As of June 29, 2026, according to Gate market data, Bitcoin (BTC) continues to fluctuate below the psychological threshold of $60,000, with the trading range roughly between $59,000 and $60,000. Bitcoin's decline this year has exceeded 30%, halving from its all-time high of approximately $126,000 in October 2025.

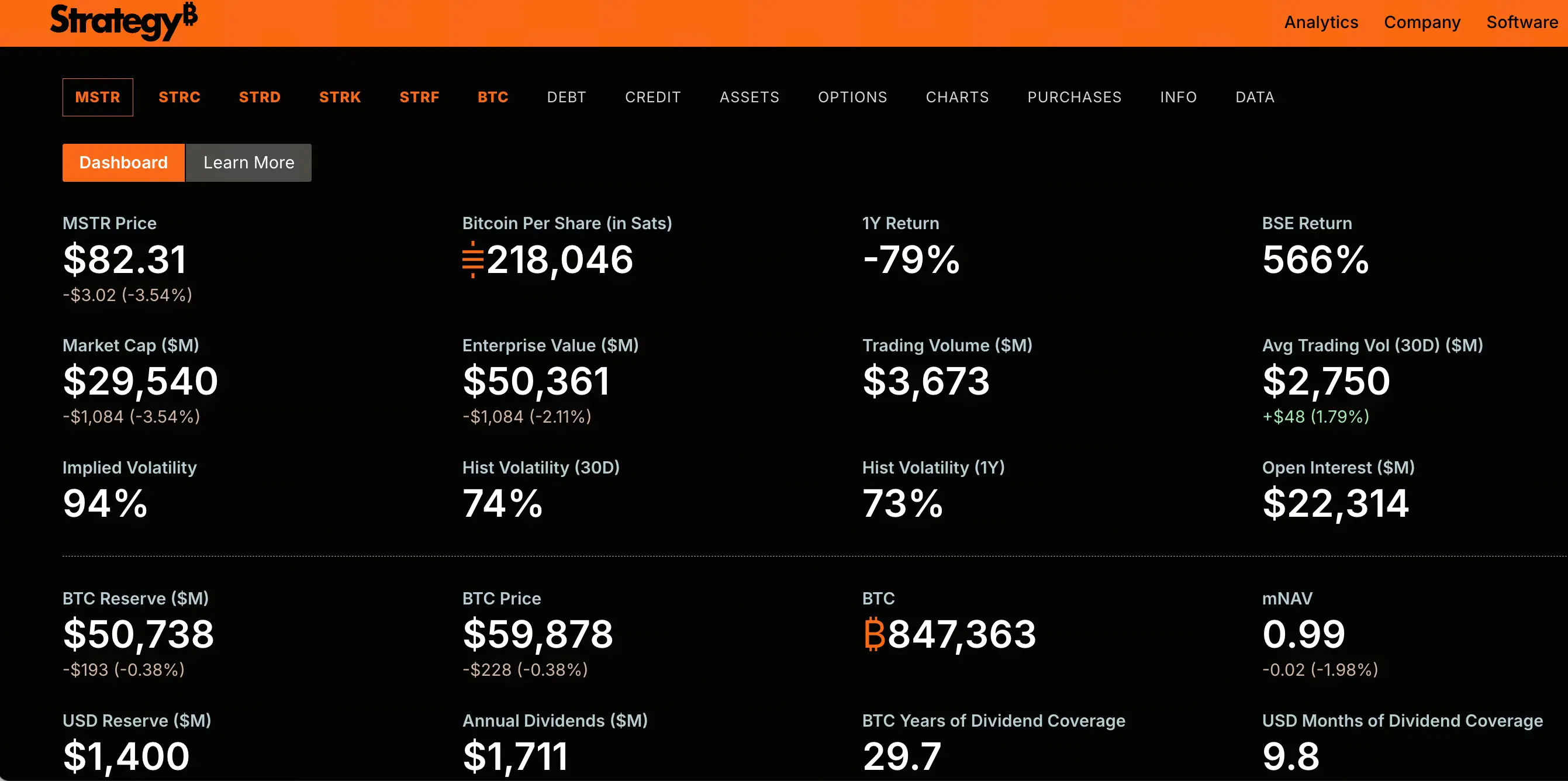

In the same time frame, Strategy (formerly MicroStrategy, ticker MSTR) has significantly underperformed Bitcoin. MSTR is currently at $82.3, down 45.7% in the past month, and has fallen approximately 82% from its all-time high of $457.22 in November 2024. Over $150 billion in market capitalization has evaporated.

MSTR's plunge is not a simple reflection of Bitcoin's decline. Bitcoin fell about 50% over the same period, while MSTR's decline was significantly amplified. The market is repricing the financial engineering that underpins Strategy's entire capital structure. When a stock positioned as a 'leveraged Bitcoin proxy' falls several times more than the underlying asset itself, the root cause must lie in the capital structure, not merely asset price fluctuations.

What Capital Structure Pressure Does the Preferred Stock De-pegging Reveal?

