RWA (Real World Assets) are traditional financial assets—including bonds, stocks, and real estate—that are tokenized using blockchain technology, allowing them to be represented, traded, and circulated on-chain. This article begins with the core logic of TradFi (traditional finance), systematically examining how RWA depends on, connects to, and enhances the traditional financial system. It analyzes whether RWA will ultimately replace traditional finance or simply complement it, and identifies avenues for efficiency gains, the underlying reasons for institutional adoption, and the practical limitations and future convergence trends.

RWA (Real World Assets) refers to the process of tokenizing real-world financial assets—such as bonds, stocks, and real estate—using blockchain technology, enabling their representation and trading on-chain. This innovation is becoming a crucial bridge between Traditional Finance (TradFi) and on-chain finance (DeFi).

In recent years, as blockchain and the crypto ecosystem have matured, the rise of RWA has proven to be more than a technical novelty—it is a tangible step toward modernizing financial infrastructure. RWA redefines the liquidity, transparency, and compliance of traditional assets on-chain, fundamentally transforming settlement, custody, and investment practices in conventional markets.

This article provides an in-depth exploration of the following key topics: the definition of TradFi and its core operating logic; the reasons RWA must rely on the traditional financial system; the compliant process for bringing traditional assets on-chain; how RWA enhances and limits traditional finance; and future pathways for integrating on-chain finance with TradFi.

Introduction to RWA and TradFi

RWA (Real World Assets) and TradFi (Traditional Finance) represent two distinct models for asset organization and circulation—on-chain finance and traditional financial systems. These models are increasingly intersecting and integrating.

