Abstract

-

The crypto market has long continued to use the Beta framework from traditional finance to explain systematic risk, but a growing body of research shows that this framework faces clear limits in digital assets.

-

From the perspective of market structure, crypto asset returns are jointly driven by high volatility, jump events, liquidity stratification, sector rotation, on-chain behavior, and macro factors, making it difficult for a single market factor to stably characterize true risk exposure.

-

Public research shows that the explanatory power of historical Beta for future Beta is significantly weaker in the crypto market than in mature equity markets. Although optimized estimators can improve results, the magnitude of improvement is limited.

-

At the hedging level, performance differences among different market indices are very large, and only a small number of assets can achieve statistically significant better risk compression through market Beta hedging.

-

Therefore, the focus of future digital asset risk modeling should not only be “estimating Beta more accurately,” but should shift toward “redefining the market factor,” and introducing on-chain, sentiment, macro, and structural variables to form a multi-factor risk representation.

1. Introduction

In traditional finance, market Beta is the core language for understanding systematic risk. It represents the extent to which an asset moves together with the overall market, and further affects asset pricing, portfolio allocation, and hedge ratio design. For mature equity markets, even though Beta may drift, its statistical stability, index definition, and institutionalized trading environment still give this framework considerable practical usefulness.

But the structure of the digital asset market is clearly different from that of the traditional equity market. Its asset life cycles are shorter, liquidity discontinuities are more obvious, tail events are more frequent, and the speed of switching market narratives is much faster than in equity, foreign exchange, or futures markets. More importantly, there is no unified answer in crypto to the question of “what the market itself is.” Can Bitcoin represent the market? Is a market-cap-weighted broad index sufficient? Are on-chain activity, stablecoin inflows, and risk appetite more important than price indices at some stages? These questions determine that Beta in the crypto market is not a naturally stable statistical object, but more like a conditional variable that is reconstructed as the environment changes.

Research by Härdle, Harvey, and Reule points out that the crypto market provides an extremely rich data environment for financial research, but its mechanisms differ greatly from traditional assets, and many classical financial tools need to be revalidated in this market. New research around predictability, jump behavior, market microstructure, and multi-source data modeling also points to the same conclusion: the risk explanation framework for digital assets must be redesigned and cannot simply be transplanted.

This paper attempts to answer three core questions:

-

Is Beta in the crypto market predictable?

-

Can Beta effectively support risk hedging?

-

If single-factor Beta has limits, how should the future risk framework be reconstructed?

2. Systematic Risk in the Crypto Market

The reason the Beta framework can operate in traditional markets is that it assumes the existence of a relatively stable, tradable “market portfolio” that can represent overall risk appetite. In crypto, however, systematic risk itself is layered. It includes at least four intertwined sources.

-

The first layer is common risk at the price level, such as changes in risk appetite, contraction in macro liquidity, or broad style rotation.

-

The second layer is market microstructure risk, including insufficient order book depth, cross-exchange spreads, amplification of liquidation chains, and instantaneous evaporation of liquidity.

-

The third layer is asset structure risk. Differences in token circulation mechanisms, unlock schedules, staking constraints, and use cases mean that their responses to “market volatility” are not consistent.

-

The fourth layer is on-chain and narrative risk. Protocol upgrades, governance events, regulatory expectations, changes in stablecoin minting and redemption, and social media attention can all alter the return distribution in a short period of time.

This means that two assets that both seem to belong to “crypto assets” may in fact be dominated by completely different driving factors. Large-cap assets are more likely to display some characteristics close to a market proxy, while mid- and small-cap tokens are more likely to be dominated by idiosyncratic events and liquidity shocks. Under this structure, using a unified index to measure the market Beta of all assets will naturally encounter distortion.

3. Beta in the Crypto Market

Research surrounding the risk explanation of crypto assets has not simply concluded that “Beta is meaningless.” A more accurate statement is that Beta still has informational value, but its stability and transferability are far lower than in traditional markets.

