In January 2009, Satoshi Nakamoto embedded a now-famous message in Bitcoin's genesis block:

"The Times 03/Jan/2009 Chancellor on brink of second bailout for banks."

The line served not only as a timestamp but also as a widely interpreted critique of the post-2008 banking bailout system. Bitcoin was designed to create a peer-to-peer value transfer network that would not rely on banks or trusted intermediaries.

Seventeen years later, however, one of the most common ways to gain Bitcoin exposure is by purchasing shares of a Bitcoin ETF issued by the world's largest asset manager, BlackRock, or by investing in publicly listed Bitcoin treasury companies.

Does this mean that crypto has drifted away from its original vision? Is Wall Street systematically taking control of crypto's issuance, pricing, custody, and distribution?

1. Is Wall Street Taking Over the Issuance, Pricing, Custody, and Distribution of Crypto Assets?

1.1 The Ideal: Bitcoin's Original Vision in 2009

To answer this question, we must return to Bitcoin's founding philosophy.

The Bitcoin white paper envisioned a financial system built around three forms of decentralization:

-

Decentralization. No central issuer, headquarters, or server that could be shut down. The ledger would be maintained collectively by a global network of nodes, with rules enforced through code.

-

Disintermediation. Value could move directly between participants without banks, brokers, or clearing houses. "Private key equals ownership" made self-custody the default model.

-

Bankless Finance. Anyone could hold and transfer assets—or participate in new issuance through mining—without opening a bank account, completing KYC procedures, or qualifying as an accredited investor.

At its core, Bitcoin sought to redistribute four fundamental powers of finance—issuance, pricing, custody, and distribution—from a small group of centralized institutions to every participant in the network.

This was both a direct response to the 2008 global financial crisis and a declaration of intent: if centralized financial institutions could fail, an alternative system should be built that no longer depended on them.

1.2 Reality: Are These Four Powers Being Reclaimed by Wall Street?

Following the approval of spot Bitcoin ETFs in 2024, that decentralized vision appears less absolute. Rather than replacing traditional finance, crypto technology is increasingly being incorporated into traditional financial institutions' issuance, settlement, and distribution infrastructure.

Asset management giants such as BlackRock, Fidelity Investments, and Franklin Templeton have transformed BTC and ETH into products that can be purchased through conventional brokerage accounts.

Once packaged as ETFs, Bitcoin and Ethereum cease to be purely on-chain assets requiring wallets and private keys; instead, they become familiar financial products accessible through traditional securities accounts.

As of May 2026, spot ETFs collectively held approximately 1.5 million BTC, representing roughly 7.14% of Bitcoin's maximum supply of 21 million coins within just two years.

A similar transformation has taken place in derivatives markets. Bitcoin and Ethereum futures and options listed on Chicago Mercantile Exchange provide institutional investors with regulated venues for trading, hedging, and portfolio risk management. Increasingly, institutions can gain crypto exposure without directly interacting with blockchain networks, instead using futures, options, ETFs, structured products, and fund shares.

The rise of real-world assets (RWA) and tokenized U.S. Treasuries has pushed this "Wall Street-ization" even further. The tokenized Treasury market expanded from approximately $380 million in early 2023 to more than $11 billion by 2026, making it the fastest-growing segment within the broader RWA sector. Notably, the list of issuers reads like a roster of Wall Street itself.

Products such as BlackRock's BUIDL, Franklin Templeton's Benji, JPMorgan Chase's Kinexys, and tokenized Treasury products from Ondo Finance are bringing traditional financial assets onto blockchain networks.

Meanwhile, institutions including Coinbase, Fidelity Investments through Fidelity Digital Assets, and BNY increasingly provide custody, trading, and compliance infrastructure.

In August 2025, a U.S. executive order further accelerated this convergence by allowing alternative assets—including cryptocurrencies and private equity—to be included in 401(k) retirement plans, opening access to approximately $12.5 trillion in retirement savings. As institutional participation expands, brokerages and wealth managers are steadily assuming greater control over crypto asset distribution. This evolution represents far more than a change in product packaging—it reflects a shift in financial power.

