DeFi is not a set of silos. It is an interconnected value stack. If the rails, liquidity, risk and security, or governance layers weaken, everything above them becomes fragile. Our DeFi Value Pyramid model maps this system. Download the full PDF here:

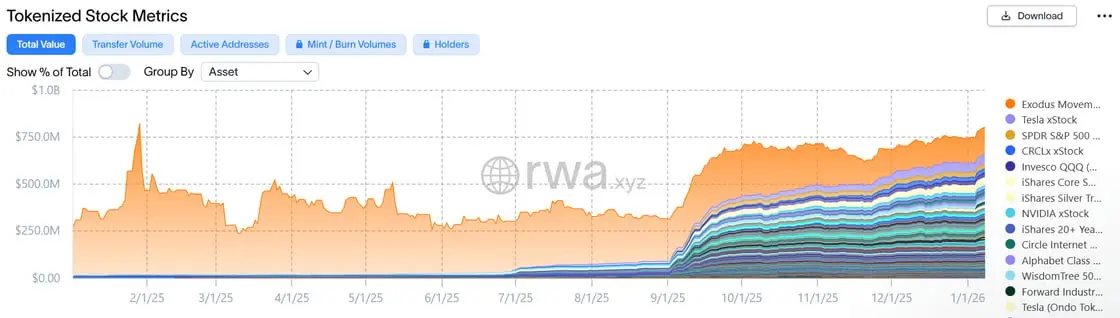

The tokenized equities sectors exhibits high concentration, with the top three providers, Ondo, Backed Finance, and Securitize, controlling over 90% of the total on-chain equity value.

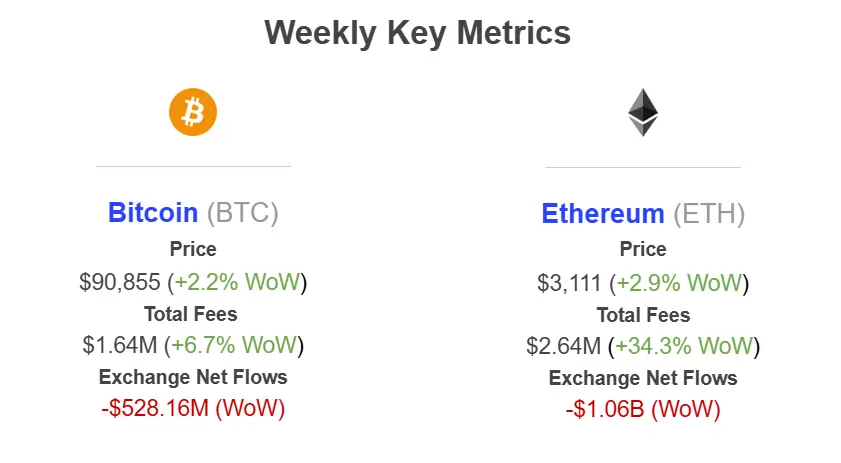

Ethereum saw a staggering -$1.06 billion in net outflows this week. This is one of the strongest accumulation signals in recent months. Combined with the 120% spike in the validator entry queue and record address growth, this data suggests that the "post-holiday" period is being used by major players to lock up ETH for staking and long-term positioning

Bringing stocks into DeFi could unlock a kind of access and utility retail investors simply haven’t had before. In this article, we take a closer look at what that means, along with the other key trends shaping the year ahead.

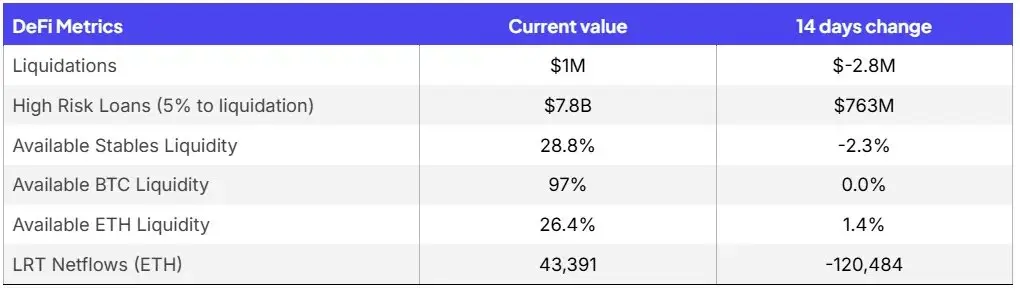

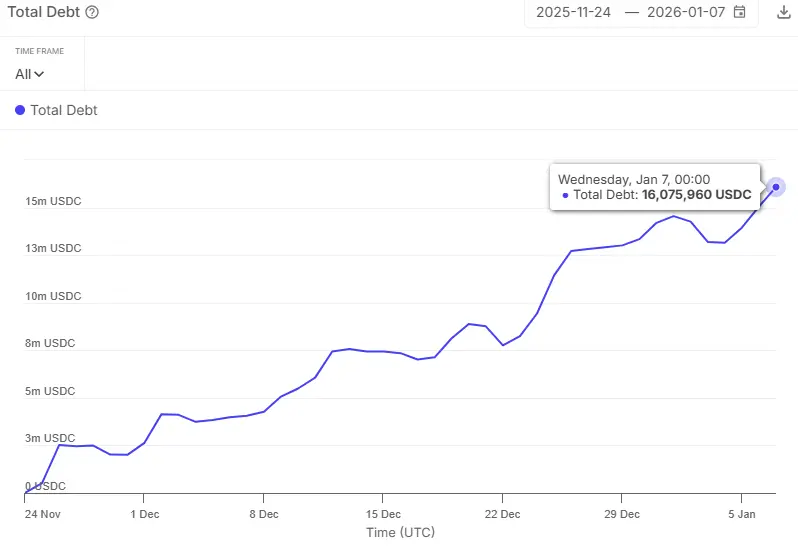

Here are some key risk metrics to consider ✔️ Liquidations fell further over the holiday period ✔️ Available liquidity remains high, with DeFi leverage still relatively muted Read more here:

Are exploits moving from smart contract exploits to other attack vectors? In this week's risk pulse, we analyze this shift and other key risk metrics to consider👇

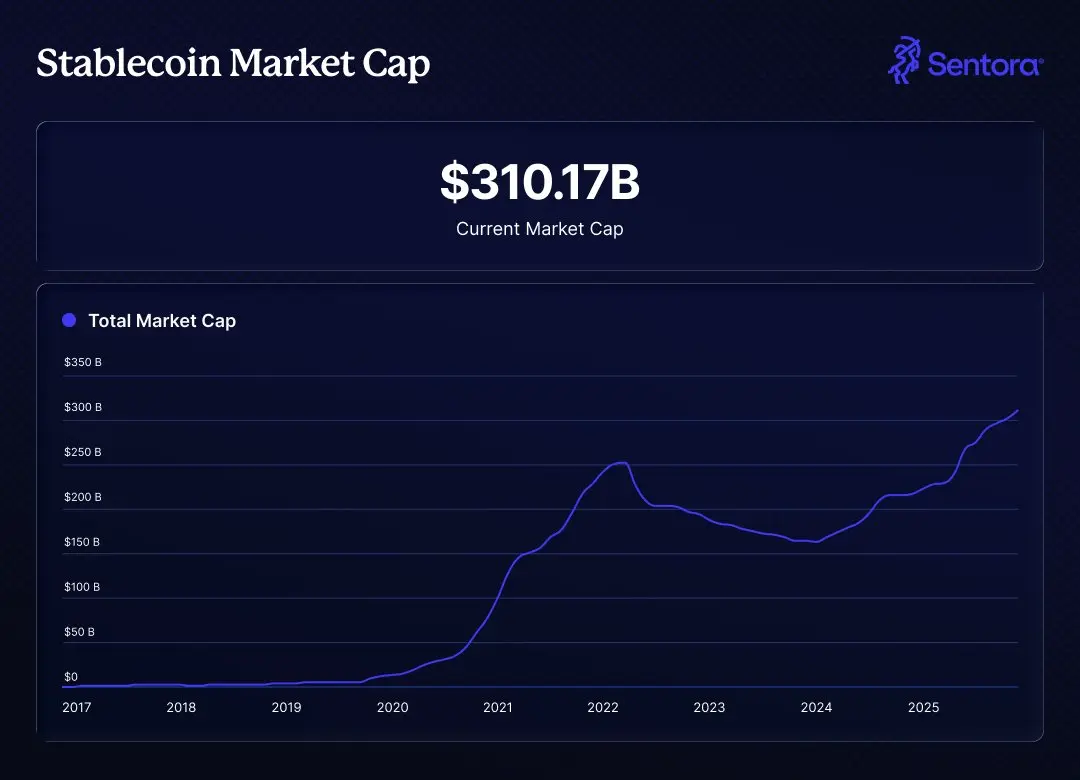

The stablecoin market saw steady, robust growth throughout 2025. That momentum is likely to carry into 2026, as neobanks roll out new stablecoin products for their retail customer bases.

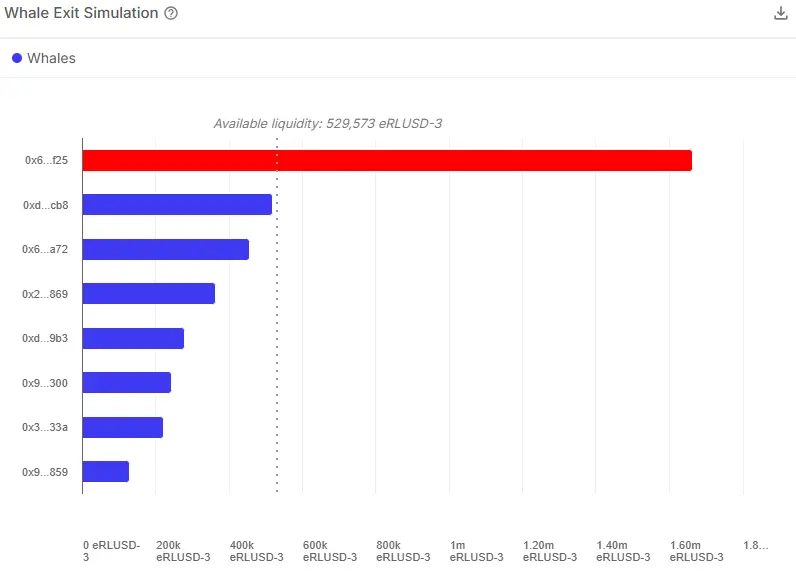

Our whale-exit simulation shows how major addresses could strain liquidity. In the image below, one whale can’t pull a big share of funds because of limited available liquidity. Review the data🔗

Audits are essential for DeFi, but not a guarantee. Audited projects saw $3.3B+ in losses between '20-'25, driven by rugs, private key compromises and post-audit changes. DeFi audits are the baseline, but effective risk management still requires active monitoring of risk