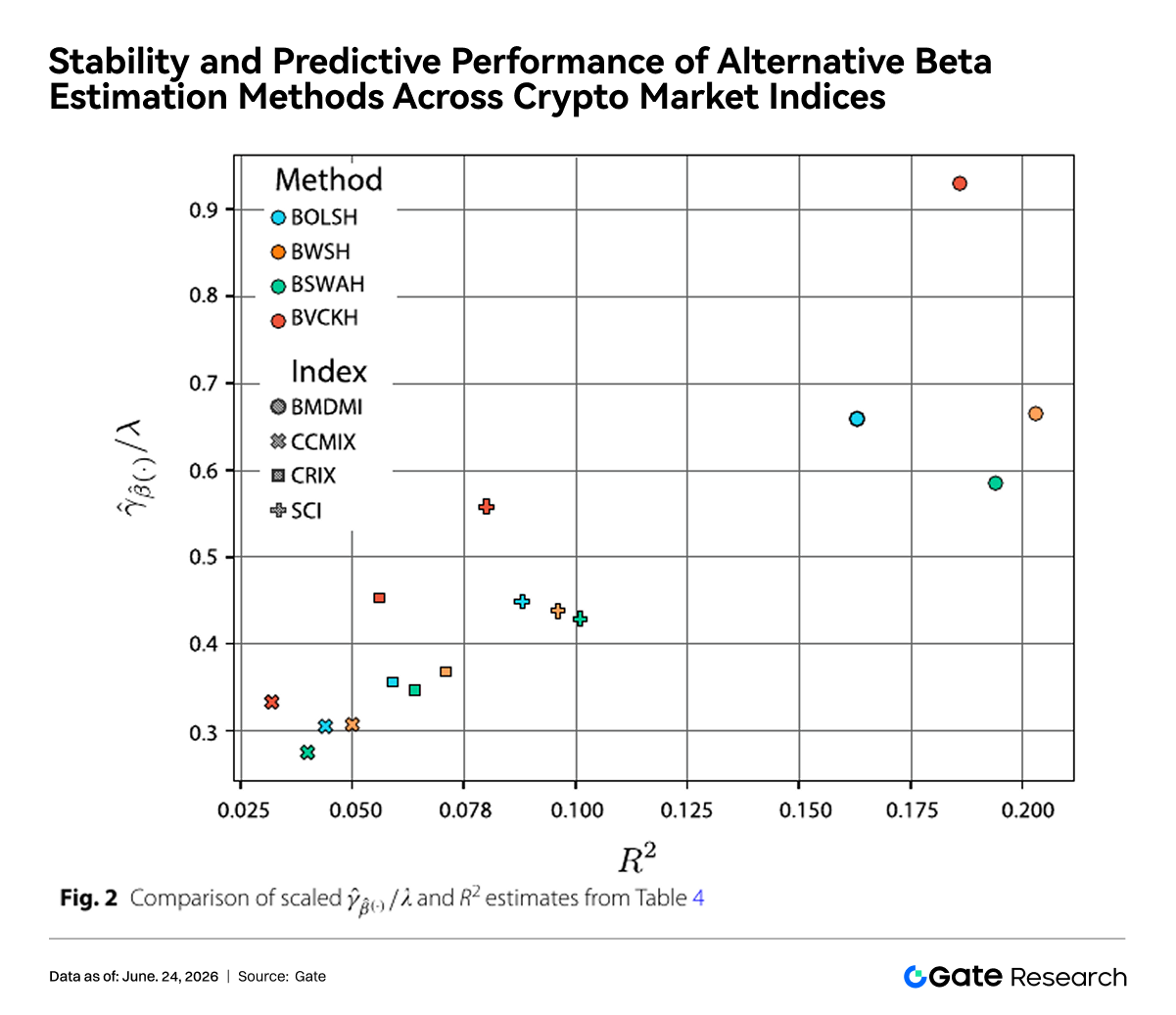

Using a sample of 515 crypto assets, Sila compares multiple Beta estimation methods and tests the predictability of one-year-ahead Beta under multiple crypto market indices. The study finds that the explanatory power of historical Beta for future Beta is far lower than in the U.S. equity market. Standard OLS performs weakly, while slope shrinkage and Vasicek shrinkage bring some improvement, but cannot fundamentally change the fact of “weak predictability.”

This conclusion echoes the evidence of market jumps in high-frequency research. Saef’s study points out that high-frequency jumps in the digital asset market cluster around black swan events, and these jumps significantly affect the direction and magnitude of daily returns. In other words, crypto asset returns are not just about “the market moving slowly,” but frequently face discrete shocks. As long as the return-generating mechanism itself is highly jump-driven, any Beta estimated from smoothed historical covariance relationships will be more prone to distortion.