Today, asset managers oversee issuance, brokers and financial advisors handle distribution, regulated custodians safeguard assets, market makers and authorized participants manage ETF creation and redemption, exchanges provide listing venues, and regulatory frameworks define market boundaries. In this process, crypto assets are increasingly being translated into the language and infrastructure of traditional finance.

2. Two Paths Converging: Why 1 + 1 > 2

Wall Street's growing influence represents only one side of the story. Looking at the broader picture, the other side is that both traditional finance and crypto are increasingly compensating for each other's weaknesses. This is not a zero-sum game in which one system replaces the other, but rather a gradual convergence between two financial paradigms.

The crypto-native ecosystem offers permissionless access, 24/7 global markets, and programmable on-chain settlement. Yet it has consistently lacked four critical components: compliant issuance channels, institutional-grade custody, deep fiat liquidity, and distribution networks capable of reaching mainstream investors. Coincidentally, these are precisely the areas where Wall Street has long held overwhelming advantages.

Traditional finance, by contrast, possesses regulatory licenses, trusted custodians, trillion-dollar capital pools, and extensive global distribution channels. However, its assets remain constrained by an outdated infrastructure: markets operate only during business hours, cross-border investing remains cumbersome, settlement typically requires T+2, and financial products are largely siloed from one another. These limitations are exactly what blockchain-based financial infrastructure is naturally designed to overcome.

Consequently, the "1 + 1 > 2" relationship is no longer merely a theoretical proposition.

Over the past year, crypto exchanges have increasingly launched real equity trading services, while the broader industry has evolved along two seemingly opposite—but ultimately converging—paths. One begins with crypto exchanges and expands toward traditional finance; the other begins with traditional financial institutions and moves toward crypto. Gate and Robinhood represent the clearest examples of these two approaches.

2.1 Path A: From CEX to Traditional Finance

Gate's TradFi strategy can be viewed as progressing through four distinct stages.