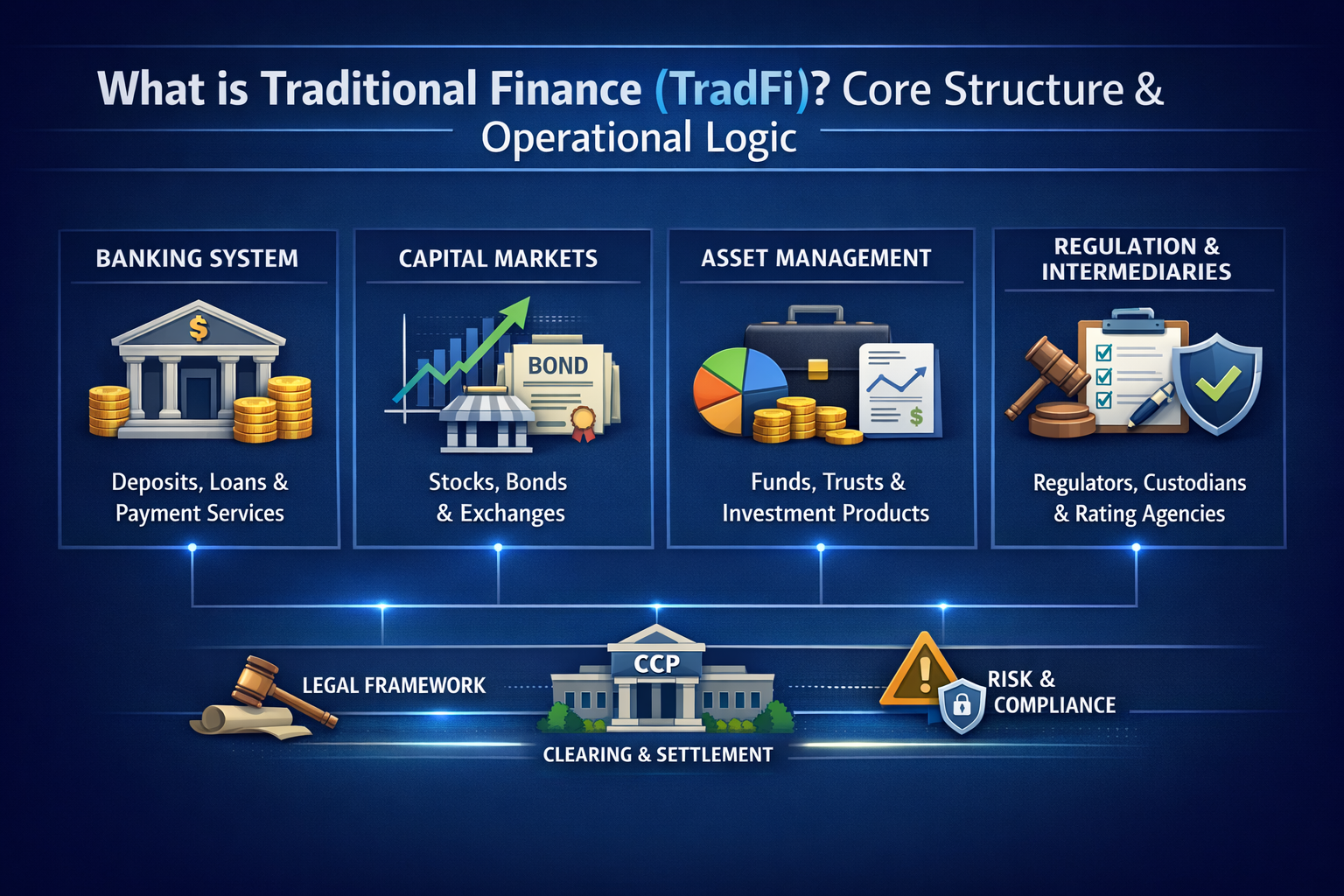

Traditional finance (TradFi) refers to the financial system built around banks, brokerages, asset management firms, and securities exchanges. Its core functions are capital intermediation, risk allocation, and payment clearing. TradFi forms the backbone of modern economic capital flows and serves as the institutional foundation for global asset issuance, trading, and custody.

Introduction to RWA and TradFi

The core structure of TradFi includes:

Banking System: Handles deposits, loans, and provides payment and settlement services;

Capital Markets: Facilitates financing and investment through securities like stocks and bonds, supported by exchanges, underwriters, and clearinghouses;

Asset Management Institutions: Pools investor capital through funds and trusts for professional management;

Regulatory and Intermediary Institutions: Encompasses regulators, rating agencies, and custodians, forming TradFi's compliance and risk control framework.

These institutions operate on mature legal systems, clearing networks, and central counterparty (CCP) mechanisms, usually with fixed business hours, tiered settlement structures, and relatively complex compliance processes.

In contrast, RWA uses blockchain technology to tokenize these traditional assets, allowing for higher-frequency circulation and programmable management on-chain. However, their legal status and value backing remain rooted in the TradFi framework.

Why RWA Must Rely on the Traditional Financial System

The core of RWA is mapping real-world assets onto the blockchain, meaning it must rely on TradFi infrastructure for value backing and compliance. The main reasons are:

Legal Nature of Assets and Proof of Ownership: Ownership and income rights for assets like stocks, bonds, and real estate are protected by law; on-chain code cannot substitute for the original legal framework;

Custody and Settlement Structures: RWA tokenization typically uses a special purpose vehicle (SPV) or custodian to hold underlying assets, requiring TradFi custody, audit, and accounting support;

Compliance and Regulatory Requirements: Issuance and trading of real-world assets must comply with KYC/AML and securities laws, all established and enforced by traditional regulators;

Market Participants and Infrastructure: Most sovereign bonds, fund shares, and similar assets are still issued and traded on TradFi exchanges and settlement systems.

Thus, RWA does not deconstruct assets from TradFi; instead, it brings blockchain technology into the legal and financial infrastructure of TradFi.

How RWA Connects with Banks, Brokerages, and Asset Management Institutions

To enable on-chain tokenization and trading of RWA, a connection layer between TradFi and blockchain must be established. This involves several cooperative models:

Bank Custody and Technology Integration: Banks act as custodians for underlying cash flows and bond assets, issuing representative tokens via smart contract platforms;

Brokerage and Trading Platform Integration: Brokerages can offer tokenized securities trading within a compliant framework, enabling interoperability between traditional securities and on-chain markets;

Digitalization of Asset Management Products: Asset managers digitize products like funds and bonds, issuing tradable tokens on blockchain while maintaining compliance structures.

This integration is not just a technical overlay—it requires standardized processes in legal, accounting, settlement, and compliance, ensuring on-chain transactions and traditional clearing systems can operate in sync.

How Traditional Assets Complete the Compliant On-Chain Process

How Traditional Assets Complete the Compliant On-Chain Process

Bringing traditional assets on-chain compliantly requires these key steps:

Legal Structure Design: Use SPV or trust structures to clarify the legal relationship between on-chain tokens and underlying asset rights;

Compliance Review: Ensure token issuance complies with local securities law, KYC/AML, and other regulatory requirements;

Custody and Audit: Custodians hold the original assets and undergo regular audits to ensure on-chain tokens match the underlying assets;

Oracle Data and Price Feeds: Trusted data sources securely transmit real-world asset valuations and status to smart contracts.

Due to different regulations across countries, this process often requires collaboration with regulatory sandboxes or specific frameworks.

Will RWA Disrupt TradFi or Serve as a Supplement?

There is no clear consensus in the industry on whether RWA will replace TradFi:

Supplementary View: Most believe RWA complements and upgrades TradFi, making assets easier to trade and fractionalize on-chain, boosting market efficiency without replacing existing legal and financial structures;

Integration Pathway: RWA tends to introduce blockchain technology within the existing financial framework, with TradFi entities and Web3 platforms jointly building infrastructure;

Not Full Disruption: Regulatory, legal, and market practice factors mean RWA is more likely to expand market boundaries than fully replace traditional market structures.

