Summary

-

The core valuation framework for Strategy is a combined function of its BTC reserves, financing capacity, and capital markets premium. As a floating-rate perpetual preferred stock, STRC adds a yield-oriented, long-duration, and tiered-capital instrument to support the company’s BTC treasury strategy.

-

STRC is anchored to a $100 par value and currently offers an 11.5% stated dividend rate, implying an effective yield of around 11.62%. This is materially higher than short-duration U.S. Treasuries, investment-grade credit, high-yield bonds, and traditional preferred stock ETFs. Investor returns are driven primarily by cash distributions, potential convergence back to par value, and improvements in Strategy’s credit profile, rather than direct linear beta exposure to BTC upside.

-

From the issuer’s perspective, STRC effectively converts yield-seeking capital into incremental BTC purchasing power. Based on current BTC prices, every $100 million of STRC issuance could theoretically fund the acquisition of roughly 1,291 BTC. However, this flywheel depends on BTC delivering long-term returns above STRC’s dividend cost, Strategy maintaining open access to capital markets, and investors continuing to accept BTC-linked credit risk.

-

On-chain, protocols including Ondo Finance’s STRCon, xStocks STRCx, as well as Pendle, Morpho, Apyx, and Saturn are building tokenized wrappers, stablecoin integrations, yield-splitting structures, and collateralized lending use cases around STRC-like assets. Over the long run, STRC could evolve into a foundational credit asset within the BTC yield ecosystem, although its risks may also be amplified through credit spread widening, BTC volatility, and DeFi leverage dynamics.

1. The BTC Treasury Strategy and the Emergence of STRC

STRC should be viewed within the broader evolution of Strategy’s BTC treasury capital structure. Since adopting a Bitcoin-centric corporate strategy, the market’s valuation anchor for Strategy has shifted away from its legacy software business toward a composite function of BTC reserves, financing capacity, and capital markets premium. The software segment still provides the listed corporate vehicle, regulatory disclosure framework, and baseline operating cash flow, while BTC reserves form the core asset base. Capital markets instruments, meanwhile, serve as the primary mechanism for expanding both liabilities and equity financing. Strategy’s key competitive advantage today lies in its ability to continuously raise U.S. dollar funding at relatively low capital costs and convert that capital into additional BTC reserves.

The model operates through a reinforcing cycle. Capital markets endorse Strategy’s BTC treasury narrative and assign elevated valuations to MSTR and related financing instruments. The company then uses these valuation windows to issue equity, debt, convertible notes, or preferred shares. The proceeds are deployed into additional BTC purchases, expanding the company’s holdings and reinforcing market perception of its asset base and strategic scarcity value. That, in turn, reopens financing windows for future capital raises. STRC emerged after this cycle entered a more mature stage, adding a yield-oriented, long-duration instrument with tiered pricing characteristics to Strategy’s capital structure.

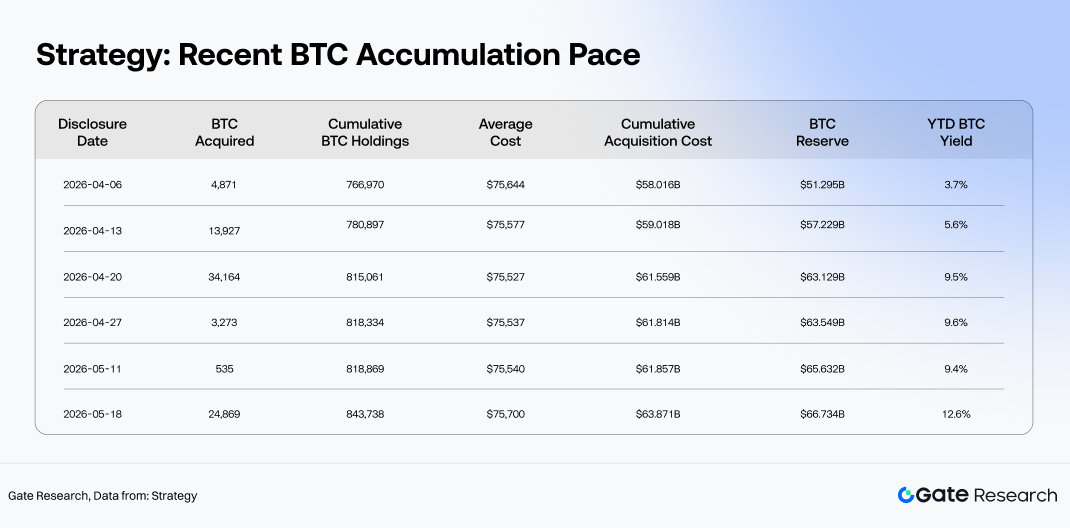

In terms of scale, Strategy is no longer simply a public company with BTC exposure. It has evolved into one of the world’s most representative institutional BTC reserve platforms. According to disclosures on Strategy’s official website, as of May 18, 2026, the company held 843,738 BTC, acquired at a cumulative cost basis of approximately $63.87 billion, with an average purchase price of roughly $75,700 per BTC. The total BTC reserve value stood at around $66.73 billion. Since the beginning of 2026, holdings increased from roughly 672,500 BTC to 843,738 BTC, representing net additions of approximately 171,238 BTC. Despite persistent BTC volatility, relatively elevated interest rates, and rapidly shifting risk-asset sentiment, Strategy has maintained a steady pace of accumulation, highlighting its strategic objective of proactively expanding BTC reserves.

As Strategy’s BTC holdings expanded, the company’s central question shifted from whether to buy more BTC to how to continue accumulating BTC at an efficient cost of capital. Equity issuance can amplify BTC reserves, but it dilutes existing shareholders. Traditional debt financing avoids equity dilution, yet introduces fixed repayment obligations. Convertible bonds offer relatively low financing costs during bull markets, but their effectiveness depends heavily on MSTR share volatility, conversion premiums, and investor appetite for embedded optionality. STRC, as a preferred equity instrument, sits between common equity and debt in the capital structure. Issued by Strategy as a floating-rate perpetual preferred stock, it provides investors with explicit distribution expectations while allowing the issuer to avoid the principal maturity burden associated with conventional debt. Within the capital stack, it occupies a risk tier senior to common equity but junior to debt obligations.

Market conditions have further strengthened demand for this type of instrument. Spot BTC ETFs have accelerated Bitcoin’s integration into institutional asset allocation frameworks, gradually positioning BTC as a form of digital reserve asset within macro portfolios. According to CoinMarketCap data, as of May 20, 2026, BTC traded at approximately $77,524, with a market capitalization of around $1.55 trillion and market dominance near 60.4%. BTC ETF assets under management stood at roughly $106.75 billion. Institutional access routes into BTC have expanded significantly, yet the needs of yield-oriented capital remain only partially addressed by spot ETFs. BTC itself generates no native cash flow, while spot ETFs primarily provide price exposure rather than income exposure. For fixed-income-oriented investors, cash flow-focused allocators, or stablecoin reserve managers, the BTC narrative still needs to be transformed into a distributable, measurable, and risk-manageable yield-bearing asset.

STRC is neither equivalent to MSTR common stock, where returns are primarily driven by equity beta, nor is it a traditional corporate bond. Its credit foundation is tightly linked to Strategy’s BTC reserves, refinancing capacity, and access to capital market premiums. Investors purchasing STRC are effectively buying a hybrid capital instrument that uses Strategy’s corporate credit as the wrapper, the BTC treasury strategy as the underlying asset narrative, and cash distributions as the primary return driver. Its risk pricing incorporates three layers: Strategy’s corporate credit quality, fluctuations in BTC reserve value, and the market’s continued willingness to support the company’s financing flywheel.