2.1.1 Stage One: Tokenized Equities

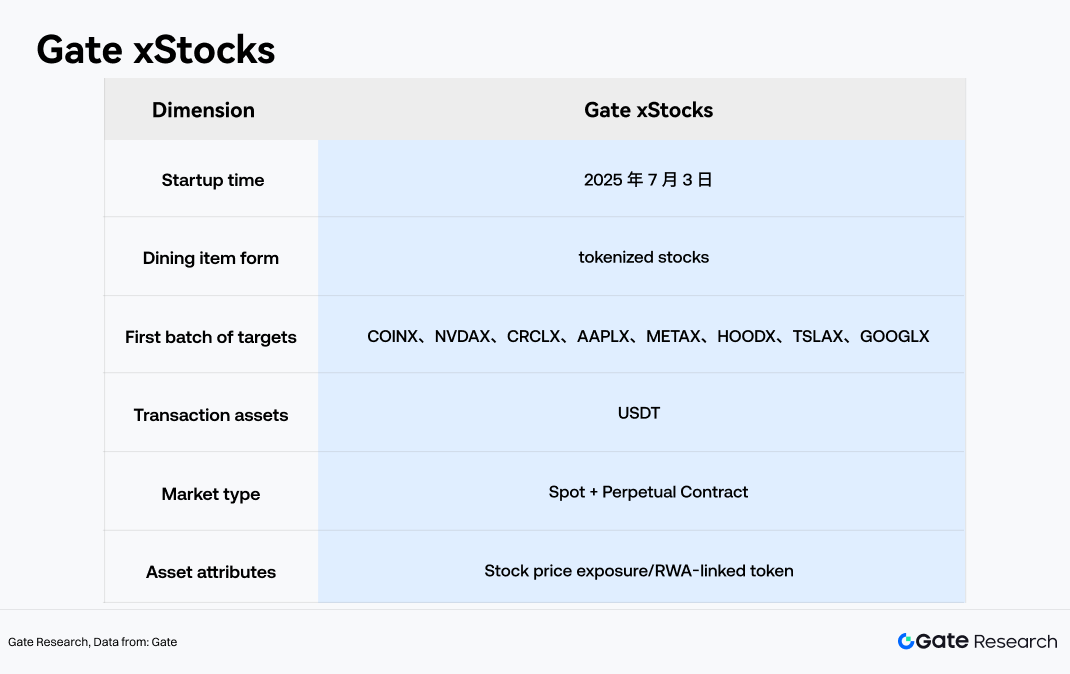

The first stage focused on tokenized equities. On July 3, 2025, Gate officially launched its xStocks Trading Section, becoming one of the earliest crypto exchanges to offer tokenized equity trading. Through partnerships with xStocks and Ondo, users were able to trade spot and perpetual contracts linked to U.S. equities—including Apple, Tesla, and Meta—directly using USDT, around the clock and without opening a traditional brokerage account.

The foundation of this model is the "third-party compliant issuance + CEX distribution" framework represented by xStocks.

Under this structure, the underlying shares are held on a one-to-one basis through special purpose vehicles (SPVs) established by the Swiss-regulated issuer Backed Finance under Switzerland's DLT regulatory framework. The corresponding shares are purchased through regulated brokers such as Interactive Brokers and held in custody by licensed institutions including InCore Bank. The resulting tokens are issued on Solana using the SPL token standard, while Chainlink price oracles and high-frequency synchronization with off-chain markets ensure pricing accuracy and market consistency.

2.1.2 Stage Two: CFDs on Traditional Assets

The second stage expanded into Contracts for Difference (CFDs), enabling users to gain price exposure to traditional assets—including gold, foreign exchange, equity indices, commodities, and selected stocks—without owning the underlying securities.

In January 2026, Gate broadened its TradFi CFD offering to cover precious metals, foreign exchange, indices, commodities, and popular equities. The platform also introduced USDx, an internal accounting unit pegged to USDT, to unify the trading experience.

At this stage, the exchange primarily functions as a provider of synthetic price exposure. Users trade derivatives rather than directly holding the underlying financial assets.

2.1.3 Stage Three: Real Equity Trading

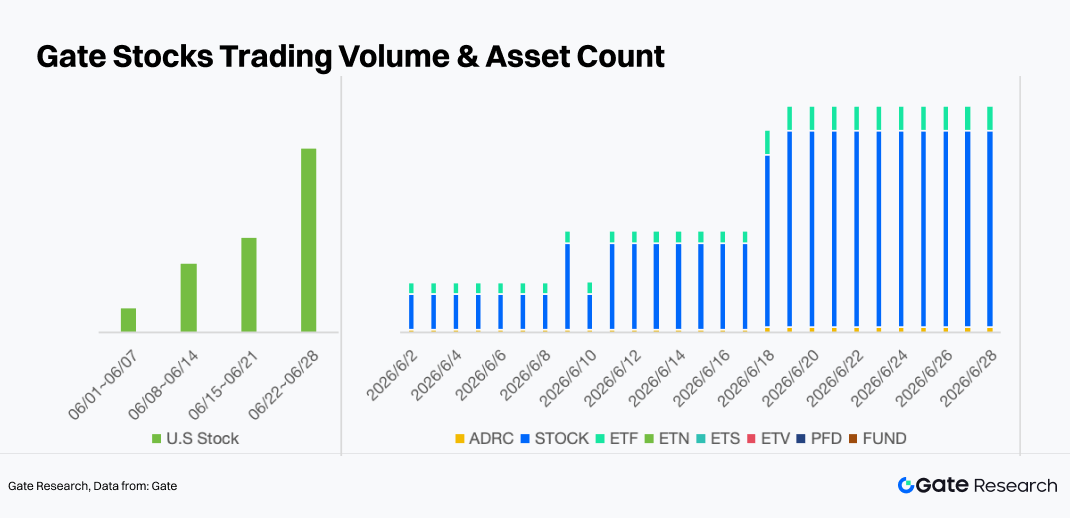

The third stage arrived in June 2026 with the launch of real stock trading.

On June 1, Gate officially introduced real equity trading, offering access to more than 10,000 U.S. stocks and ETFs listed across major exchanges including the NYSE and Nasdaq. Users can trade these securities directly using USDT.