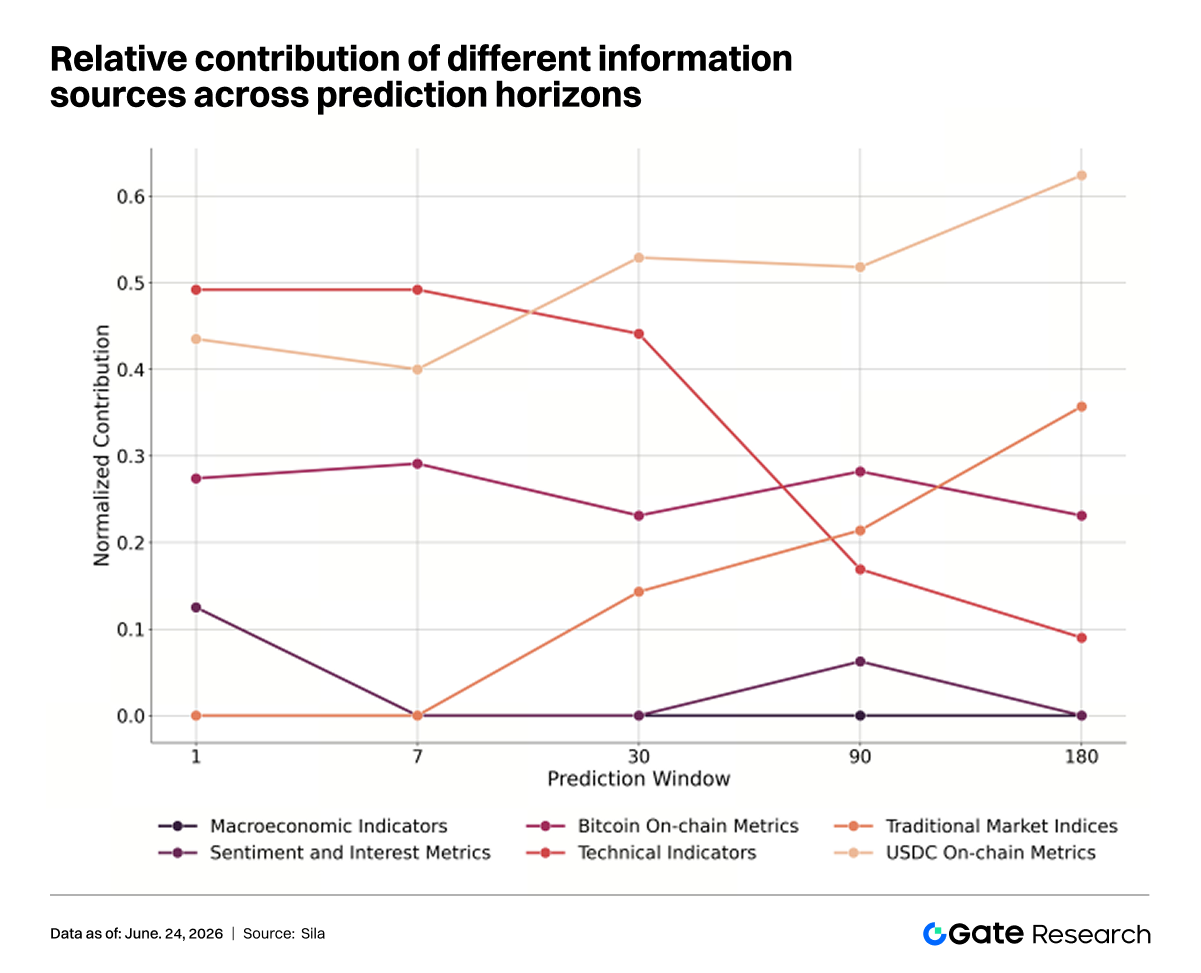

Going one step further, Demosthenous provides another important piece of evidence from the perspective of predictive modeling: when a model simultaneously introduces on-chain indicators, sentiment data, traditional market indices, and macro variables, predictive performance is significantly better than frameworks relying only on a single data source. This means that the drivers affecting the crypto market are inherently multi-source, and if a single Beta attempts to carry too much explanatory burden, it will inevitably face structural insufficiency.

