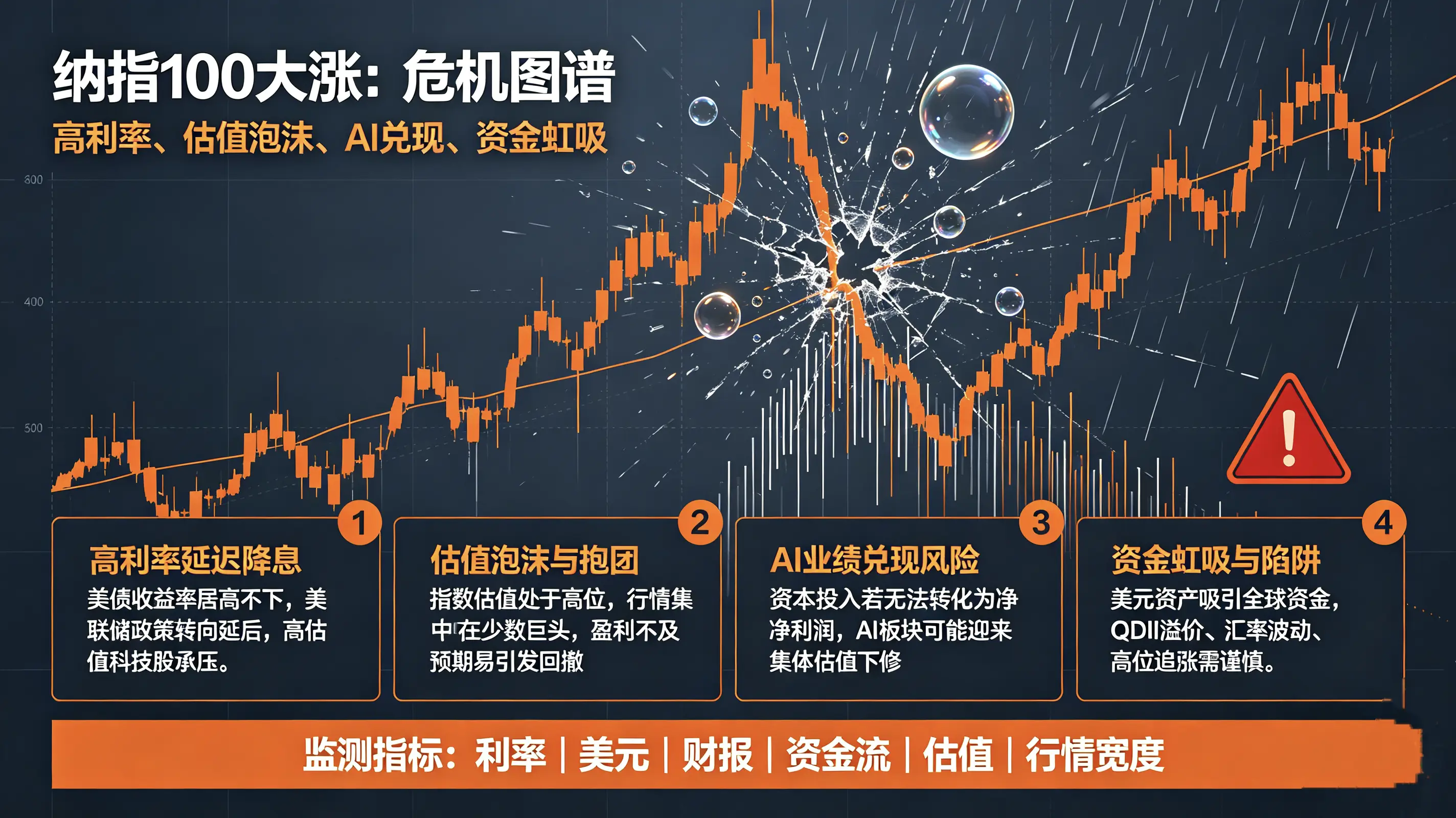

Nasdaq Index Short-Term (2026 Q3, July–September): High Probability of a Technical Correction of Around 10%

Probability of Decline: 70%–80%

Core Drivers

1. Valuation Bubble, Highly Concentrated Capital (Biggest Internal Risk)

This rally has been entirely driven by the seven major AI tech giants. The S&P 500 valuation is in the top 5th percentile historically. The forward P/E ratio premium relative to U.S. Treasury yields continues to narrow, significantly weakening value-for-money. Renowned investor Grantham believes the current market bubble exceeds the 2000 dot-com bubble, with AI growth stocks pulling forward several years of earnings expectations.

Bank of America's technical model confirms weakening upward momentum. The S&P 500 has already hit its annual target of 7,430 points. After hitting a new high in June, clear bearish divergence has emerged, predicting a three-wave correction in Q3, with a minimum drop to 6,850 points, a maximum drawdown of about 7.6%, and an extreme case of a drawdown of 10%+.

2. Repeated Expectations of Fed Policy Shifts, High Interest Rates Suppress Valuations

In May 2026, core CPI was still at 2.85%, well above the 2% target. The new Fed chair's stance leans hawkish, with major institutions deeply divided: the optimistic camp expects no rate hikes for the year, while Bank of America predicts three rate hikes within the year. As long as inflation rebounds slightly, the market will quickly price in higher rates, directly pressuring growth stock valuations. Moreover, with the current benchmark rate of 3.5%–3.75% maintained long-term, corporate financing costs have risen significantly.

3. Seasonal and Technical Selling Pressure

- Q3 has historically been a weak window for U.S. stocks, compounded by quarter-end rebalancing by pension funds and sovereign wealth funds. Stocks have significantly outperformed bonds, forcing institutions to passively reduce equities and increase bonds.

- Market leverage has risen, with margin debt and call option trading volumes surging. Once a decline occurs, it could trigger a stampede.

- A large number of AI and tech IPOs are concentrated, surging stock supply and diverting market liquidity.

4. Downside Risk to Earnings Expectations

Current Q2 earnings growth expectations are 23.1%, supported by high government deficit spending and households depleting savings. Tariff policies continue to raise corporate costs, with consumption momentum weakening in the second half of the year. Q3 earnings reports are likely to miss expectations, directly triggering a sell-off.