How RWA Improves Traditional Finance Efficiency

RWA enhances TradFi efficiency in several key areas:

Increased Liquidity: Tokenization breaks large assets into smaller, tradable units, attracting more investors;

Greater Transparency: On-chain transaction records are open to real-time auditing, reducing information asymmetry;

Global Market Access: Investors can trade across regions, 24/7, without being limited by traditional market hours.

However, these efficiency gains are still limited by regulation and infrastructure, and require real-world commercial adoption to prove their effectiveness.

Why Institutions Are Embracing the RWA Model

Financial institutions are adopting the RWA model for several reasons:

Boosting Capital Efficiency: Tokenization allows assets to be used as collateral, increasing capital utilization;

Innovative Products and Services: New product formats are emerging in asset management, securities issuance, and trading;

Attracting Younger Investors: The accessibility of on-chain markets attracts a broader investor base;

Building New Infrastructure: Laying the foundation for a more digital and automated financial ecosystem.

Challenges Facing TradFi and RWA’s Practical Limitations

Despite its promise, RWA still faces significant challenges in practice:

Regulatory Uncertainty: There is no unified global regulatory framework for RWA, and rules vary by jurisdiction;

Technical and Infrastructure Constraints: Cross-chain compatibility, oracle security, privacy protection, and lack of standardization are bottlenecks for RWA expansion;

Liquidity Shortfalls: The RWA market is still in its early stages, and many tokenized assets have limited secondary market liquidity;

Operational and Legal Integration Costs: The complexity and cost of compliant on-chain processes make widespread adoption more challenging.

Future Trends: Integration Paths for On-Chain and Traditional Finance

The integration of traditional and on-chain finance is likely to deepen in the following ways:

Hybrid Market Architecture: Connecting on-chain token trading with TradFi clearing systems, making them complementary rather than competitive;

Unified Regulatory Framework: International regulatory bodies may push for standards in on-chain asset regulation and cross-border collaboration;

Standardized Technology and Processes: Establishing cross-chain asset standards, oracle certification mechanisms, and privacy protocols as foundational infrastructure.

These trends will help RWA move from pilot projects to large-scale adoption, fostering collaborative innovation between TradFi and DeFi.

Conclusion

In summary, RWA is not a simple replacement for TradFi, but rather an upgrade and extension that brings on-chain technology to traditional financial foundations. This process balances compliance, custody, security, and efficiency, while unlocking new liquidity and market opportunities for traditional assets. TradFi and on-chain finance will continue to converge, driving the modernization and digital transformation of global financial markets.

Author: Max

Disclaimer

* The information is not intended to be and does not constitute financial advice or any other recommendation of any sort offered or endorsed by Gate.

* This article may not be reproduced, transmitted or copied without referencing Gate. Contravention is an infringement of Copyright Act and may be subject to legal action.

Solana faces both opportunities and challenges in its development. Recently, severe network congestion has led to a high transaction failure rate and increased fees. Consequently, some have suggested using Layer 2 and appchain technologies to address this issue. This article explores the feasibility of this strategy.

Sui is a PoS L1 blockchain with a novel architecture whose object-centric model enables parallelization of transactions through verifier level scaling. In this research paper the unique features of the Sui blockchain will be introduced, the economic prospects of SUI tokens will be presented, and it will be explained how investors can learn about which dApps are driving the use of the chain through the Sui application campaign.

This article introduces the technical principles, framework, and applications of Zero-Knowledge (ZK) technology, covering aspects from privacy, identity (ID), decentralized exchanges (DEX), to oracles.

Tronscan is a blockchain explorer that goes beyond the basics, offering wallet management, token tracking, smart contract insights, and governance participation. By 2025, it has evolved with enhanced security features, expanded analytics, cross-chain integration, and improved mobile experience. The platform now includes advanced biometric authentication, real-time transaction monitoring, and a comprehensive DeFi dashboard. Developers benefit from AI-powered smart contract analysis and improved testing environments, while users enjoy a unified multi-chain portfolio view and gesture-based navigation on mobile devices.

Stablecoins were originally designed as dollar substitutes within exchanges, primarily used for asset pricing and trade settlement. As on-chain financial ecosystems have matured, their role has expanded beyond simple payments to include collateral assets, cross-chain liquidity mediums, and unified settlement units. In particular, as AI systems and automated agents begin to participate directly in economic activity, demand has risen sharply for programmable value units capable of instant settlement. This shift is pushing stablecoins toward the role of foundational financial infrastructure.