Strategy’s capital structure is also evolving beyond a single-stock MSTR narrative into a multi-instrument, multi-layered credit ecosystem. Company data shows MSTR common equity market capitalization at roughly $57.89 billion, compared with BTC reserve value of around $65.34 billion during the same period. Comparing common equity valuation against BTC reserve value alone is no longer sufficient to explain Strategy’s full market pricing. Debt instruments alongside STRC, STRK, STRF, STRD, and STRE collectively form what is increasingly becoming a digital credit stack, with each instrument targeting different duration profiles, seniority levels, yield characteristics, and volatility exposure. Strategy’s BTC NAV premium is therefore no longer concentrated solely in MSTR common stock, but increasingly distributed across a broader set of capital market products backed by BTC reserves.

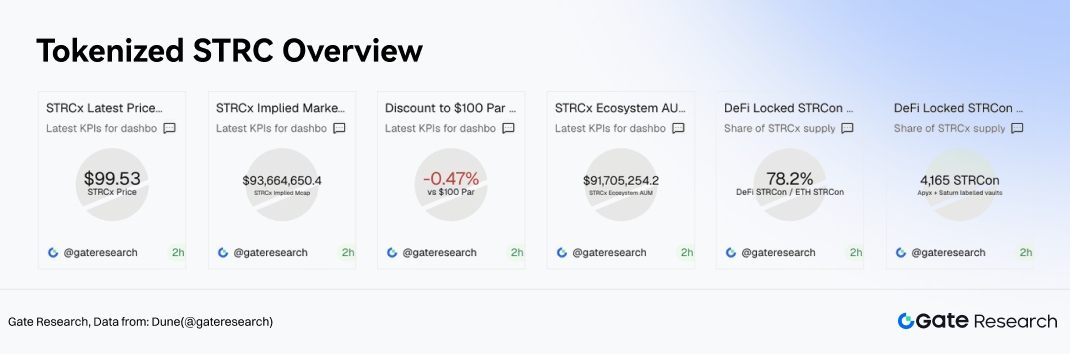

Early on-chain trading activity in tokenized STRC products also provides a useful market signal. xStocks’ STRCx recently traded at $99.53, representing a discount of roughly 0.47% to its $100 par value. On-chain mapped supply stood at approximately 941,100 tokens, implying a market capitalization near $93.66 million, while ecosystem AUM totaled roughly $91.71 million. Trading close to par suggests the market is initially treating STRC-like instruments as yield-oriented credit assets. The modest discount reflects a combination of compensation for on-chain liquidity constraints, redemption efficiency of tokenized assets, issuer credit risk, and secondary market depth.

The strategic importance of STRC lies in its ability to open access to a more segmented capital pool for Strategy. Common equity investors seek BTC upside participation, convertible bond investors focus on volatility and embedded conversion optionality, while traditional debt investors prioritize repayment safety margins. STRC, by contrast, is designed to attract yield-oriented capital into Strategy’s BTC treasury ecosystem. The instrument effectively connects the financing needs of a BTC reserve company with market demand for high-yield, distributable, and composable on-chain assets.

If STRC and its tokenized variants continue expanding into DeFi use cases such as stablecoin reserves, Pendle yield-splitting strategies, and Morpho collateralized lending markets, their role could evolve beyond simple financing instruments into foundational credit assets underpinning on-chain yield infrastructure. In that sense, the launch of STRC marks a broader transition in Strategy’s BTC strategy: from merely accumulating BTC reserves to issuing digital credit assets backed by those reserves.

2. STRC Structure, Yield Profile, and Valuation Framework

STRC, short for Variable Rate Series A Perpetual Stretch Preferred Stock, is a floating-rate perpetual preferred security issued by Strategy. It is neither a low-volatility substitute for MSTR common equity nor simply a higher-yield version of a traditional corporate bond. Its core investment characteristics are shaped by four elements: a fixed par value anchor, adjustable dividend rates, preferred liquidation seniority, and active issuer management of distributions and redemption mechanisms. Investors buying STRC are effectively purchasing a yield structure built around cash distributions and par-value stability, rather than direct linear exposure to BTC price appreciation.

2.1 Core Terms: Par Value Anchor, Monthly Distributions, and Floating Dividend Rates

According to Strategy’s March 23, 2026 STRC Stock Annex, STRC carries a stated amount of $100 per share, with an initial liquidation preference also set at $100 per share. The liquidation preference cannot be adjusted below that level. As a perpetual preferred security, STRC has no fixed maturity date, meaning investors cannot simply hold it to maturity for principal repayment like a conventional bond. Its “principal-like” characteristics instead come from the par-value anchor, liquidation preference, redemption structure, and active market price management.

STRC distributions are cumulative dividends accrued against the $100 stated amount. Dividends are payable only when declared by the board and when legally available funds exist. Distributions are currently made monthly, with payments at month-end and the 15th of each month serving as the standard record date. This structure gives STRC a predictable cash flow profile and naturally positions its investor base closer to yield-oriented capital rather than high-beta equity investors.

The dividend mechanism is the most important feature within STRC’s structure. The initial dividend rate was set at 9%, while Strategy retains the ability to adjust the rate monthly within specified limits. Official documentation explicitly states that the company’s current intention is to manage the dividend rate in a way that keeps STRC trading at or near $100 per share. If the market price falls below par, the issuer has an incentive to raise the dividend rate to improve yield attractiveness. If the market price rises above par, the issuer can lower the dividend rate to suppress excessive premium expansion. As a result, STRC effectively functions as a dividend-adjusted par-value anchored instrument.

2.2 Current Pricing: Trading Near Par With Yields Well Above Traditional Credit Assets

According to Strategy’s official STRC data, as of May 20, STRC traded at $98.99 per share, with a current stated dividend rate of 11.5% and an effective yield of 11.62%. Total notional size stood at approximately $10.49 billion, while market capitalization was around $10.38 billion. Looking at distribution history, monthly cash payouts gradually increased from $0.80 per share in August 2025 to $0.96 per share between March and May 2026, corresponding to a rise in distribution rates from 9.00% to 11.50%.

2.3 Seniority and Redemption Structure: Limited Upside, Downside Driven by Credit and Dividend Adjustments

STRC’s position within the capital structure defines its risk boundaries. Its dividends and liquidation claims rank senior to Strategy Class A common stock, Class B common stock, and junior securities such as STRE, STRK, and STRD. However, it ranks below STRF, outstanding corporate debt, future senior debt obligations, and structurally below liabilities held at subsidiary entities. This positioning places STRC above common equity but below debt, giving it a risk-return profile more comparable to high-yield preferred securities.

Its redemption structure also caps upside potential. Strategy may redeem all or part of the outstanding STRC at $101 per share plus accrued unpaid dividends. Under clean-up redemption or tax event scenarios, redemption pricing is generally based on liquidation preference plus accrued unpaid dividends. In the event of a fundamental change, holders may require the company to repurchase STRC at the $100 stated amount plus accrued unpaid dividends. Together, these provisions create a relatively defined trading range. When STRC trades below par, investors focus on dividend income and potential price recovery toward $100. When prices move above roughly $101, redemption rights and dividend adjustment mechanisms tend to suppress further premium expansion.

