TeraWulf's annual revenue increased by 20%, while AI transformation losses surged 9 times to $660 million

TeraWulf, a Bitcoin miner listed on NASDAQ, announced its financial forecast for 2025 on Thursday, projecting total revenue of $168.5 million, up 20.3% year-over-year, including $16.9 million from its newly launched high-performance computing (HPC) leasing business. However, the company’s net loss sharply widened from $72.4 million in 2024 to $661.4 million, an increase of over nine times.

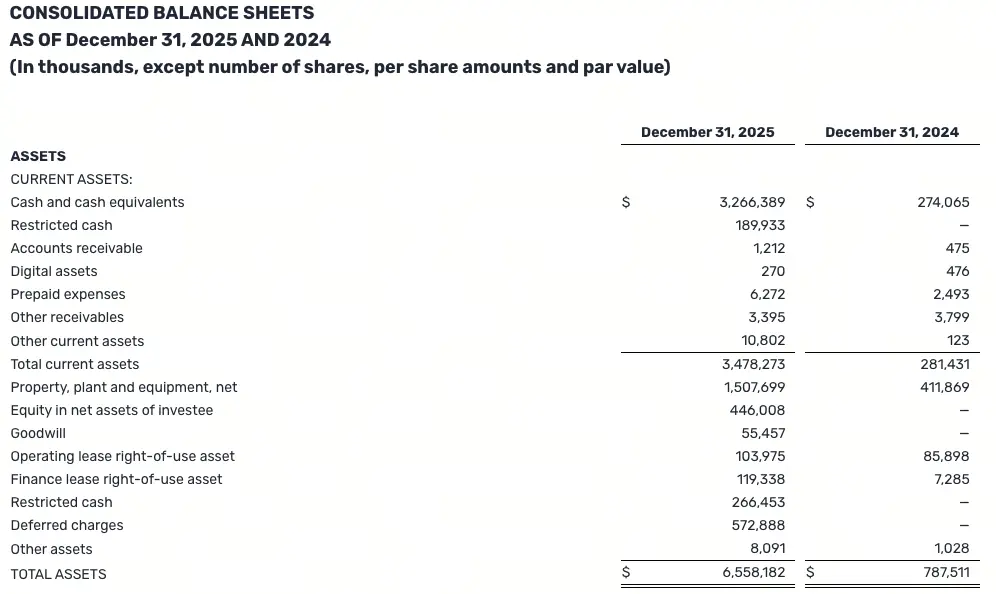

2025 Financial Performance: Revenue Growth and Significant Losses

(Source: TeraWulf)

(Source: TeraWulf)

TeraWulf’s 2025 financial data reflects typical capital investment characteristics of a transitional period: top-line revenue grew 20% driven by both mining operations and the new HPC business, but bottom-line profit was heavily impacted by substantial infrastructure construction investments.

Quarterly comparisons reveal the specific path of transformation:

Digital Asset Revenue: Decreased from $43.4 million in Q3 to $26.1 million in Q4, with the company citing “mainly due to a decline in Bitcoin production and prices in Q4.”

HPC Leasing Revenue: Increased from $7.2 million in Q3 to $9.7 million in Q4, indicating continued growth of the new business line.

Long-term Contract Scale: Long-term data center leasing agreements covering 522 MW of critical IT load, with total customer revenue exceeding $12.8 billion.

Related Financing Scale: Financing related to HPC platform construction reached $6.5 billion.

CEO Paul Prager stated in the earnings release: “Entering 2026, we have 522 MW of HPC contract capacity and a multi-region platform with a total installed capacity of 2.9 GW, aimed at long-term expansion. We will continue to focus on disciplined execution, transparent capital allocation, and transforming energy advantage infrastructure into sustainable long-term cash flow.”

AI Transformation Strategy: Multi-GW Platform and Brownfield Expansion

TeraWulf’s core strategic focus is increasingly directed toward long-term AI and cloud computing clients, primarily serving two key campuses: Lake Mariner in New York and Abernathy HPC in Texas.

Earlier this month, TeraWulf further announced the acquisition of brownfield infrastructure land in Kentucky and Maryland, adding approximately 1.5 GW of potential capacity to its overall asset portfolio. After this acquisition, the company’s multi-region platform total capacity has reached 2.9 GW, laying a hardware foundation for large-scale AI computing infrastructure needs.

This transformation reflects a common trend among U.S. Bitcoin miners seeking more stable cash flow sources amid increasing cryptocurrency market volatility. Meanwhile, Mara Holdings announced a net loss of $1.7 billion in Q4 and revealed a joint venture with Starwood Capital Group to jointly develop AI-focused data centers.

TeraWulf’s stock closed Thursday down 0.22% at $17.88, with a cumulative increase of 29.66% over the past month.

Frequently Asked Questions

Why did TeraWulf’s net loss sharply increase from $72.4 million to $661.4 million?

The significant increase in net loss mainly stems from large capital investments required for HPC and AI infrastructure transformation, including $6.5 billion in related financing and pre-construction costs for multi-region data centers. During this transition period, a large amount of one-time and non-cash expenses (such as depreciation, amortization, and financing costs) are reflected on the income statement, making the loss figures substantially higher than the previous year.

How does HPC leasing business compare to traditional Bitcoin mining in terms of long-term value for TeraWulf?

Bitcoin mining revenue is highly correlated with Bitcoin prices and hash rate competition, leading to volatile cash flows. HPC leasing typically involves long-term contracts (5-15 years), providing more stable and predictable cash flows. If the over $12.8 billion in long-term customer contracts can be fulfilled as planned, it will significantly improve the company’s cash flow predictability and reduce dependence on cryptocurrency market cycles.

Where does TeraWulf’s 2.9 GW capacity stand in the industry?

A 2.9 GW multi-region platform enables TeraWulf to compete effectively in meeting large-scale AI compute demands from hyperscaler cloud clients. The demand for power capacity in AI data centers continues to grow rapidly, and low-cost, scalable power infrastructure is becoming a core competitive threshold for AI infrastructure investments. This is an area where TeraWulf, along with other Bitcoin miners, has a relative advantage.