Nvidia's earnings report day drops 7%! JPMorgan sets a $265 target price, but the market is not buying it

NVIDIA’s Q4 earnings surpassed expectations, with revenue reaching $68.1 billion and earnings per share of $1.62. The guidance for the first quarter even projected revenue of $78 billion. Morgan Stanley immediately raised its target price from $250 to $265. However, on February 26, NVIDIA’s stock price sharply declined nearly 7% to below $185, with fund flow data and technical indicators both indicating market caution regarding this earnings cycle.

Hidden Cracks in the Earnings Figures: Slowing Growth Momentum

While NVIDIA’s annual growth figures appear impressive on the surface, the quarterly growth trajectory reveals different signals:

Q3 Quarterly Growth: 22%

Q4 Quarterly Growth: 19.5% (adjusted after earnings release)

Q1 FY2027 Guidance Implied Quarterly Growth: approximately 14.5%

For a tech stock whose valuation is primarily supported by growth momentum, three consecutive quarters of decelerating quarterly growth pose a direct challenge to forward-looking pricing by institutional investors.

Another key risk is customer concentration. Gene Munster of Deepwater Asset Management estimates that about 70% of NVIDIA’s revenue comes from just eight companies; CFO Colette Kress confirmed that the top five large-scale data center providers account for slightly over 50% of data center revenue. If a few major clients cut AI capital expenditures by 10-15%, quarterly revenue could decline by billions of dollars.