This marks a fundamental distinction between STRC and common equity. MSTR common stock derives upside primarily from BTC beta, mNAV expansion, and broader market risk appetite. STRC’s upside is driven mainly by discount compression and mean reversion toward par value, with price appreciation constrained by structural terms. The investment thesis is therefore not centered on multiple expansion, but rather on whether current yields adequately compensate investors for credit, liquidity, and structural risks.

2.4 Sources of Return: Cash Distributions, Par Recovery, and Credit Spread Compression

The first source of return for STRC is cash distributions. The current 11.5% distribution rate translates into approximately $11.50 per share annually, generating an effective yield of 11.62% at the current $98.99 trading price. This yield is materially higher than short-duration U.S. Treasuries, investment-grade credit, high-yield bonds, and traditional preferred stock ETFs, suggesting the market views STRC primarily as a higher-risk credit instrument rather than a conventional fixed-income product.

The second source of return comes from convergence toward par value. Both STRC and tokenized STRCx currently trade modestly below the $100 par anchor. If distributions remain stable, liquidity improves, and credit concerns ease, prices could gradually move back toward par. While the magnitude of this return component may be limited, it remains meaningful for yield-focused investors because it determines whether total return can exceed dividend income alone.

The third source of return is credit spread compression. STRC valuation is not directly equivalent to BTC price performance, but Strategy’s perceived credit strength strongly influences STRC discount levels and required yields. When markets believe Strategy can continue funding distributions, maintain capital market access, and actively manage its balance sheet, STRC discounts tend to narrow. Conversely, if investors become concerned about distribution sustainability, financing conditions, or BTC reserve volatility, higher yields may be required as compensation, placing downward pressure on prices.

2.5 Relative Valuation: STRC Is a High-Yield Credit Instrument, Not a Risk-Free Yield Substitute

Compared with traditional income-generating assets, STRC offers a substantially higher yield profile. Based on Strategy’s comparable market data, short-duration Treasury vehicles such as SGOV, BIL, and SHV currently yield around 3.55% to 3.57%. Intermediate- and long-duration Treasury exposure through IEF offers roughly 4.03%. Investment-grade corporate bond ETFs such as LQD and VCIT yield approximately 4.76% to 4.80%, while high-yield credit ETFs including HYG and JNK trade around 6.33% to 6.62%. Traditional preferred stock ETFs such as PFF and PGX yield roughly 5.44% to 5.50%. Against that backdrop, STRC’s 11.62% effective yield stands out as materially higher than most conventional income assets.

That said, STRC’s elevated yield should not be viewed as a risk-free carry opportunity. Its yield premium compensates investors for several distinct risks. Distributions are not contractual debt interest payments, and remain subject to board declaration. The company also retains discretion to adjust distribution rates, exposing investors to policy-driven yield changes over time. STRC ranks below corporate debt and STRF in the capital structure, while its price stability ultimately depends on continued market confidence in Strategy’s credit profile and dividend adjustment framework.

The allocation case for STRC therefore lies in offering enhanced yield and BTC treasury-related premium exposure to investors willing to accept a specific set of credit and structural risks tied to Strategy.

3. The STRC Financing Flywheel: From Yield Instrument to BTC Accumulation Engine

After understanding STRC’s structure and yield mechanics, the next step is to examine the instrument from the issuer’s perspective: how Strategy uses STRC as a financing engine for continued BTC accumulation. STRC’s core value lies not only in offering investors a high-yield credit instrument, but also in providing Strategy with a long-duration source of capital that has no fixed maturity and operates around a relatively stable par-value anchor. As long as STRC can continue to be issued near par and the market remains willing to accept its combination of dividend yield and credit risk, the instrument can remain embedded within Strategy’s BTC treasury flywheel, functioning as an intermediary layer connecting yield-oriented capital with BTC reserve expansion.

3.1 The Flywheel: Converting Yield Capital Into BTC Reserves

The STRC financing flywheel can be broken down into five stages. Strategy issues STRC and raises U.S. dollar capital. The proceeds are used for general corporate purposes, including additional BTC purchases. As BTC holdings increase, the company’s asset base and market narrative strengthen. A larger BTC reserve base improves capital market perception of Strategy’s balance sheet strength and financing capacity. The company can then continue raising capital through common equity, preferred stock, debt, or other instruments, recycling fresh capital into further BTC accumulation.

What differentiates this model from traditional corporate finance is that Strategy’s asset base is not composed of conventional operating assets, but rather highly liquid and highly volatile BTC reserves. The capital attracted through STRC is also distinct from typical equity risk capital, instead coming primarily from yield-oriented investors. The success of the flywheel depends on whether Strategy can continuously channel a portion of fixed-income and preferred-equity capital into its BTC accumulation framework at an acceptable cost of capital.

The process can be simplified as follows:

STRC issuance → USD financing → BTC accumulation → larger BTC reserves → stronger credit foundation → improved financing capacity → continued BTC accumulation

When this mechanism functions smoothly, STRC serves as an asset expansion tool. If the cycle breaks down, however, STRC can instead become a source of capital structure pressure. The dividing line depends on three variables: whether BTC’s long-term returns exceed STRC’s financing cost, whether Strategy’s access to capital markets remains open, and whether investors continue accepting BTC-linked credit exposure.

3.2 Financing Efficiency: How Much BTC Can $100 Million of STRC Buy?

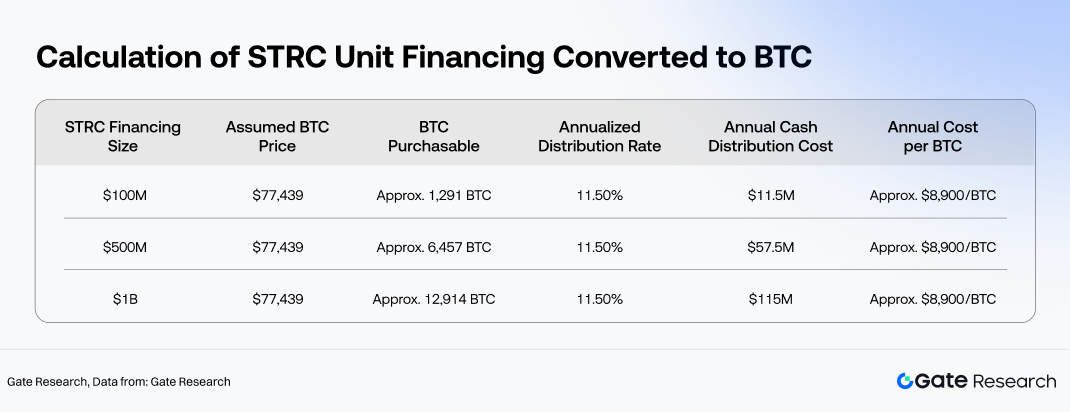

Based on a BTC price of approximately $77,439 as of May 20, every $100 million of STRC issuance could theoretically fund the purchase of roughly 1,291 BTC. Using STRC’s current 11.5% distribution rate, $100 million of issuance would correspond to approximately $11.5 million in annual cash distribution obligations. On a per-BTC basis, that implies an annual financing cost of roughly $8,900 per BTC acquired, equivalent to around 11.5% of the original purchase price.

From an economic return perspective, the long-term annualized return on newly acquired BTC must exceed STRC’s roughly 11.5% distribution cost for the flywheel to generate positive asset expansion. If BTC’s long-term return falls below the funding cost, additional BTC purchases may increase reserve size but reduce overall capital efficiency. Conversely, if BTC materially outperforms the financing cost, STRC effectively becomes a capital instrument that uses fixed-income-oriented funding to amplify long-term BTC appreciation.

