Author: David Hoffman

Translation: Jiahui, ChainCatcher

There is a “good coin” dilemma in the crypto space.

Most tokens are garbage.

Most tokens are not treated with the same seriousness as equity by the teams, neither legally nor strategically. Since historically teams have never given tokens the same respect as equity companies, the market naturally reflects this in token prices.

Today I want to share two sets of data that have made me somewhat optimistic about the state of tokens in 2026 and beyond:

MegaETH KPI Plan

Cap’s Stablecoin Airdrop (Stabledrop)

Conditioning Token Supply

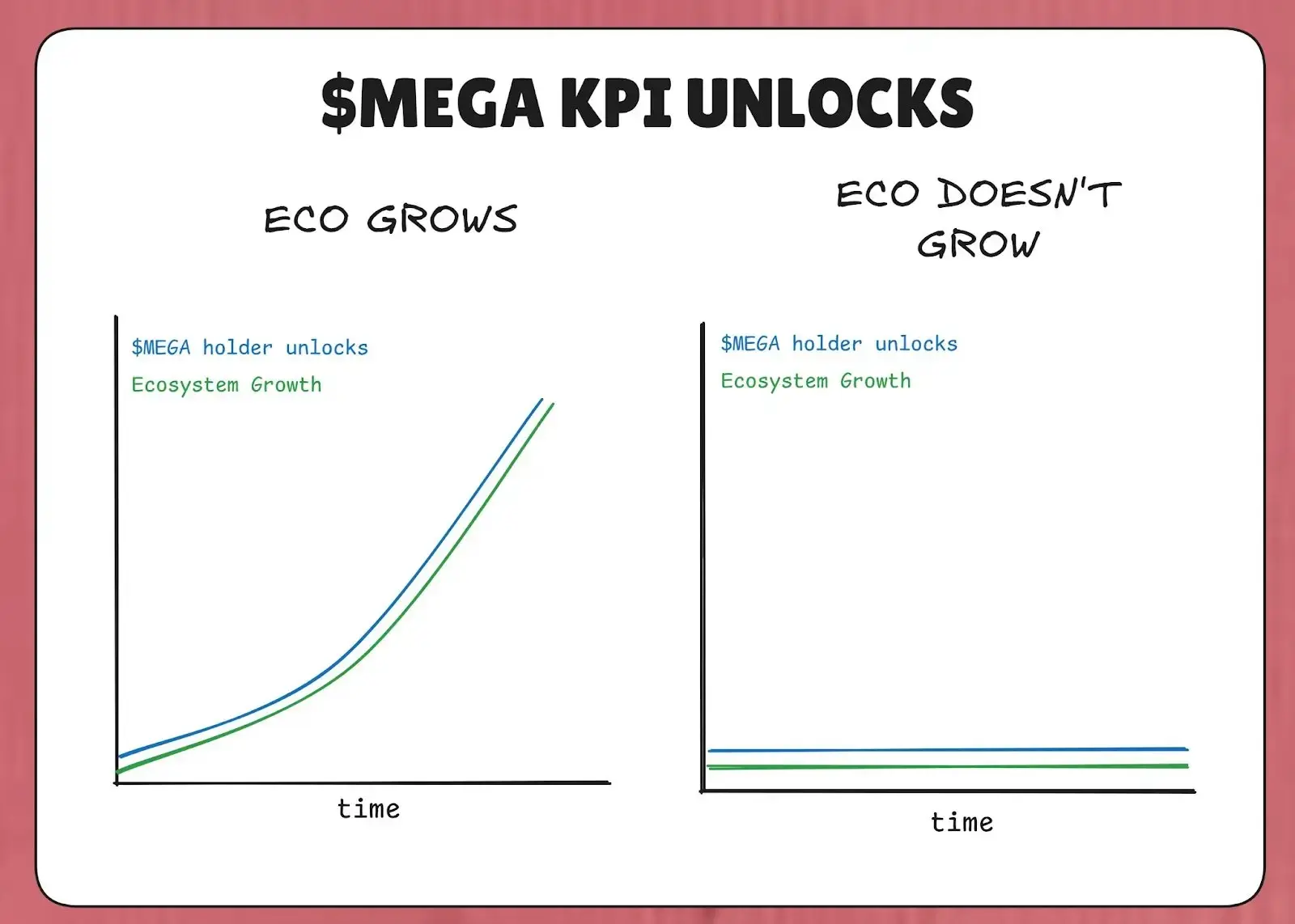

MegaETH has locked 53% of the total MEGA token supply behind a “KPI plan.” The core idea is: if MegaETH does not meet their KPIs [Key Performance Indicators], these tokens will not be unlocked.

Therefore, in a bear market with no ecosystem growth, at least no additional tokens will flow into the market and dilute holders. Only when the MegaETH ecosystem truly achieves growth (as defined by KPIs) will MEGA tokens enter the market.

