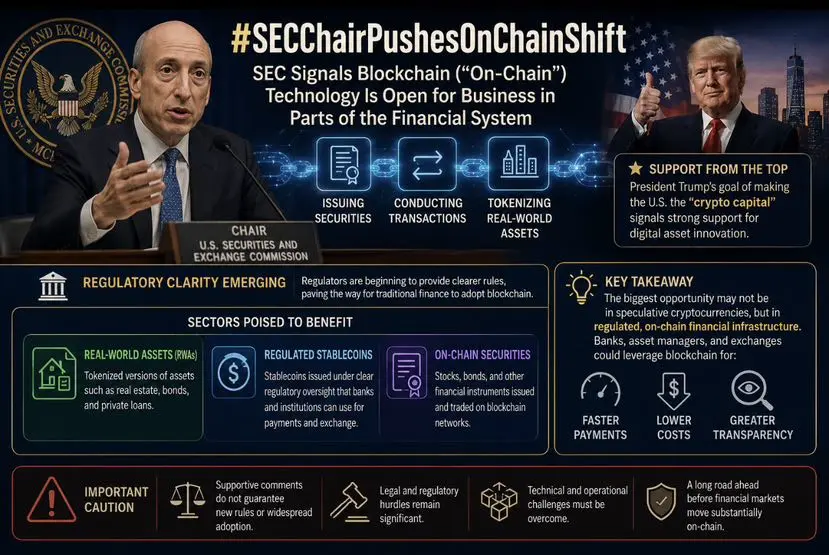

#SEC主席称将促进市场向链上转移 The "Project Crypto" proposed by SEC Chairman Paul Atkins and his vision of "markets moving on-chain" are centered on promoting the tokenization, on-chain trading, and compliance of traditional financial assets (RWA). Under this macro trend, the following sectors will become core beneficiaries:

1. Traditional Financial Asset Tokenization (RWA) Sector

This is the most direct and largest beneficiary sector of on-chain migration, mainly focusing on the on-chain reconstruction of traditional financial assets:

Tokenized Treasuries and Money Market Funds: As high-quality underlying assets for on-chain settlement, tokenized Treasuries (e.g., BlackRock's BUIDL) and on-chain money market funds are experiencing explosive growth due to their high liquidity, low barriers, and 24/7 trading advantages, serving as the "cash base" for on-chain finance.

Tokenized Stocks and ETFs: With the advancement of the SEC's "Innovation Exemption" rules, the compliance channels for third-party permissionless tokenized stocks (tracking U.S. stocks, etc.) and on-chain ETFs are being cleared, greatly benefiting related tokenization platforms (e.g., Ondo Finance) and compliant asset issuers.

Tokenized Repo Market: The on-chain migration of the repo market (with massive daily exposure) will significantly unlock collateral liquidity and reduce settlement risk, providing incremental space for related on-chain collateral and clearing protocols.

Other Traditional Assets: Tokenization of corporate bonds, ABS, private credit, and other assets, as well as publicly offered tokenization, will also see increased demand due to their ability to simplify multi-layered custody processes.

2. On-Chain Financial Infrastructure and Compliance Service Sector

Asset tokenization relies on underlying technical support and compliance assurance, highlighting the value of related infrastructure sectors:

On-Chain Clearing and Settlement (DVP) Infrastructure: On-chain clearing systems supporting delivery-versus-payment (T+0), compliant wallets (e.g., DTCC token pilot), and on-chain asset registration systems, which can significantly reduce settlement risk in traditional finance, will become essential for institutional on-boarding.

Compliance Bridging and Custody Services: Custodians, compliance platforms (e.g., compliant wallets, KYC/AML service providers), and compliance bridging projects that help traditional financial assets migrate securely and compliantly to the chain will gain substantial business opportunities by resolving compliance friction between traditional finance and the on-chain world.

On-Chain Financial "Super App": Platforms that integrate functions such as trading, clearing, custody, staking, and lending into a "super app" will become the gateway for next-generation financial traffic by providing one-stop on-chain financial services.

3. Underlying Public Chains and Payment Infrastructure (Stablecoin) Sector

Underlying Public Chains (L1/L2): The large-scale on-boarding of traditional financial assets will generate massive demand for highly scalable and secure underlying blockchains (e.g., Ethereum, Solana, and compliant L2s), directly benefiting public chains and their ecosystem infrastructure.