It is important to distinguish between economic return and cash flow matching. Rising BTC prices can improve asset coverage ratios and strengthen Strategy’s credit profile, but BTC itself does not automatically generate U.S. dollar cash flow. STRC distributions must be paid in dollars, with funding potentially sourced from common equity ATM issuance, additional financing activities, USD reserves, or operating cash flow rather than BTC-generated income. As a result, the truly sustainable version of the flywheel is not simply “BTC appreciation covers distributions.” Instead, BTC appreciation improves financing capacity, financing capacity supports cash distributions, and that financing flexibility allows Strategy to continue holding or accumulating BTC.

3.3 Dividend Costs vs. BTC Returns: The Economic Breakeven Threshold of the Flywheel

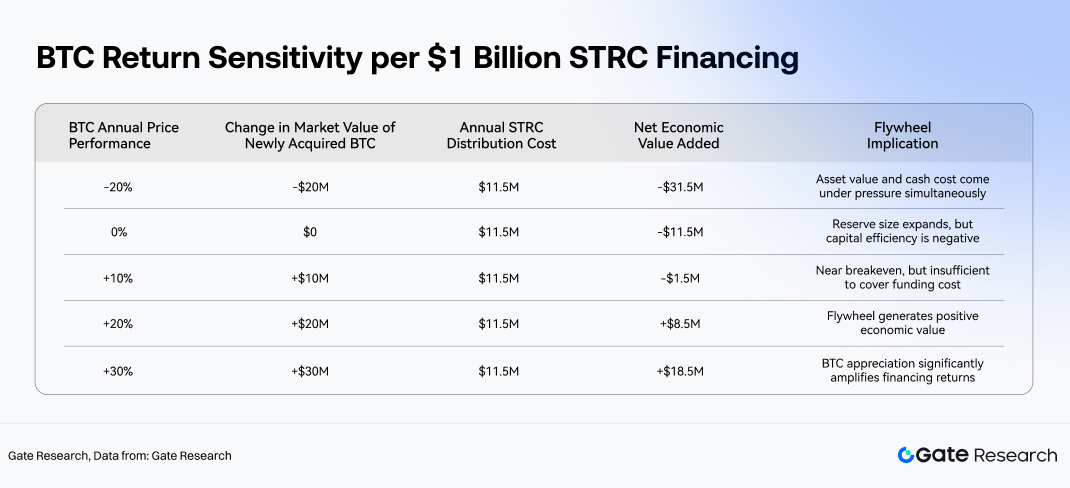

Using the current 11.5% distribution rate as a baseline, the economic breakeven point for STRC can be approximated by whether BTC’s long-term annualized return exceeds 11.5%. With every $100 million of STRC issuance funding the purchase of roughly 1,291 BTC, the economics become relatively straightforward. If BTC appreciates 10% over one year, the mark-to-market increase in the newly acquired BTC reserve would be around $10 million, below the approximately $11.5 million annual distribution obligation. If BTC rises 20%, the reserve value increase would reach roughly $20 million, materially exceeding the dividend cost. At 30% BTC appreciation, the newly added asset value would increase by approximately $30 million, making the leverage effect of the financing structure significantly more attractive.

This framework does not imply that STRC distributions must be directly funded by the short-term appreciation of newly purchased BTC. Rather, it measures capital allocation efficiency: after raising capital at an annualized cost of 11.5%, can Strategy deploy that capital into BTC assets capable of generating higher long-term returns? If BTC’s long-term return persistently falls below STRC’s funding cost, the financing flywheel risks deteriorating from an accumulation engine into an expensive balance sheet expansion mechanism. If BTC’s long-term return exceeds the funding cost, however, STRC can effectively transform yield-oriented capital into BTC reserve appreciation.

This logic also highlights the distinction between STRC financing and common equity issuance. Common stock carries no fixed distribution obligation but dilutes shareholder ownership. STRC involves far less dilution, yet creates an ongoing cash distribution commitment. The two are therefore not substitutes, but complementary financing tools serving different capital sources under different market conditions. When MSTR valuation and financing windows are strong, equity issuance offers greater flexibility. When yield-oriented investors are willing to allocate to high-distribution preferred securities, STRC broadens Strategy’s capital pool and reduces dependence on a single source of equity financing.

3.4 Asset Coverage Stress Testing: How BTC Declines Affect the STRC Flywheel

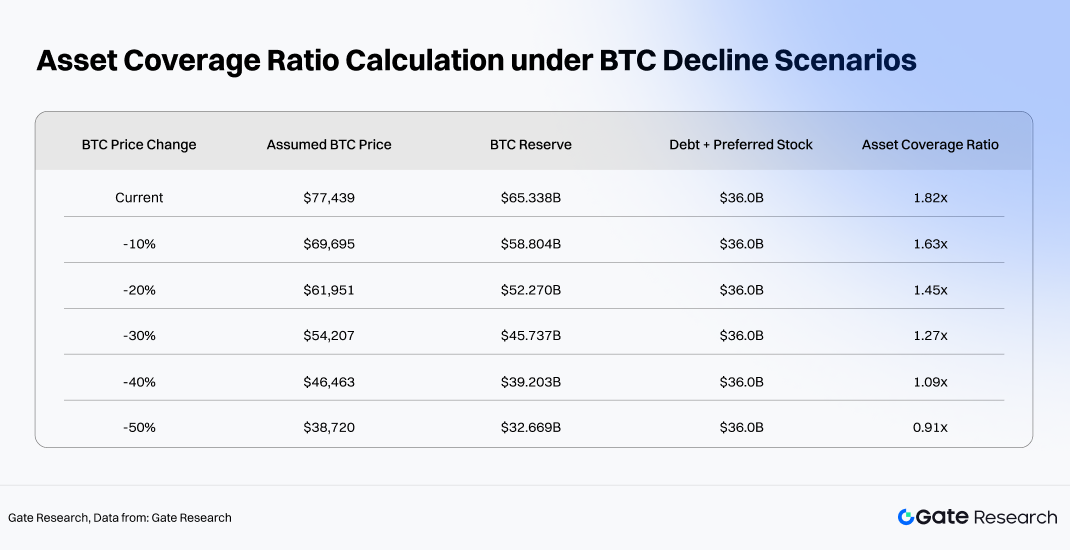

The primary vulnerability of the STRC flywheel comes from the volatility of BTC reserves. As of May 20, Strategy’s BTC reserve value stood at approximately $65.34 billion, while total debt and preferred securities amounted to roughly $36 billion. Using BTC reserves divided by total debt and preferred obligations as a simplified measure, current asset coverage stands at around 1.82x. While this is not a formal legal liquidation coverage ratio, it provides a useful indication of how much protection the BTC reserve base offers to fixed-income and preferred layers within the capital structure.

The stress test suggests that the STRC financing flywheel still retains a meaningful asset buffer during moderate BTC drawdowns. Even with BTC declining by around 30%, asset coverage would compress but remain above 1x. At roughly a 40% decline, the margin of safety becomes noticeably thinner. If BTC falls by 50%, however, the value of BTC reserves would drop below the combined amount of debt and preferred securities, significantly increasing pressure on the capital structure. At that stage, STRC’s market behavior would likely shift toward a credit-risk repricing framework, with investors demanding higher yields, wider trading discounts, and potentially reducing Strategy’s ability to issue additional preferred securities efficiently.

