Key Takeaways

- Overview of the Dual-Currency Investment Mechanism: Dual-currency investment is a structured product centered on “yield on held assets + conditional asset conversion.” Investors earn a fixed return during the lock-up period, while whether the principal is converted at maturity depends on whether the underlying price reaches a preset target level. In essence, the investor sells a short-dated option via the platform, with returns derived from the option premium. Dual-currency products exhibit behavior similar to option Greeks and represent a productized return structure combining “option premium income + compensation for principal lock-up.”

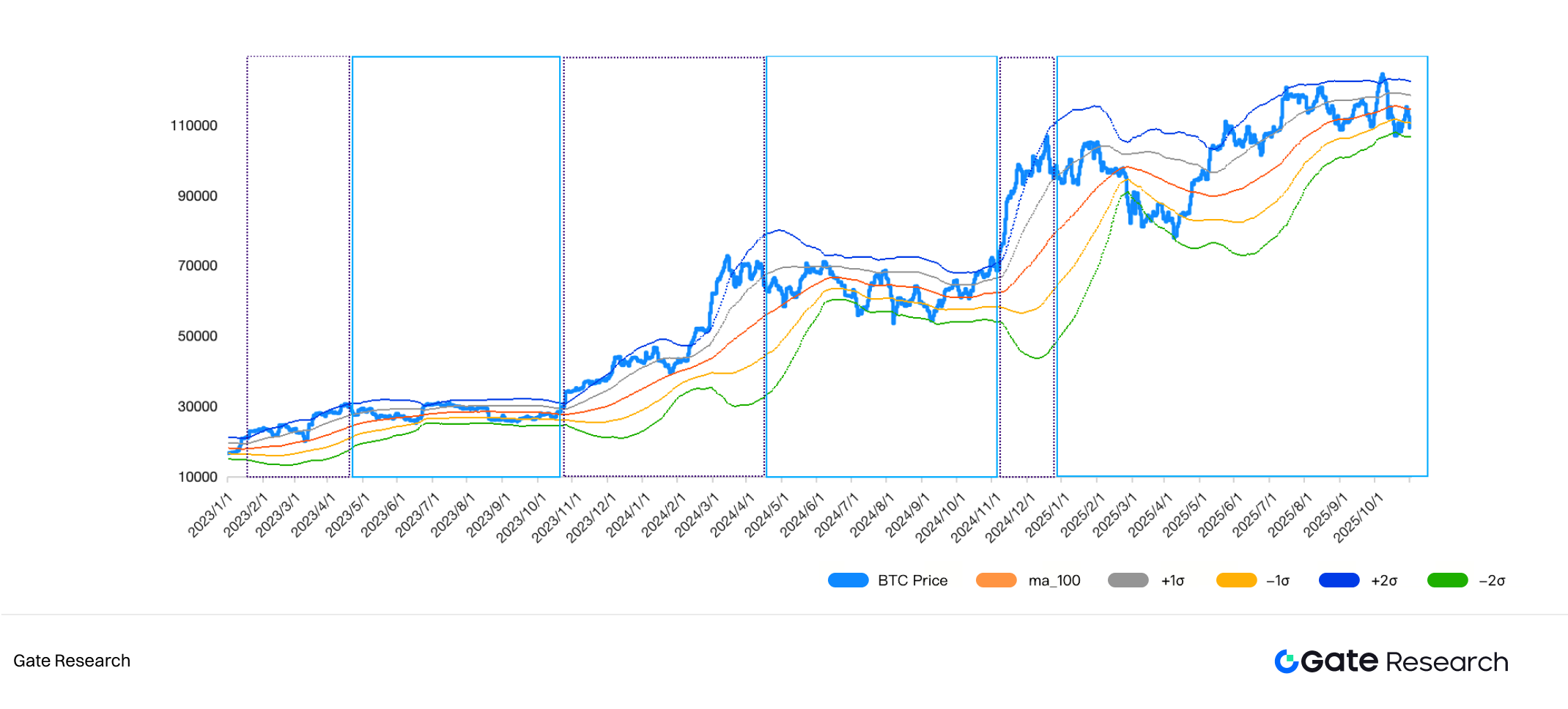

- Bitcoin Market Cycle Classification: Using technical indicators, the Bitcoin market is divided into bull, range-bound, and bear markets to characterize the risk–return profile of dual-currency investment as an option-selling strategy across different cycles. Specifically, MA100 along with its ±1σ and ±2σ rolling standard deviation bands are used for visualization. The results indicate that since 2023, the market has primarily remained in bull and range-bound phases, with no typical bear market observed.

