The AI narrative behind the $26.5 billion raised

Key data on SK hynix’s Nasdaq IPO

SK hynix’s ADR offering received more than seven times oversubscription, with total order value nearing $200 billion. Top long-term institutions such as Baillie Gifford and Coatue Management submitted aggregate subscription intentions totaling up to $7 billion. Against the backdrop of a recent visible pullback in the global semiconductor sector—SK hynix’s Seoul share price has fallen about 25% from its late-June record high—such strong demand signals are noteworthy.

Investors’ logic is not complicated. The entire proceeds from this fundraising will be used for expansion of Korea’s domestic semiconductor capacity: construction of the first-phase wafer fab at the Yongin Semiconductor cluster; construction of the Chungcheong P&T 7 advanced packaging wafer fab; and procurement of advanced equipment such as EUV lithography machines from ASML in the Netherlands. In other words, U.S. capital markets are directly financing a Korean company’s capacity expansion—based on the premise that market participants believe AI-driven demand for memory chips will stay above supply for the long term.

SK hynix’s entire 2026 HBM and full-series storage-chip capacity has already been booked out by customers. This is not a one-off case for a single company, but a common industry situation. The three major memory manufacturers have sold out all their 2026 HBM capacity.

HBM: a “high-speed feed” on the AI compute supply chain

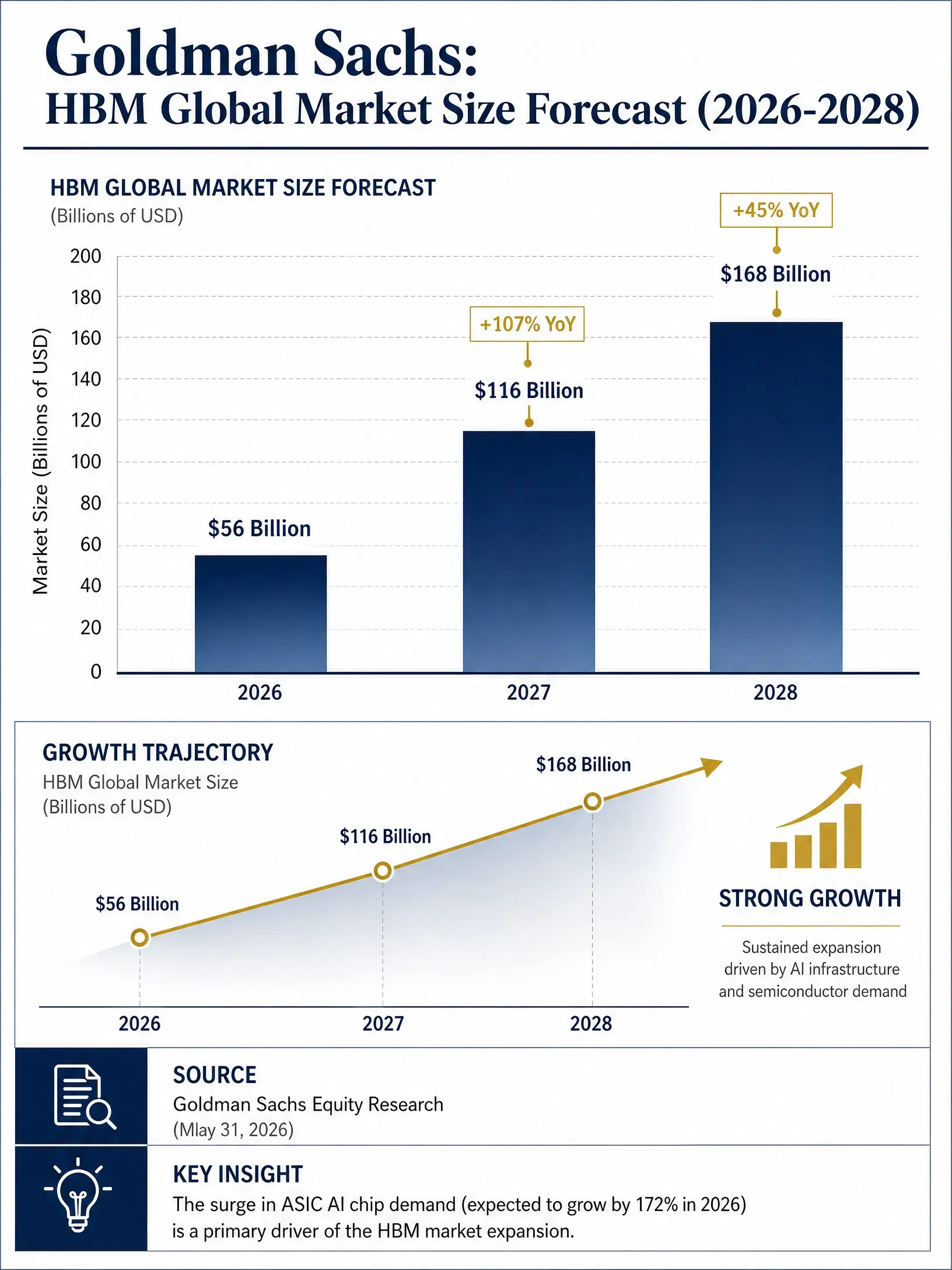

Goldman Sachs forecast of the global HBM market size (2026-2028)

To understand why SK hynix occupies such a critical position in this AI wave, it’s first necessary to understand HBM’s role in AI computing.

In traditional computing architectures, GPUs handle computation while DRAM handles storage, and the two are connected via a bus. As AI model parameter sizes move from the tens-of-billions range into the trillion range, GPU compute capacity is improving far faster than data transmission speed. Even with stronger compute, if data supply can’t keep up, the whole system can’t operate efficiently. HBM is precisely designed to solve this bottleneck. By using 3D stacking technology to vertically stack multiple DRAM chips and pairing it with silicon interconnect technology (TSV), it delivers extremely high bandwidth, very low latency, and excellent power efficiency within a tiny physical space.

Simply put, HBM is the “high-speed feed belt” for AI GPUs—without it, Nvidia’s H100, B200, and even the next-generation Rubin platform AI accelerators can’t perform as expected. It’s this system-level importance—“you can’t do without it”—that has elevated HBM from a DRAM niche category to the core strategic input for AI infrastructure.

Market size changes directly reflect this logic. Goldman Sachs predicts the total global HBM market will reach about $56 billion in 2026, double to $116 billion in 2027, and further expand to $168 billion in 2028. Meanwhile, the total global memory-chip market in 2026 is expected to surge from $247.5 billion in 2025 to more than $496.5 billion. HBM isn’t just the fastest-growing sub-segment; it’s also the core engine driving expansion across the entire memory industry.