A second layer of transmission also emerges under stress conditions. BTC price declines not only weaken asset coverage ratios, but also reduce the financing flexibility of MSTR common equity, narrow preferred issuance windows, and increase the cost of new capital. Because STRC distributions are dollar-denominated cash obligations, if the market is no longer willing to purchase STRC or related financing instruments near par value, Strategy may need to rely on USD reserves, alternative financing channels, or asset sales to sustain distributions. According to Strategy disclosures, total annual distribution obligations are approximately $1.712 billion. Existing USD reserves could theoretically cover around 15.77 months of distributions, while BTC reserves correspond to roughly 38.17 years of distribution coverage on a notional basis. The former measures near-term cash buffer strength, while the latter reflects balance sheet asset depth. In practice, flywheel stability depends far more on liquidity reserves and continued financing access than on nominal BTC reserve size alone.

3.5 Market Premium and Financing Windows: The External Constraints of the Flywheel

The sustainability of the STRC flywheel depends not only on BTC returns, but also on continued access to favorable financing windows. Strategy’s expansion model requires capital markets to keep supporting its multi-layered securities ecosystem. Common equity investors must continue accepting BTC beta exposure. Debt investors must tolerate the associated credit risk. Convertible bond buyers must remain comfortable with volatility-based pricing dynamics. STRC investors must continue accepting the preferred equity distribution model and par-value anchor structure. If any one financing layer closes, the flywheel slows. If multiple financing channels contract simultaneously, the flywheel could be forced to decelerate sharply or even reverse.

The fact that STRC continues to trade near par value is itself an important signal that financing conditions remain functional. STRC currently trades at $98.99 with an effective yield of 11.62%, while the on-chain tokenized version, STRCx, trades at $99.53, representing only a 0.47% discount to par. This pricing behavior indicates that markets are still willing to value STRC-like instruments close to their intended anchor price. As long as STRC can continue issuing near the $99 to $101 range, Strategy can raise capital close to full par value, preserving financing efficiency. If STRC were to trade materially below par for an extended period, issuing equivalent amounts of preferred stock would require either higher yields or deeper discounts, reducing the economic efficiency of the flywheel.

Another important constraint comes from MSTR common equity itself. While common stock is not the central financing instrument discussed here, it still determines the overall temperature of Strategy’s capital markets ecosystem. The more willing equity markets are to assign premium valuations to the BTC treasury model, the easier it becomes for Strategy to maintain dollar inflows through ATM issuance, convertible bonds, and other securities. When common equity valuations weaken, STRC investors may begin reassessing the sustainability of distributions and the company’s future refinancing capacity. In this sense, STRC is not a standalone high-yield product, but one component within Strategy’s broader capital structure. Its perceived credit quality is jointly shaped by BTC reserves, common equity valuation, preferred stock pricing, debt market conditions, and on-chain demand dynamics.

3.6 Conditions Required for the Flywheel to Function

In summary, the STRC financing flywheel requires three conditions to remain viable.

First, BTC’s long-term return profile must exceed STRC’s dividend cost. With STRC currently offering an effective yield of around 11.62% and a stated distribution rate of 11.5%, newly raised capital deployed into BTC must generate long-term returns above that threshold. Otherwise, the flywheel merely expands BTC exposure at a high financing cost. The assumption of strong long-term nonlinear BTC appreciation is therefore the core economic premise behind Strategy’s willingness to continue issuing yield-oriented instruments to accumulate BTC.

Second, Strategy’s capital markets premium cannot collapse materially. The flywheel depends on securities being issued at economically viable pricing levels. STRC needs to remain close to par value, MSTR must preserve sufficient liquidity and market relevance, and debt and other preferred securities must remain issuable. If markets fundamentally reprice Strategy’s BTC treasury model, financing costs would rise, issuance discounts would widen, and the effective acquisition cost of additional BTC would increase accordingly.

Third, investors must continue accepting BTC-linked credit risk. STRC buyers are not simply purchasing a high coupon product. They are underwriting a layered credit structure built around BTC reserves, preferred equity seniority, distribution policy, and ongoing refinancing capacity. As long as BTC reserves continue expanding, distributions remain stable, and STRC trades near par, the instrument can continue attracting yield-oriented capital. But if BTC experiences severe declines or markets begin questioning distribution sustainability, investors will demand higher yields, automatically slowing the flywheel.

Ultimately, STRC helps Strategy continue accumulating BTC not by merely providing another financing source, but by integrating yield-oriented capital into the company’s long-term BTC treasury cycle. Monthly distributions attract fixed-income-style investors, the $100 par-value anchor improves issuance efficiency, and preferred equity seniority reduces risk exposure relative to common stock. Strategy then converts the capital raised into additional BTC accumulation, expanding the asset side of the balance sheet. The upside potential of the flywheel is determined by BTC’s long-term return profile and sustained capital market premiums, while its downside boundaries are defined by distribution coverage capacity, asset coverage ratios, and financing window stability.

4. Tokenized STRC and the DeFi Flywheel for Yield-Bearing Stable Assets

Once brought on-chain, STRC is no longer just another yield-oriented preferred security within Strategy’s capital structure. Instead, it becomes a programmable base asset that can be tokenized, collateralized, yield-split, and recursively refinanced across DeFi. In traditional finance, STRC’s core characteristics are defined by par value, dividend rate, and issuer credit quality. In DeFi, the focus shifts toward composable cash flows. Tokenized STRC transforms what was originally a yield-bearing security held through brokerage accounts and traded on Nasdaq into an on-chain financial primitive that can integrate into stablecoins, yield-bearing assets, Pendle PT/YT structures, and Morpho lending markets.

4.1 The Tokenization Path: From STRC to STRCon and STRCx

The first stage of STRC’s on-chain expansion is tokenization, primarily through two mapped asset structures: Ondo Finance’s STRCon and xStocks’ STRCx. Both products serve the purpose of bringing STRC-like yield assets on-chain, but they differ in structure and market positioning. STRCx more closely resembles a standardized tokenized stock product, emphasizing price anchoring, supply scale, and secondary market trading. STRCon, by contrast, is positioned more deeply within protocol treasuries, stablecoin reserve structures, and composable DeFi architectures, functioning as a foundational layer for subsequent yield packaging.

In terms of scale, STRCx currently represents the larger on-chain mapping vehicle. Outstanding supply is approximately 941,100 tokens, implying a market capitalization of roughly $93.66 million, with ecosystem AUM around $91.71 million. At this size, STRCx has already reached a level where it can begin functioning as a meaningful on-chain financial asset, supporting pricing markets, collateral usage, yield splitting, and cross-protocol integration within the broader tokenized equity ecosystem.

