Lululemon released its first quarter fiscal year 2026 financial results on June 4 US after-hours, reporting a 38% decline in net profit to $195 million and lowering its full-year guidance. The Canadian athletic apparel company cited negative publicity affecting customer traffic over a 6-7 week period in late Q1 and early Q2, along with underperforming new product launches, as primary factors behind the guidance reduction. The earnings release follows the recent resolution of product quality controversies related to PFAS testing, which showed no detection of the substances in randomly sampled products.

Lululemon Reports Q1 FY2026 Financial Results

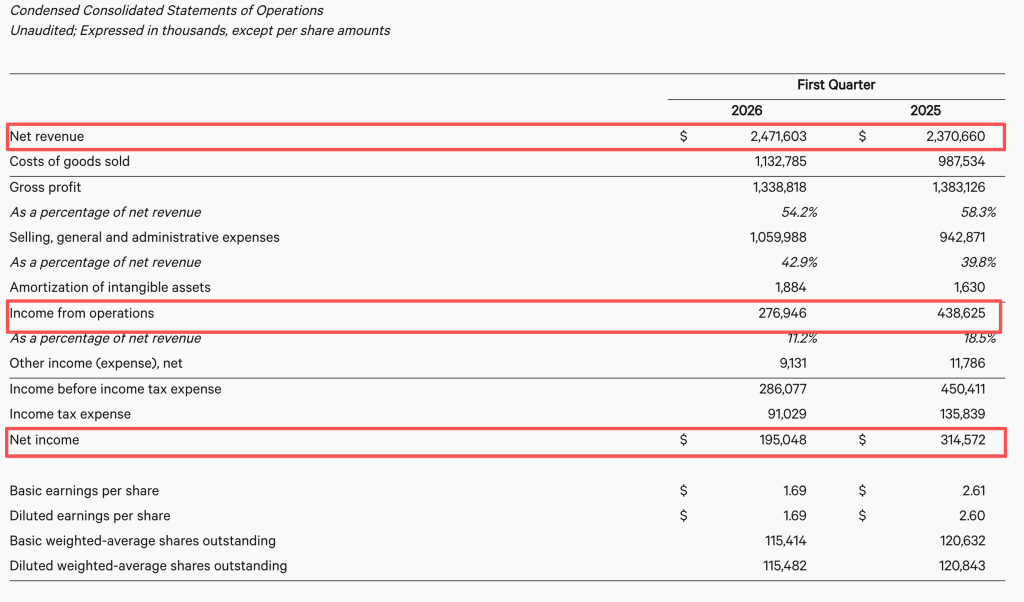

For the first quarter ended May 3, 2026, Lululemon reported net revenue of $2.472 billion, up 4.3% year-over-year. Operating profit decreased 37% to $277 million, with operating margin down 7.3 percentage points to 11.2%. Net profit fell 38% to $195 million. Gross margin declined 4.1 percentage points to 54.2%. Diluted earnings per share came in at $1.69, down 35% year-over-year.

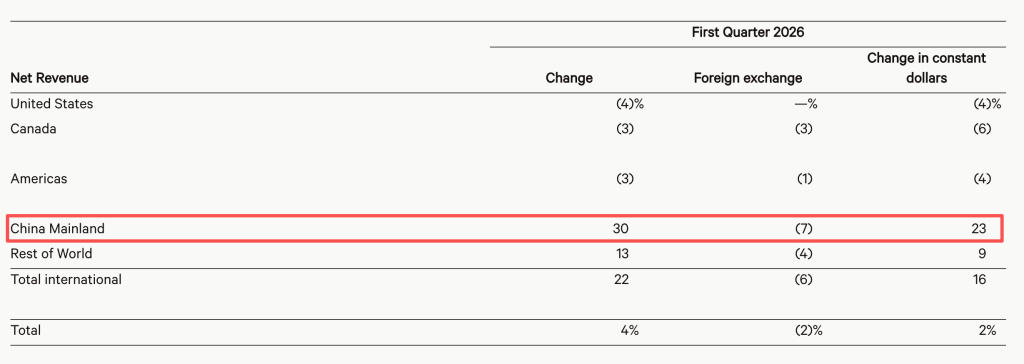

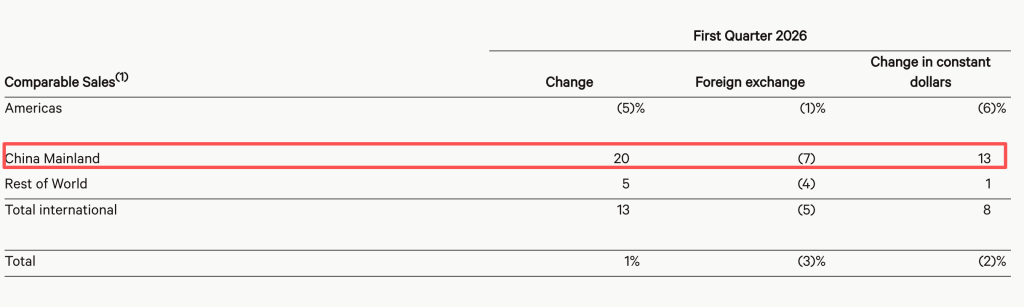

By region, Americas net revenue decreased 3% in Q1, while international markets grew 22%. Comparable store sales increased 1% overall, or declined 2% on a constant currency basis. Americas comparable store sales fell 5%, while international markets rose 13%.

Stock Declines Nearly 13% in Premarket Trading

Lululemon shares closed at $124.92 on June 4, down 0.88%. The stock has declined nearly 40% year-to-date. In premarket trading on June 5, shares fell nearly 13%.