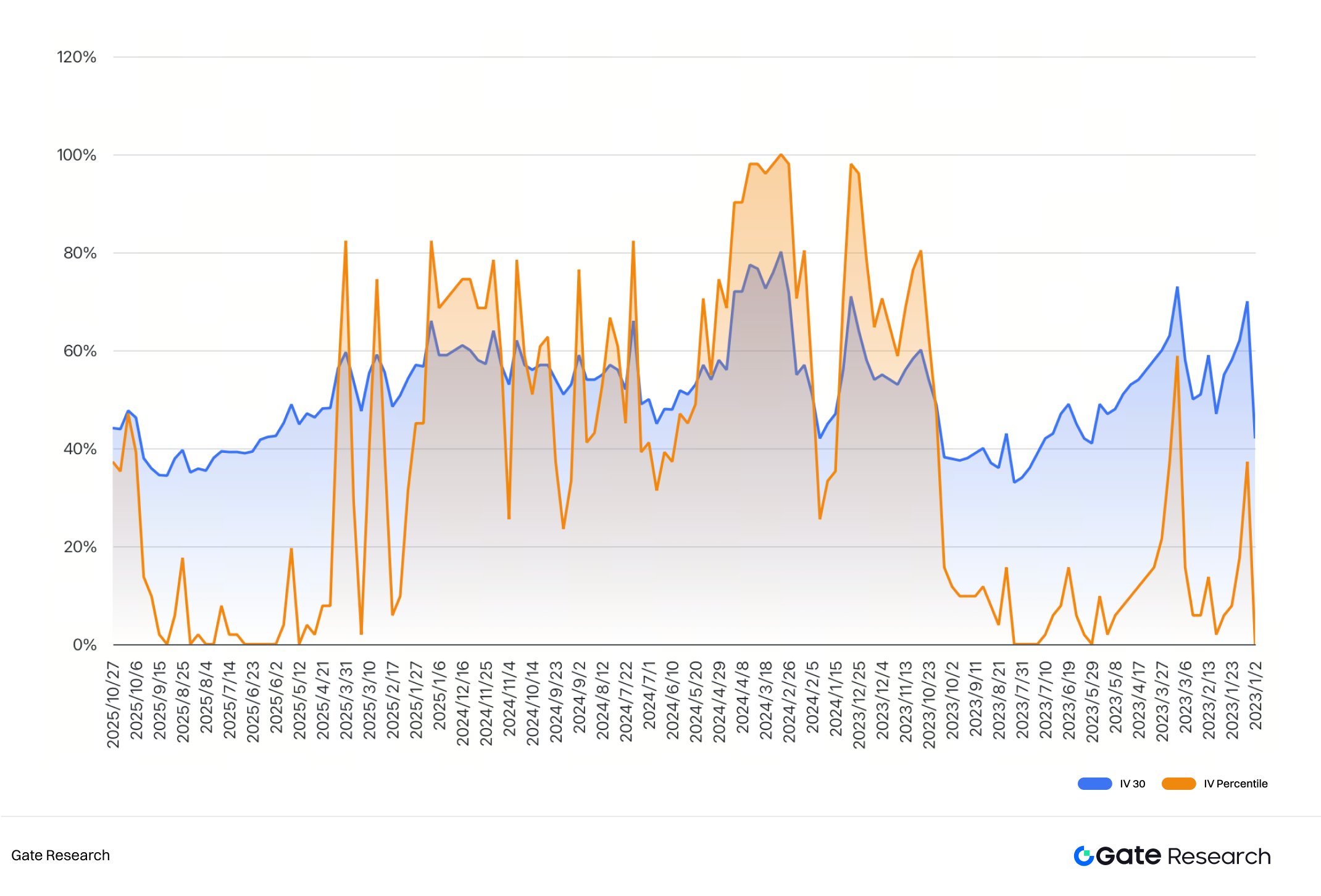

- Dual-Currency Investment Strategy Design: Entry timing for dual-currency investments should align with option pricing and volatility structure. “Sell High / Buy Low” corresponds respectively to Sell Call and Sell Put strategies, with the execution direction determined by market regime. The strategy uses elevated implied volatility as a unified entry signal: favoring sell-high positions toward the late stage of bull markets or during range-bound markets, and favoring buy-low positions during range-bound markets or toward the end of bear markets, thereby locking in higher option premiums during volatility expansions and improving overall return efficiency.