This marked a significant strategic evolution. Rather than serving only crypto-native users through spot markets, derivatives, Launchpad offerings, copy trading, wallets, and on-chain tools, Gate began incorporating traditional financial assets—including equities, ETFs, bonds, foreign exchange, and investment funds—into its trading ecosystem.

Unlike the earlier CFD model, Gate emphasizes direct connectivity to regulated securities markets through licensed brokerage infrastructure, rather than relying on tokenized equities or synthetic assets.

On June 3, Gate further announced a strategic partnership with Alpaca to expand access to real stock trading for eligible users. Alpaca, an SEC-registered clearing broker, provides the underlying infrastructure for trade execution, clearing, and custody.

In other words, Gate is not issuing equities itself. Instead, it positions itself as the front-end gateway connecting crypto accounts, stablecoin liquidity, and the traditional brokerage and clearing ecosystem.

2.1.4 Stage Four: Geographic Expansion of Equity Markets

The fourth stage focuses on expanding access to global equity markets.

Following the launch of U.S. equities, Gate introduced Hong Kong stock trading on June 15, supporting more than 1,000 companies listed on the Hong Kong Stock Exchange. Users can trade leading companies—including Tencent, HSBC, Xiaomi, Meituan, BYD, and China Mobile—using USDT through the same unified stock account used for U.S. equities.

On June 22, Gate further expanded into South Korea by launching trading for equities listed on the Korea Exchange (KRX). The initial rollout covers the country's largest 1,000 listed companies, including Samsung Electronics, SK Hynix, NAVER, Hyundai Motor, and Celltrion, spanning both the KOSPI and KOSDAQ markets.

Within a single month, Gate completed a rapid expansion from U.S. equities to Hong Kong and South Korean markets, establishing a multi-market investment platform unified by USDT as the primary funding currency and global equities as the underlying investment universe.

These four stages illustrate how the growth strategy of centralized exchanges has evolved.

Historically, CEXs relied primarily on spot trading, derivatives, Launchpad products, wealth management services, and Web3 wallets to build their ecosystems. However, as crypto adoption matures, fee competition intensifies, and regulatory requirements become increasingly stringent, the growth potential of crypto-only trading continues to narrow.

Traditional assets—including equities, ETFs, and commodities—not only expand the range of tradable products but also improve user asset retention.

For Gate, real equity trading serves two strategic purposes: it satisfies crypto users' growing demand for cross-asset portfolio allocation while simultaneously attracting traditional financial investors into the Gate account ecosystem.

2.2 Path B: From Traditional Finance to Crypto

Moving in the opposite direction from Gate, a growing number of traditional brokerages—represented by Robinhood—are steadily expanding into the crypto market. Their greatest strengths lie in their established brokerage customer base, mature regulatory frameworks, and extensive experience in retail investment products. As a result, they are able to integrate traditional financial products such as stocks, ETFs, and options with crypto assets on a single trading platform at relatively low customer acquisition costs.

For these institutions, crypto is no longer simply an additional asset class within traditional wealth management. Instead, they are leveraging crypto's defining characteristics—including 24/7 trading, high volatility, and global market accessibility—to create new revenue streams and strengthen their competitive positioning.

Robinhood is perhaps the most representative example of this trend.

Originally launched as a retail brokerage and fintech platform, Robinhood built its business around stock trading, options, cash management, margin lending, and subscription services. Over the past several years, however, crypto has become one of its most important growth engines.

In the fourth quarter of 2024, Robinhood generated $358 million in crypto trading revenue, representing year-over-year growth of more than 700%, while total transaction-based revenue increased by more than 200%. By the end of 2025, Robinhood's annual revenue had reached $4.5 billion, annual net deposits totaled $68 billion, and its Robinhood Gold subscription service had surpassed 4.2 million members. These figures demonstrate that Robinhood has evolved from a stock trading application into a comprehensive financial account platform.

Robinhood's crypto strategy extends far beyond simply listing cryptocurrencies. In June 2025, Robinhood completed its acquisition of Bitstamp, bringing Bitstamp's retail and institutional crypto businesses across Europe, the United Kingdom, the United States, and Asia into the Robinhood ecosystem. The acquisition significantly strengthened Robinhood's global licensing portfolio and institutional crypto capabilities.