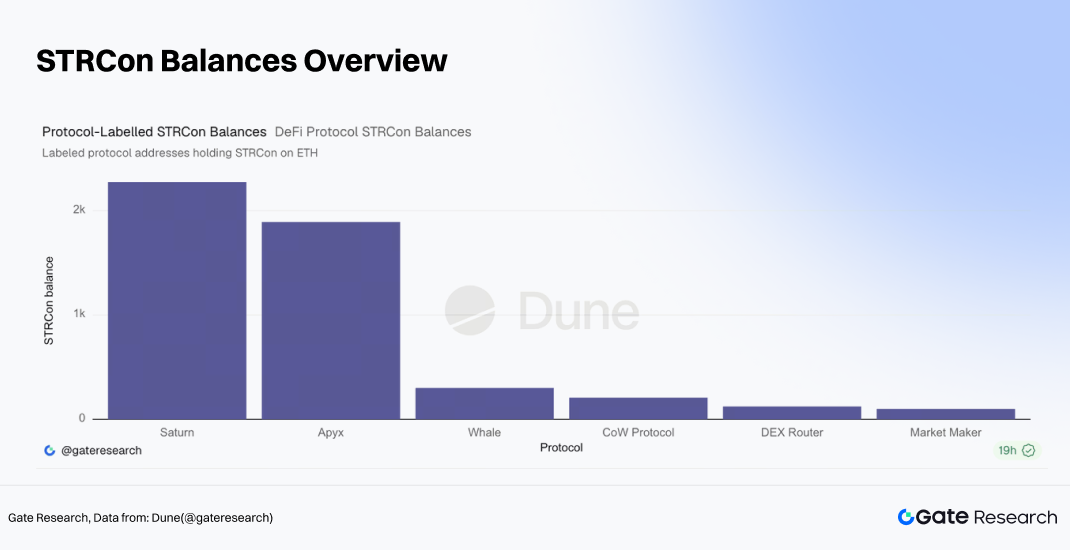

Compared with STRCx, Ondo Finance’s STRCon remains in a much earlier stage of on-chain adoption. Total supply currently stands at approximately 2,319.95 STRCon on Ethereum and around 6,072.43 STRCon on BNB Chain. What makes STRCon notable is that it has already begun flowing into a range of DeFi protocol and infrastructure addresses, including Saturn, Apyx, CoW Protocol, DEX routers, and market maker wallets. Among these, Saturn-tagged addresses hold roughly 2,273.66 STRCon, Apyx-associated addresses hold around 1,890.97 STRCon, CoW Protocol holds approximately 207.32 STRCon, DEX Router addresses about 123.77 STRCon, and market maker wallets around 99.61 STRCon.

4.2 From Asset Mapping to Yield Packaging: The Roles of Apyx and Saturn

The second layer of the on-chain STRC ecosystem is yield packaging. The native cash flow of STRC originates from periodic dividend distributions, but DeFi protocols must transform those cash flows into asset structures familiar to crypto-native users: stablecoins, yield-bearing stable assets, senior/junior tranches, and tradable yield claims. This is where protocols such as Apyx and Saturn become strategically important.

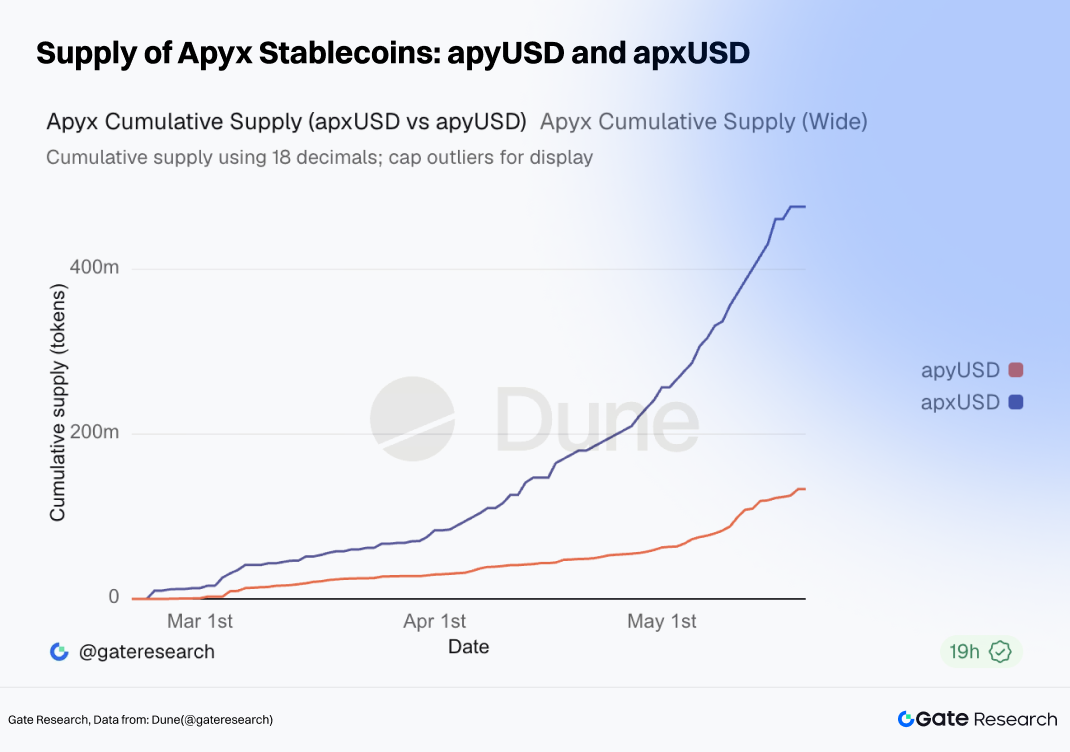

Within the Apyx ecosystem, apxUSD and apyUSD represent non-yield-bearing and yield-bearing stablecoin structures, respectively. Total supply for apxUSD has reached approximately $476 million, while apyUSD supply stands at around $133 million. In terms of network activity, cumulative transfer volume across both assets has already exceeded $3 billion. Apyx has therefore established a sizable stablecoin circulation layer built around the STRC yield narrative. apxUSD functions primarily as a stable medium of exchange, while apyUSD serves as the yield distribution vehicle. Together, the two products package underlying yield-bearing assets into dollar-denominated instruments that are more intuitive and accessible for DeFi users.

Saturn, by contrast, adopts a more structured credit-layering approach. Its jrUSDat and srUSDat products reflect a classic junior/senior tranche framework: underlying yield-bearing assets generate cash flow, and the protocol redistributes both risk and return across different layers. The senior tranche is designed to resemble a lower-risk, lower-volatility income product, while the junior tranche absorbs greater risk in exchange for potentially higher returns. Combined cumulative transfer volume for jrUSDat and srUSDat has already surpassed $10 million. Although Saturn remains smaller than the Apyx stablecoin ecosystem, it is beginning to establish a growing layer of structured liquidity built around STRC-linked yield exposure.

Taken together, this architecture closely resembles traditional securitization frameworks. Underlying STRC cash flows function as the asset pool generating returns. apxUSD and apyUSD operate as stablecoin wrappers around those returns. srUSDat and jrUSDat introduce tranche-based risk segmentation. Pendle further separates duration exposure and yield rights, while lending protocols such as Morpho provide collateralized lending and recursive leverage opportunities. The major difference is that DeFi structures operate at significantly higher composability and execution speed. Protocols can interact permissionlessly, while yields are continuously repriced in real time through secondary market activity.

4.3 DeFi Pricing: Pendle Creates an On-Chain Yield Curve for STRC Cash Flows

Once STRC becomes tokenized, its cash flows begin entering the DeFi pricing system. Markets on Pendle do not simply replicate the effective yield available on Nasdaq-listed STRC. Instead, yields are repriced according to maturity profile, liquidity conditions, tokenized asset structure, PT/YT separation mechanics, and broader protocol risk.