Why SK hynix has become the biggest beneficiary

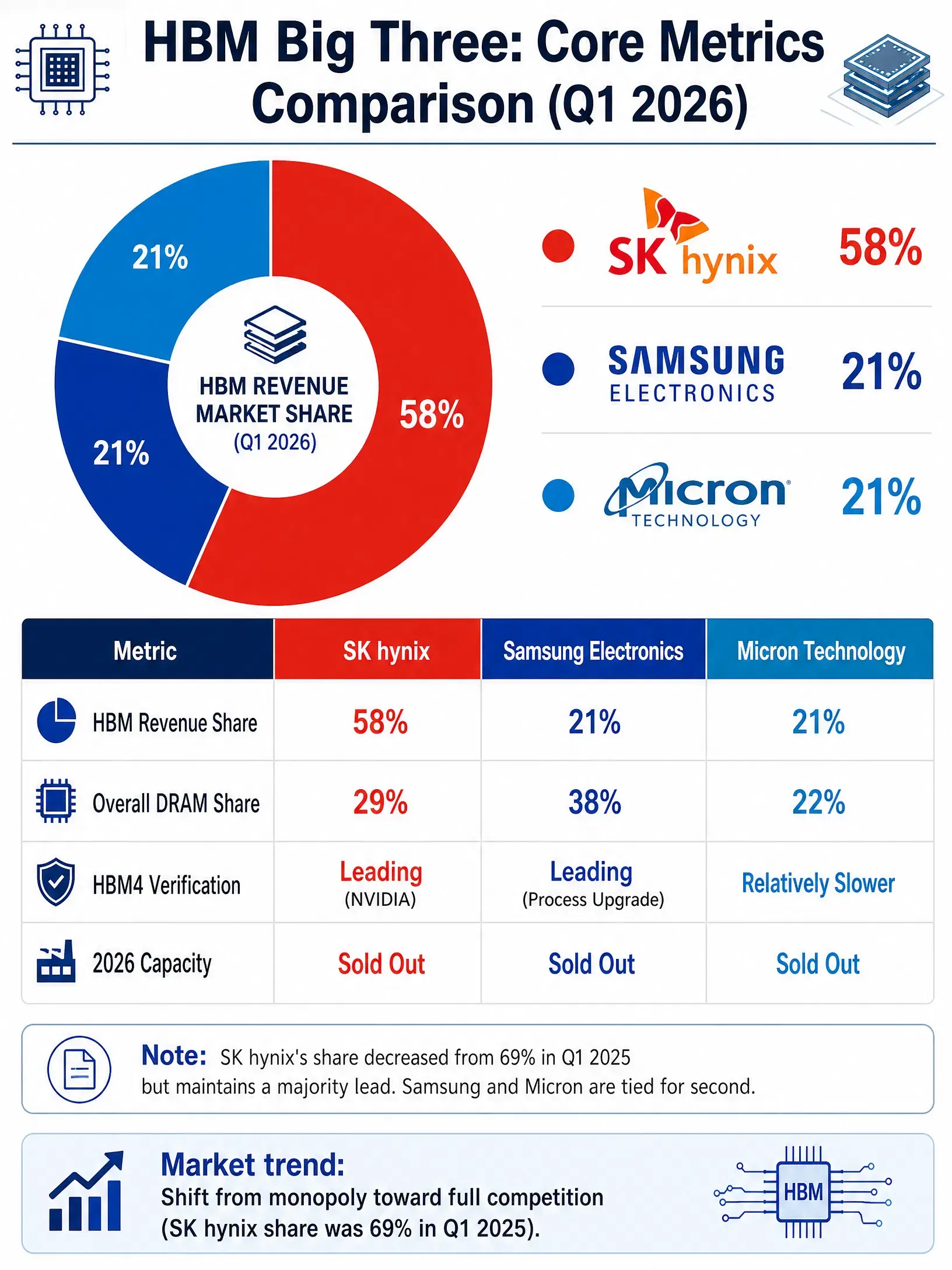

2026 Q1 global HBM market revenue share (comparison of three major players)

In the highly concentrated HBM market, only three companies globally can mass-produce: SK hynix, Samsung Electronics, and Micron Technology. Thanks to its first-mover advantage and technological accumulation, SK hynix holds a clear lead in this arena.

According to data released by Counterpoint Research on June 25, 2026, the revenue-share distribution of the global HBM market in Q1 2026 is: SK hynix 58%, Samsung Electronics 21%, and Micron Technology 21%. If measured by shipment volume, company research forecasts SK hynix’s full-year 2026 market share at about 52%, Samsung around 39%, and Micron around 8%. Although figures differ under different statistical approaches, SK hynix’s leading position is clear.

This lead is built on multiple layers of barriers. On the technology front, SK hynix’s MR-MUF packaging yield is considered an industry benchmark—the only vendor viewed as able to run both HBM3E and HBM4 production lines stably at the same time. On the customer-relationship front, SK hynix is Nvidia’s most important HBM supplier, holding roughly 60% to 70% share in HBM4 supply for the Vera Rubin platform. On the capacity front, SK hynix’s 2026 HBM capacity has essentially been booked out by customers.

On the eve of SK hynix’s listing, UBS published a research report raising its 12-month target price from 3.0 million Korean won to 3.2 million Korean won, reiterating a “Buy” rating, and expecting operating profit in 2026 to reach 32.7 trillion Korean won, with 2027 further rising to 62.3 trillion Korean won. Meanwhile, J.P. Morgan International (Jiao Yang International) forecast SK hynix’s revenue for 2026 to 2028 at 37 trillion, 57.8 trillion, and 65.5 trillion Korean won, respectively.