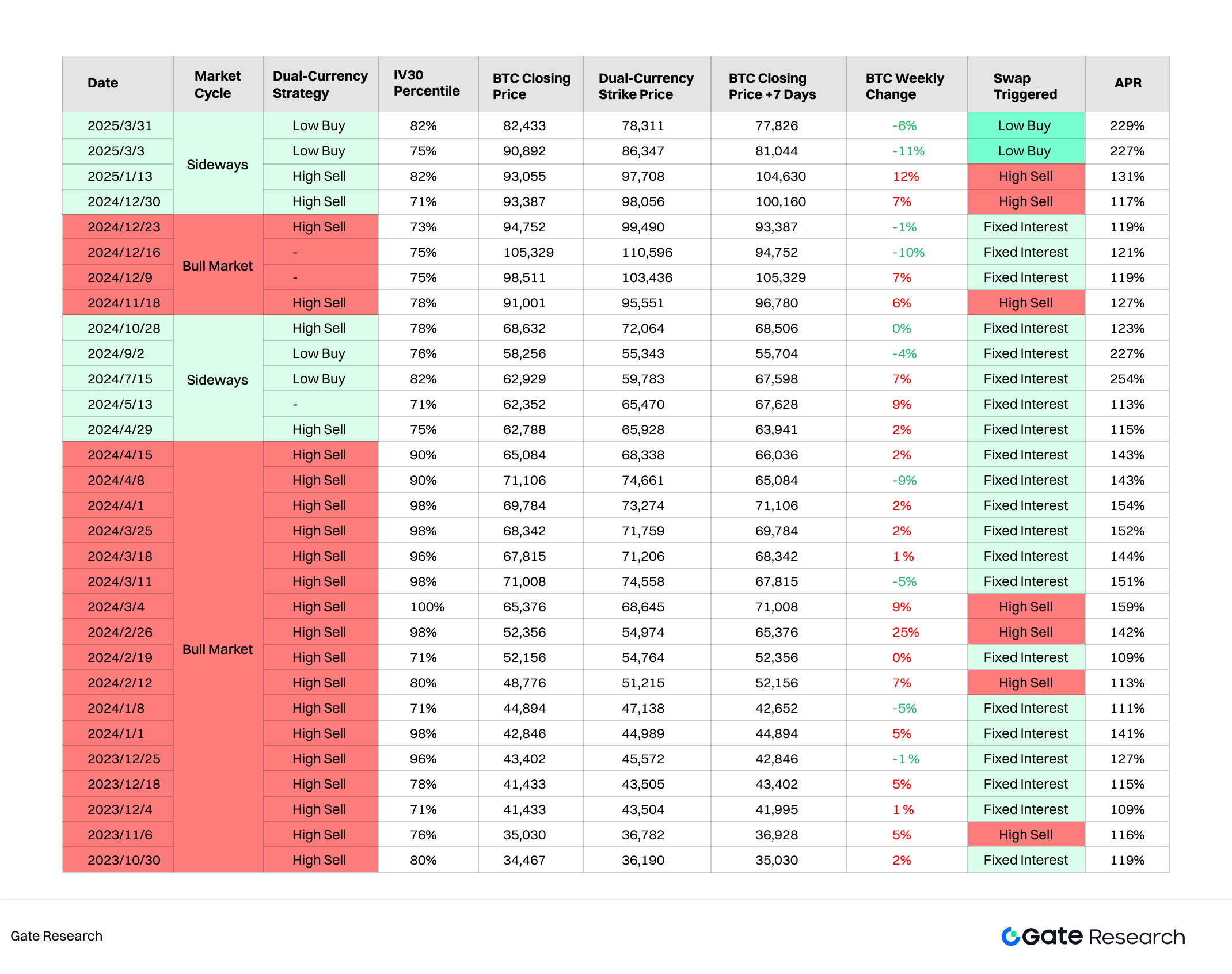

- Empirical Analysis: To validate the strategy, 7-day dual-currency “sell high / buy low” backtests are conducted during high-IV windows, incorporating market cycle classification and the MA100 ±2σ framework, with APR estimated using option pricing models. Results show that on high-volatility trading days, the strategy achieves APRs in the range of 109%–253% across bull and range-bound markets, confirming the effectiveness of the “IV-based entry + cycle-oriented positioning” approach, while also highlighting the need for more refined risk controls and parameter optimization in strongly trending markets.

(Click below to access the full report)Gate Research is a comprehensive blockchain and crypto research platform that provides readers with in-depth content, including technical analysis, hot insights, market reviews, industry research, trend forecasts, and macroeconomic policy analysis.

Disclaimer

Investing in the cryptocurrency market involves high risk. Users are advised to conduct independent research and fully understand the nature of the assets and products before making any investment decisions. Gate is not responsible for any losses or damages arising from such investment decisions.

Author: Akane

Reviewer(s): Ember, Shirley, Puffy, Kieran

Disclaimer

* The information is not intended to be and does not constitute financial advice or any other recommendation of any sort offered or endorsed by Gate.

* This article may not be reproduced, transmitted or copied without referencing Gate. Contravention is an infringement of Copyright Act and may be subject to legal action.