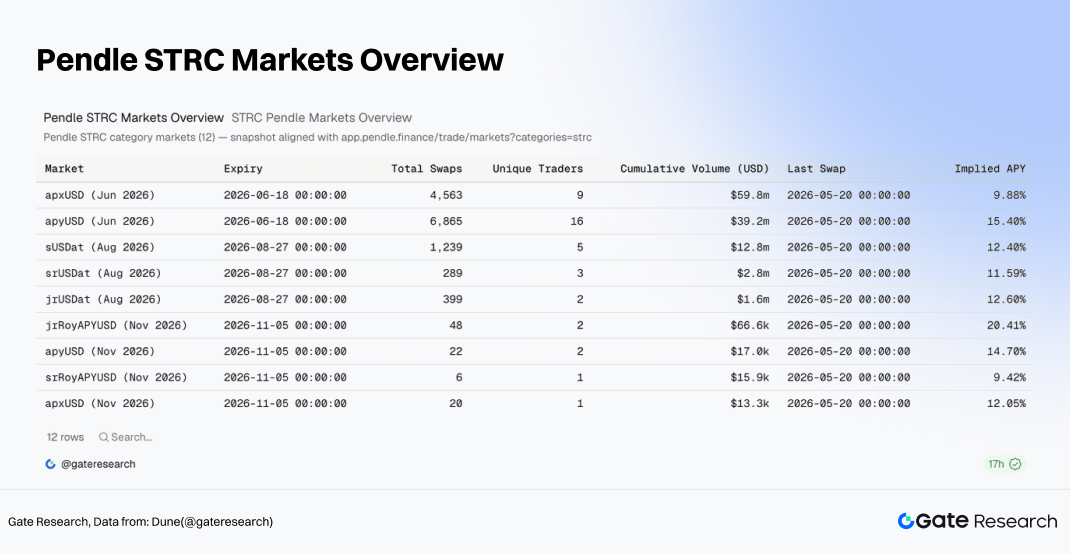

In the June 2026 markets on Pendle, cumulative trading volume for apxUSD reached approximately $59.8 million, with a latest implied APY of around 9.88%. apyUSD recorded roughly $39.2 million in cumulative trading volume and an implied APY near 15.40%. Meanwhile, the August 2026 sUSDat market generated about $12.81 million in cumulative volume, with an implied APY of approximately 12.40%. The implied APYs for srUSDat and jrUSDat currently stand at around 11.59% and 12.60%, respectively.

Pendle has effectively begun decomposing STRC-linked cash flows into multiple duration buckets and differentiated risk layers. The implied APY of srUSDat remains relatively close to STRC’s native effective yield, suggesting that the senior tranche behaves similarly to the underlying distribution stream. Higher implied APYs in markets such as apyUSD and jrUSDat reflect additional structural complexity, liquidity risk, and yield repackaging premiums. While the standalone STRCx market currently shows an implied APY of roughly 13.03%, cumulative trading volume remains relatively limited, making it less informative than the deeper apxUSD, apyUSD, and sUSDat markets.

DeFi pricing fundamentally changes the asset boundary of STRC. In traditional finance, STRC is treated primarily as a high-yield preferred security. In DeFi, STRC cash flows are decomposed into stablecoin reserves, yield-bearing tokens, PT/YT structures, and collateral assets. As a result, STRC evolves from a fixed-income-like security into a foundational yield source that can be repackaged, repriced, and releveraged across multiple on-chain protocols.

4.4 The Leverage Layer: Morpho and Collateralized Lending

Morpho represents the leverage layer within the DeFi flywheel. Once stablecoins and yield bearing assets are established, the market does not stop at simply holding them. Instead, these assets begin serving as collateral for lending, recursive leverage, and yield enhancement strategies.

The Morpho layer operates through a relatively straightforward flywheel. Users hold STRC related stablecoins or PT assets, post them as collateral, borrow stablecoins against them, and then deploy the borrowed capital into additional yield bearing assets, creating a recursive loop. If the underlying yield exceeds borrowing costs, leverage amplifies returns. If underlying assets begin trading at discounts, yields are repriced lower, or collateral liquidity deteriorates, leverage accelerates downside risk transmission. Unlike Pendle, which primarily focuses on pricing future yield streams, Morpho transforms yield bearing assets into financeable collateral. Once STRC related assets enter Morpho, they effectively become credit collateral within the DeFi system.

This is the most expansionary part of the DeFi flywheel, but also the area where systemic risk can accumulate most easily. Stablecoin issuance increases demand for underlying STRC exposure. Pendle creates yield trading markets. Morpho introduces financing leverage. Together, these layers can generate strong TVL growth momentum. At the same time, disruptions in any part of the system, including price dislocations, oracle failures, collateral ratio adjustments, or liquidity withdrawals, can quickly propagate back into the underlying tokenized STRC ecosystem.

5. Investment Appeal, Risk Scenarios, and Long Term Strategic Implications

Based on the analysis above, STRC can be understood as a high yield, par anchored, and DeFi composable credit asset within Strategy’s BTC treasury ecosystem. Its appeal comes from three main drivers. First, its cash distribution yield above 11% is materially higher than traditional credit assets. Second, Strategy’s BTC reserves provide the asset foundation supporting its credit narrative. Third, once tokenized STRC enters stablecoin systems, Pendle markets, and lending protocols, its utility expands significantly. At the same time, these strengths correspond to three major risks: whether the yield premium adequately compensates for credit exposure, whether BTC volatility could erode asset coverage buffers, and whether DeFi repackaging could transform isolated asset risk into broader on-chain liquidity risk.

5.1 Allocation Value: Yield, Par Anchor, and On Chain Composability

From a yield perspective, STRC’s relative attractiveness is fairly clear. Its current effective yield of approximately 11.62% stands well above short duration Treasury ETFs yielding around 3.55% to 3.57%, investment grade corporate bond ETFs yielding roughly 4.76% to 4.80%, traditional preferred stock ETFs yielding approximately 5.44% to 5.50%, and even high yield bond ETFs yielding around 6.33% to 6.62%. This makes STRC particularly attractive to income oriented capital. For investors seeking BTC treasury related credit exposure without taking on the full volatility of MSTR common equity, STRC provides a more explicit cash flow based investment profile.

From a pricing perspective, both STRC and STRCx continue trading close to their $100 par value. Native STRC trades around $98.99, while on chain STRCx trades near $99.53, representing only a 0.47% discount to par. This suggests the market still broadly accepts the par value anchor and distribution framework. If STRC can continue trading within the $99 to $101 range while AUM expands, it would indicate sustained market confidence in STRC as a high yield credit asset. If prices begin trading persistently below par with widening discounts, however, markets may start demanding materially higher credit compensation.

From an on chain adoption standpoint, STRC’s incremental value comes from composability. The STRCx ecosystem currently holds around $91.71 million in AUM. Within the Apyx ecosystem, apxUSD supply has reached approximately $476 million while apyUSD supply stands near $133 million. On Pendle, trading volumes for apxUSD, apyUSD, and sUSDat markets have already reached tens of millions of dollars. This demonstrates that STRC related cash flows are actively being transformed into stablecoins, yield bearing assets, and duration based yield products. For DeFi users, STRC’s appeal extends beyond its underlying yield of roughly 11%. It also comes from the additional capital efficiency generated through yield splitting, collateralized lending, and recursive leverage.

As a result, STRC’s allocation value lies in offering elevated yield compensation for investors capable of accepting its specific risk profile. The ideal investor is not a conservative cash management allocator, but rather a yield oriented participant who understands Strategy’s credit structure, BTC volatility dynamics, and DeFi composability risks. Investors seeking risk free dollar income would likely find STRC too risky. Investors willing to underwrite BTC treasury related credit exposure in exchange for materially higher cash flow than traditional credit assets, however, may find STRC worthy of serious research and allocation consideration.