The competitive landscape among the three HBM giants

HBM’s competition is evolving from “single dominance” toward a “three-horse race.” In Q1 2025, SK hynix’s HBM market share had been as high as 69%. As Samsung and Micron rapidly ramped up capacity, SK hynix’s share declined somewhat—but this wasn’t a loss of orders; it’s an inevitable stage as the market moves from a near-monopoly toward full competition.

Samsung’s catching-up effort is the most evident. As the leader in the global DRAM market with a 38% share, Samsung is already ahead in HBM4 validation progress. Its process upgrades addressed heat issues and improved efficiency. Samsung plans to increase HBM capacity by 50% in 2026, targeting 250,000 wafers per month. In Q2 2026, Samsung Electronics’ operating profit surged about 19 times year over year, expected to reach 89.4 trillion Korean won (about $58.4 billion), making it the company with the highest quarterly operating profit globally.

Micron Technology, meanwhile, has secured a foothold thanks to advantages in the U.S. domestic market and its technological accumulation. Micron’s net profit for fiscal year 2026 is expected to be about $83 billion, with an operating margin as high as 80%. In early July, Micron announced spending $9.3 billion to expand HBM capacity in Hiroshima, Japan. However, limited by its technical architecture, Micron’s progress in HBM4 validation is relatively slower.