Management Addresses Publicity Impact on Customer Traffic

During the earnings call, management stated that the overall athletic apparel market remained stable, but the company experienced significant customer traffic declines and lower conversion rates over the past 6-7 weeks. Management attributed this to concentrated negative publicity in late Q1 and early Q2, including a proxy battle and April controversies related to product material quality. The issues primarily affected the company's two major markets, North America and China. Management stated the publicity "has now subsided, but we have not yet seen a trend of recovery to previous levels."

Management also noted that some new product launches underperformed expectations, prompting targeted operational improvements. These two factors collectively dragged down current performance and formed the core reasons for lowering guidance.

Regarding the PFAS controversy, management referenced testing conducted in April. On April 22, Lululemon China confirmed that the company randomly sampled products from stores and warehouses and tested them for per- and polyfluoroalkyl substances (PFAS) using national standards. Test results showed PFAS substances were not detected.

Lululemon Lowers Full-Year and Q2 Guidance

For the second quarter of fiscal 2026, Lululemon expects net revenue between $2.45 billion and $2.475 billion, representing a decline of 3% to 2% year-over-year. Diluted earnings per share are expected between $1.76 and $1.81, assuming a tax rate of approximately 30%.

For the full fiscal year 2026, the company expects net revenue between $11 billion and $11.15 billion, representing flat to down 1% year-over-year. Diluted earnings per share are expected between $10.95 and $11.15. Full-year gross margin is expected to decline 0.9 percentage points, and operating margin is expected to decline 3.8 percentage points year-over-year.

Previously, Lululemon had expected fiscal 2026 net revenue between $11.35 billion and $11.5 billion (up approximately 2% to 4%) and full-year diluted earnings per share between $12.1 and $12.3.

Management stated on the call that the company has two priorities this year: stabilizing the North American business base and continuing to grow global engines. Full-price product sales remain the core goal for North America for the full year. Management noted that a recent yoga-themed marketing campaign did not meet revenue expectations. However, the company has ample new product inventory, with multiple summer items launching in Q2 across running, tennis, golf, and casual lifestyle categories. Throughout the year, the company will continue to introduce innovative fabrics in outerwear and loungewear categories.

China Mainland Revenue Grows 30% in Q1

In the first quarter of fiscal 2026, China mainland net revenue reached $478.4 million, up 30% year-over-year, leading growth rates. Revenue contribution increased to 19% from 16% in the prior-year period. China mainland comparable store sales rose 20%.

Management told analysts on the call that Q1 China mainland's 30% revenue growth included an 8 percentage point benefit from Lunar New Year timing shifts, with the remainder representing organic growth. China mainland gross margin continues to improve steadily, and the brand will continue to increase local investment.

Management further stated that China started the year strong, but momentum slowed in late Q1 as negative publicity surged. However, this situation has now subsided. The team continues to enhance brand awareness and differentiation, and the China market remains vibrant. Management stated that from an operating margin perspective, China still has healthy growth potential, and the company will continue investing in this business to drive long-term growth.

China maintains its previous guidance. Management stated on the call that the company expects China mainland sales to achieve mid-to-high double-digit growth in the second quarter and maintains its full-year growth expectation of approximately 20%.

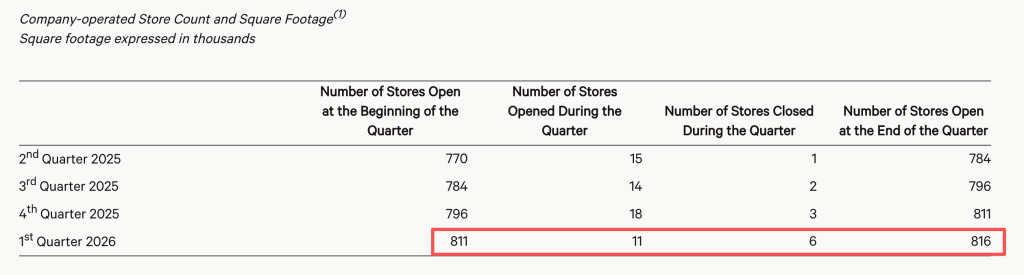

Company Plans 40-45 New Store Openings in FY2026

Lululemon added a net 5 company-operated stores in the first quarter, bringing the total to 816 stores.

Regarding future store expansion, management maintained its previous plan, stating on the call that in fiscal 2026, the company plans to open 40 to 45 new company-operated stores globally and optimize approximately 35 stores. This is expected to drive low double-digit growth in total square footage. New store plans include approximately 10 to 15 in North America (with approximately 8 in Mexico) and approximately 25 to 30 internationally, with the majority in China.

FAQ

What did Lululemon report for Q1 fiscal 2026?

Lululemon reported Q1 fiscal 2026 net revenue of $2.472 billion (up 4.3%), net profit of $195 million (down 38%), and diluted earnings per share of $1.69 (down 35%) for the quarter ended May 3, 2026.

Why did Lululemon lower its full-year guidance?

Management cited two primary factors: negative publicity affecting customer traffic over 6-7 weeks in late Q1 and early Q2, and underperforming new product launches. The company now expects fiscal 2026 revenue of $11-11.15 billion (flat to down 1%) and diluted EPS of $10.95-11.15.

How did Lululemon's China business perform in Q1?

China mainland net revenue grew 30% year-over-year to $478.4 million in Q1, with comparable store sales up 20%. Management maintains the full-year China growth expectation of approximately 20%.