5.2 Risk Boundaries: Credit, Volatility, Structural Mechanics, and DeFi Transmission

The first layer of STRC risk is credit risk. Although STRC ranks senior to common equity and certain junior preferred securities within the capital structure, it remains subordinate to corporate debt and higher ranking instruments such as STRF. Its distributions are also not contractual debt interest payments, but preferred dividends declared by the board and payable only when legally available funds exist. While Strategy currently maintains substantial BTC reserves and USD reserves, STRC distributions ultimately depend on the company’s ongoing financing access, capital market windows, and balance sheet management capability. If financing conditions deteriorate, STRC prices would likely reflect credit concerns first through widening discounts.

The second layer of risk comes from BTC driven asset coverage compression. Earlier stress tests showed that with approximately $65.34 billion in BTC reserves against around $36 billion of combined debt and preferred obligations, current coverage stands near 1.82x. A 30% BTC decline would reduce coverage to roughly 1.27x. A 40% decline would compress it to around 1.09x. A 50% decline would reduce coverage to approximately 0.91x. This highlights how heavily STRC’s credit safety margin depends on BTC pricing. Moderate BTC volatility may be absorbed through balance sheet buffers, but severe drawdowns could rapidly alter the market’s risk pricing framework for STRC.

The third layer of risk relates to the effectiveness of the mechanism itself. STRC’s par value anchor depends on the issuer maintaining near $100 trading levels through dividend adjustments, redemption mechanisms, and issuance management. While this framework may function effectively under normal market conditions, it is not an unconditional guarantee. If investors conclude that dividend adjustments no longer adequately compensate for risk, or if concerns emerge around distribution sustainability, prices could deviate materially from par value. Redemption provisions cap upside premiums, but do not guarantee downside stability. Fundamental change repurchase rights provide event based protection, not day-to-day liquidity support.

The fourth layer of risk emerges from DeFi integration. Once tokenized STRC enters ecosystems such as Apyx, Saturn, Pendle, and Morpho, underlying credit exposure becomes increasingly repackaged and leveraged. Stablecoin users focus on redemption quality and reserve backing. Pendle users focus on discounted future yield expectations. Morpho users focus on collateral pricing and liquidation thresholds. If STRC discounts widen, the result could include simultaneous stablecoin reserve repricing, sharp PT and YT curve adjustments, collateral liquidations, and liquidity withdrawals across DeFi markets. The DeFi flywheel improves capital efficiency during expansionary conditions, but can amplify liquidity stress during downturns.

5.3 Scenario Analysis: STRC’s Upside Potential and Fragility

Under a bull market scenario, rising BTC prices expand Strategy’s BTC reserves, improve asset coverage ratios, and strengthen market confidence in refinancing capacity. STRC becomes more likely to trade near or slightly above par, while dividend rates may gradually decline. Demand for on chain STRCx and STRCon assets increases, and TVL across Apyx, Saturn, Pendle, and Morpho expands. In this environment, STRC returns are driven primarily by high distributions and modest par value recovery, while DeFi activity amplifies demand through yield splitting and collateral efficiency.

Under a base case scenario, BTC remains range bound while Strategy’s financing windows remain open without significant expansion. STRC continues trading at a modest discount, with yields remaining above traditional credit markets. DeFi demand persists, though ecosystem growth depends more on genuine liquidity and protocol adoption than on pure APY driven speculation. In this environment, STRC behaves primarily as a high yield credit asset valued based on cash flow and risk compensation.

Under a bear market scenario, BTC declines reduce the value of Strategy’s BTC reserves, pressure MSTR common equity valuations, and increase preferred financing costs. STRC discounts widen as markets demand higher yields, reducing the efficiency of new issuance. On chain, Pendle implied APYs may rise sharply, stablecoins may trade at discounts, collateral values may deteriorate, and DeFi TVL may contract. In this environment, STRC transitions from a yield allocation thesis into a credit risk management exercise, with markets focusing on asset coverage ratios, USD reserve strength, dividend continuity, and whether STRCx can continue trading close to par value.

Under a severe stress scenario, rapid BTC declines, widening STRC discounts, stablecoin redemptions, and cascading DeFi liquidations occur simultaneously. The key risk here is not simply falling asset prices, but synchronized repricing across multiple markets. Traditional finance markets widen STRC credit spreads. DeFi lending markets reduce collateral values. Pendle reprices future yields. Morpho and related protocols trigger liquidations. If on-chain liquidity becomes impaired during such an event, tokenized STRC assets could trade at materially wider discounts than native STRC itself, creating additional redemption friction and arbitrage dislocations.

5.4 Long Term Implications: From BTC Financing Instrument to Digital Credit Infrastructure

From Strategy’s perspective, STRC represents the standardization of a new BTC treasury financing module. Common equity serves high beta risk capital. Convertible bonds serve volatility and optionality driven capital. Debt serves traditional credit capital. STRC, meanwhile, targets yield oriented preferred equity investors. As long as markets continue accepting this structure, Strategy can diversify its financing stack beyond common equity, reduce reliance on any single funding source, and continue converting capital market inflows into BTC reserve expansion.

More importantly, STRC connects public company credit, BTC reserves, preferred equity cash flows, and DeFi yield infrastructure into a cross market credit architecture. Traditional finance provides the issuer, legal framework, and cash distributions. BTC reserves provide the asset narrative and credit foundation. DeFi protocols provide yield decomposition, collateral financing, and liquidity reuse. If this structure matures successfully, other BTC treasury companies or broader reserve based corporate structures may eventually issue similar instruments, creating an entirely new category of on chain credit assets.

From the perspective of the broader BTC yield ecosystem, STRC introduces an important new pathway. BTC itself remains non yield bearing, but corporate credit instruments built around BTC reserves can generate distributable cash flows, which can then enter DeFi through tokenization. Historically, BTCFi has relied heavily on lending markets, staking like wrappers, bridges, or structured products. STRC introduces a different model: a BTC linked yield layer generated through public company capital structures. It does not alter BTC’s non yield bearing nature, but instead transforms BTC reserves into financeable, distributable, and composable yield bearing assets through the balance sheet of a BTC treasury company.

Ultimately, any investment conclusion around STRC should remain measured. The instrument combines three major attractions: high yield, par value anchoring, and DeFi composability. At the same time, it carries three major risks: Strategy credit exposure, BTC volatility, and on-chain leverage dynamics. If STRC continues trading near $100 over the long term, distributions remain stable, on chain AUM grows steadily, and Pendle implied APYs remain reasonably aligned with underlying yields, the market would effectively be validating both its credit structure and DeFi expansion potential. If elevated APYs are driven primarily by short term incentives, weak liquidity, or recursive leverage while STRC discounts and DeFi lockup stress widen simultaneously, investors should be cautious of leverage driven prosperity disguised as sustainable yield.

The ultimate upside for STRC is becoming a foundational credit asset within the BTC yield ecosystem. Its greatest fragility is that the same flywheel driving expansion during favorable conditions could also become the mechanism through which risk propagates during periods of stress.

Source:

Gate Research is a comprehensive blockchain and cryptocurrency research platform that provides deep content for readers, including technical analysis, market insights, industry research, trend forecasting, and macroeconomic policy analysis. Disclaimer Investing in cryptocurrency markets involves high risk. Users are advised to conduct their own research and fully understand the nature of the assets and products before making any investment decisions. Gate is not responsible for any losses or damages arising from such decisions.