As the single largest buyer of HBM, Nvidia’s procurement strategy directly determines the share ceiling for the three suppliers. For supply-chain security reasons, Nvidia adopts a strategy of having three suppliers coexist. This means SK hynix’s leading position remains solid in the near term, but Samsung’s momentum can’t be ignored.

Can the memory supercycle continue?

Any analysis of the semiconductor industry can’t avoid the issue of cycles. The memory-chip industry is known for strong cyclicality—prices typically rise for a few years, then fall into a downturn of similar duration. Will this AI-driven expansion repeat history?

The optimistic chain of logic is clear. Global AI data center construction is still accelerating. Bank of America predicts that by 2027, global capital expenditures for cloud computing and AI infrastructure will reach $1.5 trillion. Goldman Sachs believes that the AI compute arms race dominated by cloud giants is shifting memory chips from being cyclical products to scarce strategic assets, and that price increases in 2026 are not the end of the story, but may be the early stage of a supercycle. A report from TrendForce (C&K Consulting) also points out that in the first half of 2026, the global memory-chip industry is in a once-in-15-years super boom cycle.

But risks are also real. The three major memory makers plan to release large-scale HBM and DRAM capacity between 2027 and 2028. If capacity is released concentratedly while the growth rate of AI investment slows, supply-demand dynamics could reverse. In addition, memory-chip prices have risen sharply for multiple consecutive quarters—general DRAM prices more than doubled within half a year—so the magnitude of the increase itself contains pressure for mean reversion.

In its commentary on SK hynix’s IPO, The Wall Street Journal noted that the market’s lower valuation for memory-related stocks is reasonable—because the memory industry experiences cyclical swings. SK hynix’s forward P/E ratio is about 7x, Samsung only about 2x, and Micron about 6x. These numbers are far below valuation levels for AI chip-design companies like Nvidia, reflecting the market’s heightened caution about cyclicality continuing.

UBS and KB Securities hold different views. KB Securities analysts believe SK hynix will benefit from expected memory-chip supply shortages lasting through the end of 2028, and that the uptrend in profitability and the stock price is far from over. UBS characterizes the current cycle as a “super memory cycle once every 30 years.”

Both views have their own rationale. Ultimately, the answer depends on one core variable: whether AI infrastructure investment can maintain its current growth slope over the coming years. For investors, that’s both an opportunity and a risk that must be continuously monitored.

FAQ

What are the fund-raising size and pricing for SK hynix’s Nasdaq IPO?

SK hynix priced its offering at $149 per ADR and issued 177.9 million ADRs, raising about $26.5 billion in total—setting the highest record for a foreign company’s IPO in the U.S. Each ADR corresponds to one-tenth of a share of Korean ordinary stock, and the issue price was at a premium of about 3% versus the closing price on the previous trading day in Seoul. ADR trading began on July 10 on the Nasdaq Global Select Market in the United States under the temporary ticker “SKHYV,” and switched to the official code “SKHY” on July 13.

What is an HBM chip, and why is it so important for AI?

HBM (high-bandwidth memory) is a high-performance memory that vertically integrates multiple DRAM chips using 3D stacking technology. In AI computing, as GPU compute increases, it needs faster data transmission speeds to match it. The bandwidth, low latency, and high energy efficiency provided by HBM exactly meet this need. It is a key component of Nvidia AI accelerators and is viewed by institutions such as Goldman Sachs as a core strategic input in the AI compute supply chain.

What is SK hynix’s competitive position in the HBM market?

SK hynix is the leader in the global HBM market. Counterpoint data shows its market share in Q1 2026 is 58%, while Samsung Electronics and Micron each hold 21%. SK hynix is Nvidia’s most important HBM supplier and holds roughly 60% to 70% share in HBM4 supply for the Rubin platform. Its entire 2026 HBM capacity has been booked by customers.

Will the memory supercycle continue?

Optimistic factors include continued global AI data center construction, increased capital expenditures by cloud providers, and rapid growth in HBM demand. Goldman Sachs forecasts that the HBM market will grow from $56 billion in 2026 to $168 billion in 2028. But risks remain: the storage industry has strong cyclicality, and the three major manufacturers plan to release large-scale capacity between 2027 and 2028. If supply and demand invert, it could trigger price adjustments.

What does SK hynix’s Nasdaq listing mean for investors?

This listing expands global investors’ access channels and can help narrow the valuation gap between SK hynix and its U.S.-listed competitor Micron. UBS and KB Securities both assign “Buy” ratings, believing the AI-driven memory supercycle is still in an early stage. However, investors need to watch for cyclicality risks in the memory industry and changes in supply-demand dynamics that capacity expansion may bring.