In theory, failure in Beta prediction usually comes from three kinds of reasons: measurement error, factor definition bias, and instability in the relationship itself. In the crypto market, these three problems almost exist at the same time.

Against this background, improving estimators does help. For example, shrinkage methods can reduce the impact of extreme values, and Bayesian shrinkage can reduce cross-sectional noise. But these methods improve problems at the measurement level, not the market structure itself. As long as the driving factors of asset returns are rearranged across different time periods, the predictive accuracy of Beta will be difficult to fully recover through local technical fixes.

The figure above compares the performance of different crypto market indices (BMDMI, SCI, CRIX, CCMIX) and different Beta estimation methods in terms of Beta stability and future predictive ability. Overall, results corresponding to BMDMI are distributed more in regions of higher stability and higher predictability, while the traditional BOLSH estimation method performs relatively weakly overall. The research results show that both the way a market index is constructed and the method used to estimate Beta affect predictive performance, but even when better indices and more robust estimators are adopted, the magnitude of improvement remains limited. This further indicates that the difficulty of predicting Beta in the crypto market does not simply stem from statistical estimation error, but more reflects structural characteristics such as fragmented market structure, diversification of risk factors, and dynamic changes in return relationships.

4. Hedging Limits

If Beta is difficult to predict stably, then the most direct practical question is: is it still worthwhile to use it for hedging? From a trading perspective, the logic of market Beta hedging is very clear: while holding a long position in a given asset, establish a short position in a market index or market proxy to compress systematic volatility as much as possible, leaving only relative value or individual alpha.

But the reality of the crypto market is much more complex than this framework. First, many assets do not have sufficiently stable market linkage, so hedging may not significantly reduce variance. Second, whether different indices can represent “true market risk” itself varies. Third, a large part of asset returns may come from idiosyncratic risk, liquidity risk, or narrative risk, and these components do not automatically disappear simply because the market index is shorted.