The most central pressure point in Strategy's capital structure is the floating-rate Series A perpetual preferred stock called STRC.

STRC is designed as a product anchored to a $100 par value, with Strategy dynamically adjusting the dividend rate to maintain its price around par. The essence of this design is to allow the company to continuously issue new STRC at near-par prices, thereby raising funds to accumulate more Bitcoin. STRC is considered Strategy's cheapest and most efficient financing channel.

However, this mechanism is failing. As of June 29, 2026, STRC has significantly de-pegged from its $100 par value, once hitting a historic low of $71.40, a discount of 28.6%. The de-pegging of STRC is not just simple price volatility but a direct manifestation of thoroughly shaken market confidence.

The de-pegging of STRC has directly cut off Strategy's most important financing channel. When secondary market investors can buy the same preferred stock for $75 or even less, no one will participate in a new issuance at nearly $100. The contraction of financing capacity means the core cycle of Strategy's continuous Bitcoin accumulation—'finance → buy coins → refinance → buy more coins'—is losing momentum.

Is There a Fatal Mismatch Between High Dividend Obligations and Cash Reserves?

STRC is not only a financing tool but also a continuously accumulating cash expenditure obligation.

As of now, the issuance scale of STRC has reached approximately $10.49 billion, with a current dividend rate of 11.5%, meaning STRC alone corresponds to over $1.2 billion in annual cash dividend payments. Adding other preferred stocks issued by Strategy such as STRD, STRK, STRF, etc., the total preferred stock scale reaches about $15.467 billion, with annual dividend obligations climbing to about $1.711 billion.

In comparison, Strategy's software business generated approximately $477 million in revenue in 2025. Dividend obligations are more than three times the software business revenue.

More critical is the cash reserve. According to the common stock issuance filing on June 21, Strategy disclosed a cash reserve of approximately $1.4 billion. Based on the current annual dividend payout of about $1.7 billion, the book cash can cover less than one year of preferred stock dividend payments. The dividend coverage ratio has shrunk sharply from over 7 years at the beginning of the year to just 14 months.

When a company needs to pay $1.7 billion in dividends annually, and its cash reserves can only support less than a year, the capital structure is in a highly strained state.

How Unrealized Losses on Bitcoin Holdings Amplify Financial Leverage

Strategy's balance sheet shows a typical leveraged structure. The company holds 847,363 Bitcoin, with a cumulative purchase cost of approximately $64.1 billion, and an average purchase price of about $75,650 per coin. Based on the current Bitcoin price of around $60,000, the market value of the holdings is about $50 to $51 billion, with an unrealized loss of approximately $12.6 to $14 billion.

The company's liability side consists of two layers: the first is about $6.714 billion in convertible bonds; the second is about $15.467 billion in perpetual preferred stocks. Total liabilities are about $22.2 billion.

From a static balance sheet perspective, as long as Bitcoin does not fall below about $26,000, the asset side (Bitcoin holdings plus cash) can theoretically cover liabilities. But this static calculation ignores two key variables: first, the annual $1.7 billion dividend payout will continuously consume cash; second, the early redemption or put rights in the terms of preferred stocks and convertible bonds may trigger concentrated repayment demands under certain conditions.

More importantly, there is a shift in market pricing logic. During the Bitcoin bull market, MSTR traded at a 3x premium over its Bitcoin holdings. But now, MSTR's market cap has fallen below the fair value of its Bitcoin holdings, and the mNAV (market cap to Bitcoin holdings market value ratio) has fallen below 1x. Not only has the premium disappeared, but the market has started to price the company at a discount.

The Formation Mechanism and Transmission Path of the Downward Spiral

To understand the possibility of a downward spiral, we need to start from the operating logic of Strategy's capital structure.

In an upward cycle, the mechanism is: Bitcoin rises → MSTR stock price rises (leveraged amplification) → mNAV premium expands → the company issues new shares or preferred stocks at a premium → raises funds to buy more Bitcoin → Bitcoin rises further. This is a positive reinforcement loop.

In a downward cycle, the same mechanism runs in reverse: Bitcoin falls → MSTR stock price falls (leveraged amplification) → mNAV premium shrinks or turns into discount → financing capacity contracts → dividend payment pressure increases → cash reserves deplete → market concerns intensify → stock price falls further.

Currently, this reverse cycle has entered a substantive phase. At the end of May, Strategy sold 32 Bitcoin for the first time since 2022 to cover preferred stock dividends. Although the sale was minimal (about $2.5 million), the 'never sell Bitcoin' narrative was broken, and its symbolic significance far outweighs the actual amount. The market is no longer asking whether Saylor will sell Bitcoin, but when he will sell on a large scale.

On June 21, Strategy sold 2.71 million shares of MSTR common stock, cashing out $335.5 million, but only spent $34.9 million to buy 520 Bitcoin, with the remaining approximately $300 million deposited into cash reserves to cover preferred stock interest payments. This means that most of the funds raised through the issuance of common stock were used to pay dividends rather than to accumulate Bitcoin—the financing 'flywheel' is slowing down.