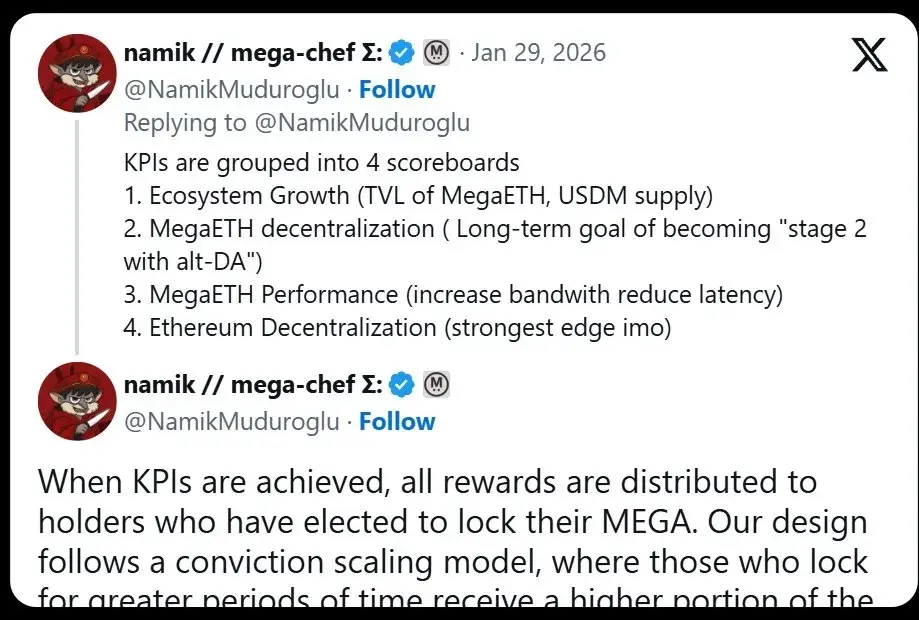

The KPI plan is divided into four scoring boards:

-

Ecosystem Growth (TVL, USDM supply)

-

MegaETH Decentralization (progress in L2Beat stage)

-

MegaETH Performance (IBRL)

-

Ethereum Decentralization

In theory, as MegaETH achieves its KPI targets, the value of MegaETH should increase accordingly, buffering the negative price impact of MEGA dilution on the market.

This strategy feels very much like Tesla’s compensation philosophy for Elon Musk—“only deliver results to earn rewards.” In 2018, Tesla granted Musk a stock-based compensation package, divided into several tranches, only vested if Tesla met continuously rising market cap and revenue targets. Elon Musk only earns $TSLA when Tesla’s revenue increases and its market cap grows.

MegaETH is trying to transplant some of that logic into their tokenomics. “More supply” is not a given—it’s a right that the protocol must earn by truly scoring on meaningful KPIs.

Unlike Musk’s Tesla benchmark, I don’t see any KPI related to MEGA market cap in Namik’s targets—perhaps for legal reasons. But as an investor in the public offering of MEGA, this KPI is definitely interesting to me.

Who Gets the New Supply Matters

Another interesting aspect of this KPI plan is which investors will receive MEGA when KPIs are met. According to Namik’s tweets, those who unlock MEGA are the ones who stake MEGA into lock-up contracts.

Those who lock more MEGA and for longer periods will gain the right to access 53% of the MEGA tokens entering the market.

The logic behind this is simple: distribute MEGA dilution to those who have already proven to be MEGA holders and are interested in holding more MEGA—that is, those least likely to sell their MEGA.

Balancing Incentives

It’s worth emphasizing that this also introduces risks. We’ve seen similar structures cause serious issues in the past. See this excerpt from Cobie’s article: “ApeCoin and the Death of Staking”

If you are a token pessimist, a crypto nihilist, or just a bearish trader, this alignment of interests is what you worry about.

Setting token dilution after the achievement of KPIs that should reflect the growth of the MegaETH ecosystem is much better than any ordinary staking mechanism we saw during the yield farming era of 2020-2022. Back then, tokens would be issued regardless of whether the team made fundamental progress or the ecosystem grew.

So, ultimately, MEGA’s dilution is:

This does not guarantee that MEGA’s value will rise—markets do what markets do. But it’s an honest and effective attempt to fix what appears to be a core flaw affecting the entire crypto token industry.

Treat Your Tokens Like Equity

Historically, teams have “shotgun” distributed their tokens across the ecosystem. Airdrops, farming rewards, grants—if they are truly valuable, teams wouldn’t do these activities.

Because teams distribute tokens as if they are worthless governance tokens, the market prices them as worthless governance tokens.

You can also see this same moral principle in MegaETH’s approach to CEX (centralized exchange) listings, especially when Binance opened MEGA futures on its platform (which was Binance’s attempt to extort the team for tokens).

I hope teams become more selective about token distribution. If teams start treating their tokens as treasures, perhaps the market will respond in kind.

Cap’s “Stablecoin” Airdrop

Instead of traditional airdrops, stablecoin protocol Cap launched a “Stabledrop.” They did not airdrop their native governance token CAP but instead distributed their native stablecoin cUSD to users who farmed with Cap points.

This method rewards genuine value to farming users, fulfilling their social contract. Users who deposit USDC into Cap’s supply contract bear smart contract risk and opportunity cost, and the stablecoin airdrop compensates them accordingly.

For those who want CAP itself, Cap is conducting token sales via Uniswap CCA. Anyone seeking CAP tokens must be a genuine investor and put in real capital.

Filtering Steadfast Holders

The combination of stablecoin airdrops and token sales filters for committed holders. Traditional CAP airdrops might go to speculative flippers who might sell immediately. By requiring capital investment through token sales, Cap ensures CAP flows to those willing to bear full downside risk for upside potential—more likely to hold long-term.

Theoretically, this structure builds a base of concentrated holders aligned with the protocol’s long-term vision, increasing the likelihood of success, rather than relying on an imprecise airdrop mechanism that hands tokens to those only interested in short-term profits.

Token Design Is Maturing

Protocols are becoming smarter and more precise in their token distribution mechanisms. No more shotgun, spray-and-pray token emissions—MegaETH and Cap are highly selective about who receives their tokens.

“Optimized distribution” is no longer popular—perhaps a legacy of the Gensler era (former SEC Chair known for tough crypto regulation). Instead, these teams are optimizing for concentration to build a stronger holder base.

I hope that as more applications launch by 2026, they observe and learn from some of these strategies, even improve upon them, so that the “good coin” problem ceases to be a problem, leaving us only with “good coins.”