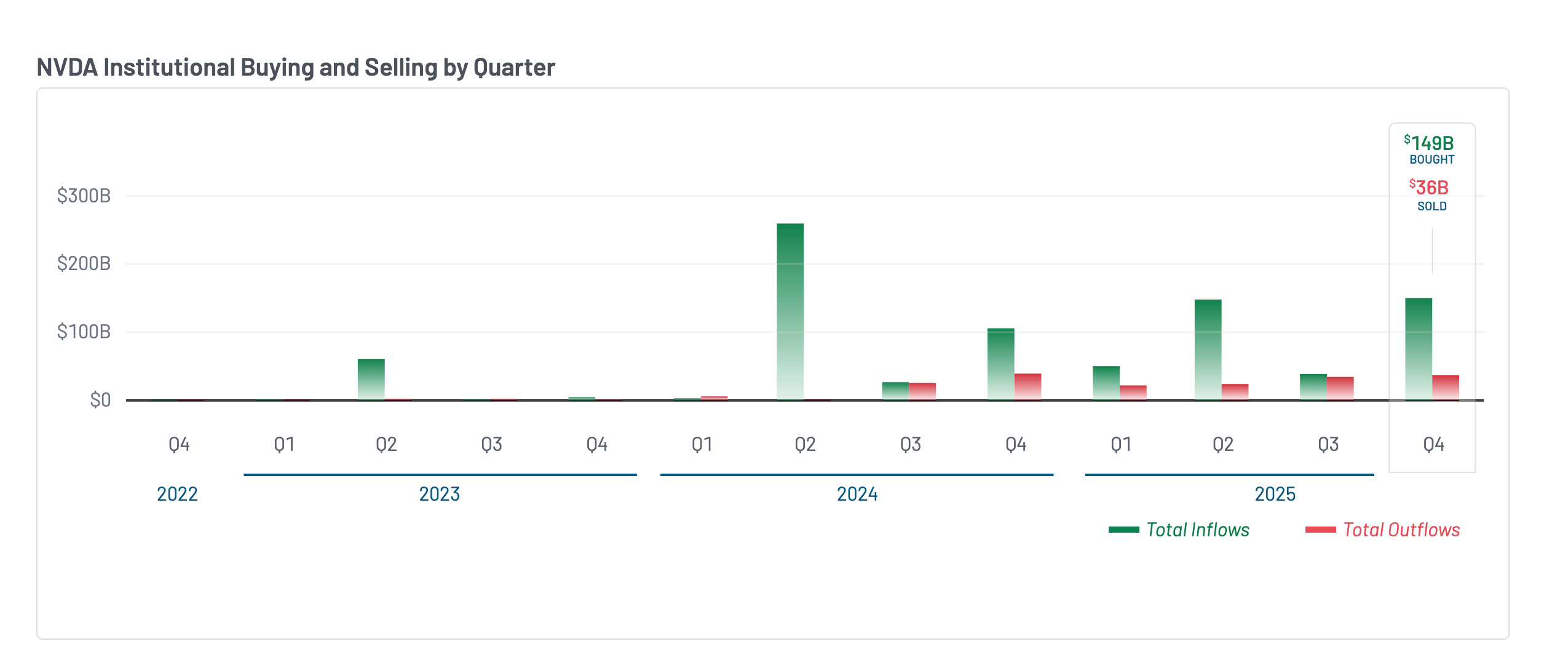

Contradictory Signals from Institutional Funds: Heavy Buying but No Stock Price Rise

(Source: Market Beat)

According to 13F filings, institutional net buying of NVIDIA surged in Q4 2025: approximately $149 billion purchased, $36 billion sold, resulting in a net inflow of about $113 billion—far exceeding the mere $4 billion net inflow in Q3. Despite such substantial institutional inflows, NVIDIA’s stock price remained nearly flat throughout the quarter, showing no clear upward trend.

This phenomenon suggests early insiders and initial shareholders may have been selling. NVIDIA director Mark Stevens sold about $40 million worth of stock in December; Bank of America slightly increased its holdings but also fully closed its long and short options positions, removing directional bets.

Notably, Morgan Stanley’s asset management division is also a significant institutional shareholder of NVIDIA. This is standard Wall Street practice, but retail investors should consider this connection when interpreting the bullish sentiment behind the target price upgrade.

Technical Analysis: Hidden Bearish Divergence and Failed Break of $195

(Source: TradingView)

On the daily chart, from November 10, 2025, to February 25, 2026, NVIDIA formed a “hidden bearish divergence”: the stock made lower highs, but the Relative Strength Index (RSI) showed higher highs, indicating weakening upward momentum.

On February 25, NVIDIA attempted to break above the inverse head and shoulders neckline at $195, but the breakout failed within 24 hours, with the stock plunging to below $185, accompanied by a sharp collapse in the Chaikin Money Flow (CMF) indicator. Speculative funds quickly exited at the failed breakout, and the VWAP support also broke down.

Key technical levels now are: support at $183 (Fibonacci 0.5) and $180 (0.382). If these are broken, the stock could test the $170 low of the right shoulder and the $169 head pattern. To resume the upward path toward $226, $235, and Morgan Stanley’s target of $265, NVIDIA needs to effectively reclaim the $195 neckline.

FAQs

NVIDIA’s earnings are so strong, why did the stock drop 7%?

Market pricing reflects expectations for the future, not past performance. NVIDIA’s growth has slowed for several consecutive quarters (from 22% to a forward guidance of 14.5%), and high customer concentration introduces potential vulnerabilities, causing doubts about sustainable valuation. The post-earnings decline is often seen as a “sell the news” reaction—meaning the good news was already priced in, and the actual announcement triggered profit-taking.

Is Morgan Stanley’s $265 target price a conflict of interest?

Morgan Stanley’s asset management division is itself a major institutional holder of NVIDIA. While their target price increase is not technically illegal, retail investors should be aware of the “firewall” between research analysts and the asset management side, as well as the potential interests of the holding institutions.

Is NVIDIA’s inventory buildup similar to Cisco in 2000?

Investor Michael Burry points out that NVIDIA’s current supply commitments are comparable to Cisco’s levels before the dot-com bubble burst. CFO Kress also admits inventory locking is “more extended than before.” However, there are fundamental differences: AI infrastructure demand is driven by growing compute-intensive workloads, whereas the 2000s enterprise network equipment bubble was fueled by systemic demand overstatement. Whether a Cisco-style collapse can recur depends on whether major large-scale clients significantly cut AI capital expenditures.