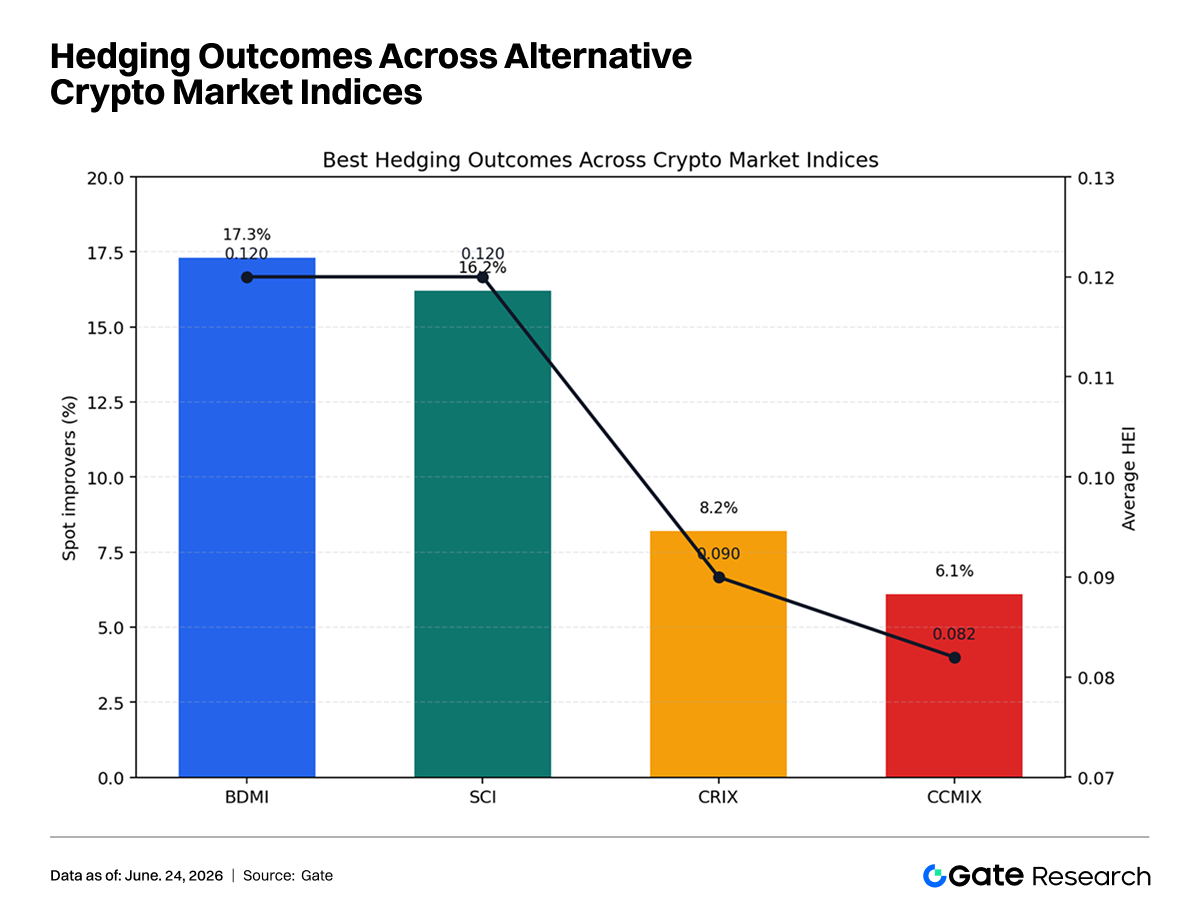

The gap in hedging effectiveness across different indices is very large. Under BMDMI and SCI, the proportions of assets that can significantly outperform simply holding spot are about 17.3% and 16.2%, respectively, while under CRIX and CCMIX, this proportion falls to 8.2% and 6.1%. This shows that “which index is chosen to represent market risk” is not a marginal issue, but a core prerequisite determining whether hedging is usable.

Looking further, even under the better-performing index frameworks, the proportion of assets that can truly achieve statistically superior risk compression remains low. This means that the applicability of market Beta hedging in the crypto market is limited. It is more like a “selectively effective” tool than a universally replicable general solution.

5. Multi-Factor Reassessment

Putting the above research conclusions back into industry practice yields implications at three levels.

-

For quantitative teams: Beta should no longer be treated as a default stable base input, but as a state variable that needs rolling validation. When building neutral strategies, sector rotation models, or style exposure monitoring, researchers should simultaneously track changes in index definition, liquidity conditions, and market event windows, rather than relying only on a fixed historical window regression to produce a long-term valid Beta.

-

For trading platforms: if a platform wants to launch more mature risk control and strategy tools, the focus should not only be on providing a “broad market index,” but on building multi-layer market profiling capability. For example, the platform can simultaneously provide a price market index, a liquidity market index, an on-chain activity index, a stablecoin funding index, and a sentiment heat index, allowing strategy researchers to choose corresponding factors according to different problems, rather than being forced to compress everything into a single market Beta.

-

For institutional investors: if institutions continue to use the traditional market hedging framework of “index short + asset long,” they need to reassess which assets truly have hedgeability. Large-cap assets and highly liquid sectors are more likely to be explained by market factors, while long-tail assets are more likely to exhibit a return structure dominated by individual events. For such assets, applying Beta hedging may only increase transaction costs without significantly reducing net risk.

6. Conclusion

Taken together, existing public research shows that Beta in the crypto market has not lost its meaning, but it is far less stable, universal, and replicable than in traditional finance. The lack of a unified definition of market indices, frequent return jumps, obvious liquidity stratification, and the persistent disturbance of on-chain and narrative factors jointly weaken the explanatory power of historical Beta for future Beta, and also limit the applicability of market-Beta-based hedging strategies across the whole market.

For researchers and institutions, this reality means two directions must advance simultaneously: one is to continue improving the robustness of Beta estimation methods, and the other, more importantly, is to rebuild the market factor system for digital assets. The truly competitive risk management framework of the future is likely not “a more precise single Beta,” but a multi-factor model that can unify price, liquidity, on-chain behavior, sentiment, and the macro environment into the same risk language.

Reference:

Gate Research is a comprehensive blockchain and cryptocurrency research platform that provides deep content for readers, including technical analysis, market insights, industry research, trend forecasting, and macroeconomic policy analysis.

Disclaimer

Investing in cryptocurrency markets involves high risk. Users are advised to conduct their own research and fully understand the nature of the assets and products before making any investment decisions. Gate is not responsible for any losses or damages arising from such decisions.