Compliant Stablecoins: As the payment infrastructure ("water, electricity, and gas") for on-chain asset transactions, compliant stablecoins (e.g., USDC, USDT, and stablecoins issued by compliant institutions) will see their underlying support value magnified as on-chain transaction volumes surge.

4. Decentralized Finance (DeFi) and On-Chain Derivatives Sector

On-Chain Lending and Derivatives: Tokenized assets (e.g., tokenized Treasuries) used as underlying collateral for on-chain lending protocols (e.g., Aave, Sky) or on-chain derivatives trading will greatly unlock the financial derivative value of assets, providing related DeFi protocols with abundant on-chain asset liquidity.

On-chain migration does not mean shifting to permissionless full decentralization, but rather an "institutional permissioned" and "compliant" on-chain transformation. Therefore, institutions and projects with compliance qualifications that can solve traditional financial pain points (e.g., settlement efficiency, collateral circulation) will hold an absolute advantage.

1. Traditional Financial Asset Tokenization (RWA) Sector

This is the most direct and largest beneficiary sector of on-chain migration, mainly focusing on the on-chain reconstruction of traditional financial assets:

Tokenized Treasuries and Money Market Funds: As high-quality underlying assets for on-chain settlement, tokenized Treasuries (e.g., BlackRock's BUIDL) and on-chain money market funds are experiencing explosive growth due to their high liquidity, low barriers, and 24/7 trading advantages, serving as the "cash base" for on-chain finance.

Tokenized Stocks and ETFs: With the advancement of the SEC's "Innovation Exemption" rules, the compliance channels for third-party permissionless tokenized stocks (tracking U.S. stocks, etc.) and on-chain ETFs are being cleared, greatly benefiting related tokenization platforms (e.g., Ondo Finance) and compliant asset issuers.

Tokenized Repo Market: The on-chain migration of the repo market (with massive daily exposure) will significantly unlock collateral liquidity and reduce settlement risk, providing incremental space for related on-chain collateral and clearing protocols.

Other Traditional Assets: Tokenization of corporate bonds, ABS, private credit, and other assets, as well as publicly offered tokenization, will also see increased demand due to their ability to simplify multi-layered custody processes.

2. On-Chain Financial Infrastructure and Compliance Service Sector

Asset tokenization relies on underlying technical support and compliance assurance, highlighting the value of related infrastructure sectors:

On-Chain Clearing and Settlement (DVP) Infrastructure: On-chain clearing systems supporting delivery-versus-payment (T+0), compliant wallets (e.g., DTCC token pilot), and on-chain asset registration systems, which can significantly reduce settlement risk in traditional finance, will become essential for institutional on-boarding.

Compliance Bridging and Custody Services: Custodians, compliance platforms (e.g., compliant wallets, KYC/AML service providers), and compliance bridging projects that help traditional financial assets migrate securely and compliantly to the chain will gain substantial business opportunities by resolving compliance friction between traditional finance and the on-chain world.

On-Chain Financial "Super App": Platforms that integrate functions such as trading, clearing, custody, staking, and lending into a "super app" will become the gateway for next-generation financial traffic by providing one-stop on-chain financial services.

3. Underlying Public Chains and Payment Infrastructure (Stablecoin) Sector

Underlying Public Chains (L1/L2): The large-scale on-boarding of traditional financial assets will generate massive demand for highly scalable and secure underlying blockchains (e.g., Ethereum, Solana, and compliant L2s), directly benefiting public chains and their ecosystem infrastructure.

Compliant Stablecoins: As the payment infrastructure ("water, electricity, and gas") for on-chain asset transactions, compliant stablecoins (e.g., USDC, USDT, and stablecoins issued by compliant institutions) will see their underlying support value magnified as on-chain transaction volumes surge.

4. Decentralized Finance (DeFi) and On-Chain Derivatives Sector

On-Chain Lending and Derivatives: Tokenized assets (e.g., tokenized Treasuries) used as underlying collateral for on-chain lending protocols (e.g., Aave, Sky) or on-chain derivatives trading will greatly unlock the financial derivative value of assets, providing related DeFi protocols with abundant on-chain asset liquidity.

On-chain migration does not mean shifting to permissionless full decentralization, but rather an "institutional permissioned" and "compliant" on-chain transformation. Therefore, institutions and projects with compliance qualifications that can solve traditional financial pain points (e.g., settlement efficiency, collateral circulation) will hold an absolute advantage.