This illustrates that Robinhood is not merely treating crypto as another product category within its brokerage app. Rather, it is using acquisitions to build a complete crypto ecosystem encompassing exchanges, regulatory licenses, institutional clients, and global operating capabilities.

More importantly, Robinhood is actively bringing traditional financial assets onto blockchain infrastructure.

On June 30, 2025, Robinhood announced the launch of Stock Tokens in Europe and revealed plans to develop Robinhood Layer 2, a blockchain network designed to support tokenized real-world assets, 24/7 trading, cross-chain interoperability, and self-custody.

The initial issuance of these stock tokens takes place on Arbitrum, with a future migration planned to Robinhood's proprietary Layer 2 built using the Arbitrum technology stack.

These Classic Stock Tokens are derivative instruments issued in connection with Robinhood that track the price performance of the corresponding stocks and exchange-traded products (ETPs).

This approach stands in sharp contrast to Gate's strategy.

While Gate emphasizes direct access to real securities through regulated brokerage infrastructure, Robinhood focuses on transforming traditional equity exposure into tokenized or quasi-on-chain financial instruments.

2.3 The Shared Destination: Competing for the Next Generation of Integrated Financial Accounts

For ordinary investors, the financial classification of an asset is becoming increasingly irrelevant.

Most users do not particularly care whether they are trading stocks, cryptocurrencies, ETFs, event contracts, or tokenized securities. What truly matters is whether everything can be traded through a single account, whether transactions can be executed at low cost, whether prices are updated in real time, and whether portfolios can be reallocated instantly during periods of market volatility.

This is precisely why traditional brokerages are embracing crypto assets. Their objective is not simply to become another Gate or another centralized exchange. Rather, they seek to ensure that the next generation of financial user entry points does not become dominated by crypto-native platforms.

Accordingly, the critical question is not whether any individual product succeeds in the short term. What matters is that the direction of industry convergence has become unmistakably clear.

Traditional financial institutions seek the speed, global liquidity, younger user base, and high-frequency trading behavior that characterize crypto markets.

Crypto platforms, meanwhile, seek access to traditional finance's real-world assets, regulatory legitimacy, institutional credibility, and broader asset universe.

Each side is moving toward what the other does best. The boundary between crypto and traditional finance is therefore disappearing—not only at the product level, but increasingly at the infrastructure level.

The next stage of competition will no longer revolve around individual asset classes. Instead, it will be defined by regulatory capabilities, breadth of asset coverage, capital efficiency, user experience, and, ultimately, ownership of the global integrated financial account.

3. RWAs and On-Chain Treasuries: The Middleware of a Unified Capital Market

The convergence represented by Gate and Robinhood takes place at the user-entry level. RWAs and tokenized Treasuries, by contrast, represent convergence at the asset layer.

Historically, one of crypto's biggest limitations has been the relatively closed supply of on-chain assets. Beyond native tokens, stablecoins, NFTs, and a limited range of derivative assets, blockchain networks have struggled to support a sufficiently diverse universe of real-world, low-volatility, yield-generating assets suitable for institutional investors.

Tokenized U.S. Treasuries are changing this dynamic. Once U.S. Treasuries, money market funds, and short-duration bond funds are tokenized, they effectively become the blockchain ecosystem's closest equivalent to "risk-free" yield. These assets can serve as collateral, participate in DeFi strategies, support institutional treasury management, and provide the yield foundation behind stablecoins and other on-chain financial products.