How Short-selling Forces and Derivatives Markets Exacerbate Structural Pressure

MSTR's decline is no longer just a passive result of Bitcoin price fluctuations; its financial product attribute as a 'leveraged Bitcoin' is being precisely priced by the derivatives market.

Since the first Bitcoin reduction at the end of May, MSTR has fallen 48% cumulatively, hitting a two-year low. On-chain derivatives data shows that shorts are systematically positioning. One high-level short opened a short position on MSTR at $130.65 with 10x leverage, holding $2.4 million, with unrealized profit reaching $1.32 million. Despite the declining market, new short orders continue to enter.

Shorts are targeting not only Bitcoin's price but also the market's recalibration of valuation models after the 'never sell Bitcoin' narrative was broken. Once MSTR underperforms Bitcoin by another 10%, each ATM (at-the-market offering) will further dilute Bitcoin holdings per share, and the 'death spiral' feared by the market may truly begin.

Does the Fluctuation Pattern Below $60,000 for Bitcoin Pose Additional Risk?

Bitcoin's continued fluctuation below $60,000 provides the external environment for the above structural pressures.

The current Bitcoin price is at its lowest level since October 2024. U.S. spot Bitcoin ETFs continue to see large-scale outflows—on June 26, a single-day outflow of about $444.5 million, with cumulative outflows exceeding $4.4 billion over the past 13 trading days. Institutional redemptions directly suppress spot demand, and combined with some miners selling coins to cover operational costs, selling pressure persists.

On the macro level, expectations of Fed rate hikes continue to rise, the U.S. dollar remains strong, and global liquidity is tightening. Risk appetite decreases, with funds flowing to more stable assets like the U.S. dollar and gold.

For Strategy, every drop in Bitcoin below $60,000 further expands the unrealized losses on its holdings, compresses its mNAV multiple, and intensifies market doubts about the sustainability of its capital structure. Meanwhile, the contraction of financing capacity prevents it from 'buying the dip' to increase holdings at low prices as it did in past cycles—this is the most fundamental difference from previous cycles.

FAQ

Q1: What is the relationship between MSTR's plunge and Bitcoin's decline?

MSTR's plunge is not a simple reflection of Bitcoin's decline. Bitcoin fell about 50% over the same period, while MSTR fell about 82%, a significantly amplified decline. This is because MSTR is essentially a 'leveraged Bitcoin' vehicle—the company buys Bitcoin by issuing preferred shares and convertible bonds, and its capital structure amplifies the impact of Bitcoin price fluctuations on its stock price. The market is currently repricing the financial engineering that supports this capital structure, rather than just following Bitcoin's volatility.

Q2: What is STRC? Why is its de-pegging so important?

STRC is Strategy's floating-rate Series A perpetual preferred stock, the company's most core financing tool. It is designed to be anchored to a $100 par value, maintaining price stability through dynamic dividend rate adjustments, so that the company can continuously issue new shares at near-par prices to raise funds to buy Bitcoin. The de-pegging of STRC means this financing channel has been blocked—when the secondary market price is far below par, no one will participate in a new issuance at par. This poses a fundamental challenge to Strategy, which relies on continuous financing to sustain operations.

Q3: What exactly does 'downward spiral' refer to? Has it already occurred?

The downward spiral refers to the reverse reinforcement loop in Strategy's capital structure during a downturn: Bitcoin falls → MSTR stock price falls (leveraged amplification) → mNAV premium turns to discount → financing capacity contracts → dividend payment pressure increases → cash reserves deplete → market concerns intensify → stock price falls further. Currently, this cycle has entered a substantive phase—financing channels are ineffective, cash reserves are depleting rapidly, and mNAV has fallen below 1x—but it has not yet entered an irreversible spiral. The key variables are whether Bitcoin's price can recover to a level that alleviates capital structure pressure, and whether the company can regain financing capacity.

Q4: What is the current level of Strategy's financial situation?

As of June 2026, Strategy holds 847,363 Bitcoin, with a market value of approximately $50 billion to $51 billion, and unrealized losses of approximately $12.6 billion to $14 billion. The company's total preferred stock scale is approximately $15.467 billion, with annual dividend obligations of about $1.711 billion; convertible bonds are about $6.714 billion. Cash reserves are about $1.4 billion, sufficient to cover less than a year of preferred stock dividend payments. mNAV has fallen below 1x, meaning the total enterprise value is now lower than the market value of its Bitcoin holdings.

Q5: What price does Bitcoin need to return to in order to ease Strategy's pressure?

According to market analysis, Strategy's survival and capital structure sustainability are highly dependent on Bitcoin's price recovering to a level that can cover its leverage costs. Analysis suggests that Bitcoin needs to surpass $80,000 to offset the company's leverage costs. However, this threshold will change dynamically over time as dividend payments continue to consume resources. It should be noted that this is not a price prediction but a static projection based on the current capital structure.