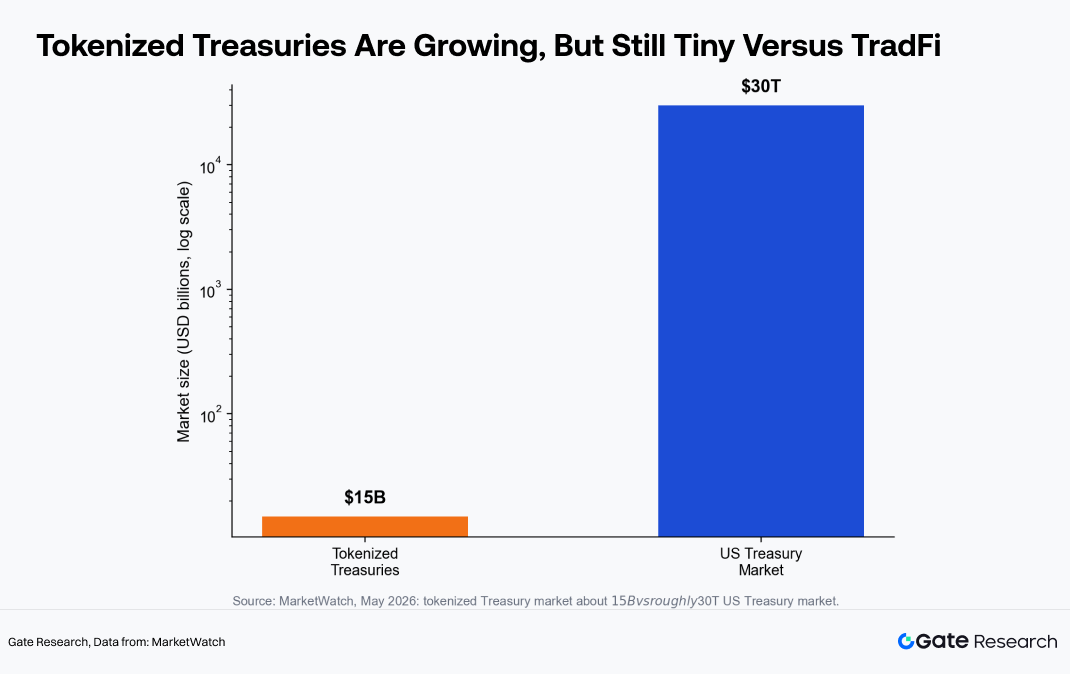

Even so, the market remains in its infancy. As of May 2026, the tokenized U.S. Treasury market was valued at approximately $15 billion, while the overall U.S. Treasury market exceeded $30 trillion—a difference of more than three orders of magnitude.

This gap reveals two important realities. First, RWA is not a mature market—it is only beginning its institutionalization. Second, its long-term growth potential does not depend primarily on crypto-native users. Rather, it depends on whether traditional financial assets can enter blockchain networks through compliant, auditable, settlement-ready, and distributable structures.

This is precisely why institutions such as JPMorgan, BlackRock, Franklin Templeton, BNY, DTCC, and Nasdaq all feature prominently in the tokenization narrative. In the long run, these institutions are not merely launching isolated crypto products; they are experimenting with the future infrastructure for capital market settlement and asset registration.

Market data further demonstrates that this convergence is not simply a narrative—it is a structural trend. During the first half of 2026, the overall cryptocurrency market declined by approximately 28%, while total value locked (TVL) in DeFi fell by more than 25%. In contrast, the RWA sector expanded by more than 40%, surpassing $32 billion in market size.

Tokenized equities emerged as the primary growth engine. The number of wallets holding tokenized stocks increased by 188% within six months to approximately 350,000, making tokenized equities the largest RWA category by wallet count, overtaking tokenized gold.

This suggests that a growing number of crypto-native investors seeking exposure to U.S. equities have found an alternative that does not require returning to traditional brokerage platforms.

At the same time, institutions including DTCC, as well as major banks in the United States and Japan, have announced plans to enter the market between 2026 and 2027, with the objective of transforming tokenized equities into core financial infrastructure.

4.1 A Unified Capital Market and the "Super Account"

Under the traditional financial system, different asset classes are fragmented across separate accounts. Stocks reside in brokerage accounts; mutual funds are managed through asset management platforms; bonds trade within institutional systems; bank deposits remain inside banking networks; cryptocurrencies are held on exchanges or in wallets; and on-chain assets exist within self-custodied blockchain addresses. Each asset class has its own trading hours, settlement cycle, custody model, regulatory requirements, and user interface.

The next generation of financial platforms is attempting to compress all of these distinctions into a single account. Crypto exchanges are expanding outward from digital assets into equities, ETFs, RWAs, payments, and on-chain yield products. Traditional brokerages are moving beyond equities into cryptocurrencies, tokenized securities, prediction markets, stablecoins, and around-the-clock trading. Asset managers are extending beyond mutual funds into ETFs, tokenized investment funds, and blockchain-based distribution. Banks are expanding beyond deposits and payments into tokenized deposits, on-chain payment systems, and institutional settlement networks. On the surface, each institution appears to be building different products.

In reality, they are all competing for the same objective: becoming the default gateway to the next generation of multi-asset financial accounts. Whoever controls that gateway controls distribution. Whoever controls distribution ultimately influences liquidity, pricing, custody, and even asset issuance.

The emerging vision is one in which investors can trade BTC, ETH, Apple shares, NVIDIA shares, S&P 500 ETFs, tokenized U.S. Treasuries, money market funds, gold, RWAs, prediction market contracts, and even tokenized private company equity—all through a single interface.

Stablecoins may become the common capital layer connecting different markets. Tokenized Treasuries may evolve into the primary source of collateral and yield generation. ETFs and tokenized funds may become the bridge through which traditional financial assets enter crypto-native accounts.

Meanwhile, the distinction between brokerage applications and crypto exchange applications will continue to fade. The future is unlikely to be fully decentralized, nor will it be entirely controlled by Wall Street. A hybrid structure is more likely to emerge. Asset issuance will remain regulated. Custody will continue to rely on licensed financial institutions. Securities trading will still be subject to jurisdictional restrictions and investor suitability requirements.

Yet trading interfaces, capital mobility, settlement speed, and portfolio construction will increasingly resemble those of crypto markets. The defining competition of the next-generation capital market will no longer be between crypto exchanges and stock exchanges. Instead, it will be a competition over who can integrate the broadest asset universe, deepest liquidity, most trusted custody infrastructure, and smoothest user experience into a single financial account.

4.2 Conclusion: Wall Street Has Not Conquered Crypto—Nor Has Crypto Bypassed Wall Street

The "Wall Street-ization" of crypto finance should not be interpreted as traditional finance taking over the crypto industry. More accurately, it represents a process of mutual transformation.

The next phase of competition is unlikely to be defined by isolated battles between centralized exchanges and traditional brokerages. Instead, it will revolve around competition between integrated financial super-platforms.

Crypto exchanges will continue expanding into equities, ETFs, bonds, mutual funds, gold, foreign exchange, payments, and wealth management. Traditional brokerages will continue expanding into spot crypto trading, staking, tokenized assets, stablecoin payments, and on-chain settlement. Ultimately, users may no longer distinguish between a "crypto exchange" and a "stock brokerage." Instead, they will interact with a single integrated account containing BTC, ETH, USDT, U.S. equities, ETFs, gold, tokenized Treasuries, and on-chain yield products. Over the long term, asset classes will continue to matter, and regulatory boundaries will remain in place. What will change is the user experience.

Today's fragmented financial ecosystem will gradually give way to a unified market in which stocks, cryptocurrencies, RWAs, and tokenized Treasuries coexist within the same capital layer, the same account structure, and the same trading interface.

Wall Street has not simply conquered crypto. Nor has crypto circumvented Wall Street. Together, they are reshaping the capital markets into an entirely new form. This brings us back to the message embedded by Satoshi Nakamoto in Bitcoin's genesis block.

Seventeen years ago, Bitcoin sought to bypass Wall Street and build an entirely new financial system. Seventeen years later, Bitcoin and Wall Street are jointly constructing a new financial infrastructure. The ideal of decentralization has not disappeared—it continues to operate at the protocol layer. Meanwhile, at the application layer that ordinary users interact with every day, a more efficient, more global, and more open unified capital market is quietly taking shape at the intersection of these two converging paths.

Data Source:

Gate Research is a comprehensive blockchain and cryptocurrency research platform that provides deep content for readers, including technical analysis, market insights, industry research, trend forecasting, and macroeconomic policy analysis.

Disclaimer

Investing in cryptocurrency markets involves high risk. Users are advised to conduct their own research and fully understand the nature of the assets and products before making any investment decisions. Gate is not responsible for any losses or damages arising from such decisions.