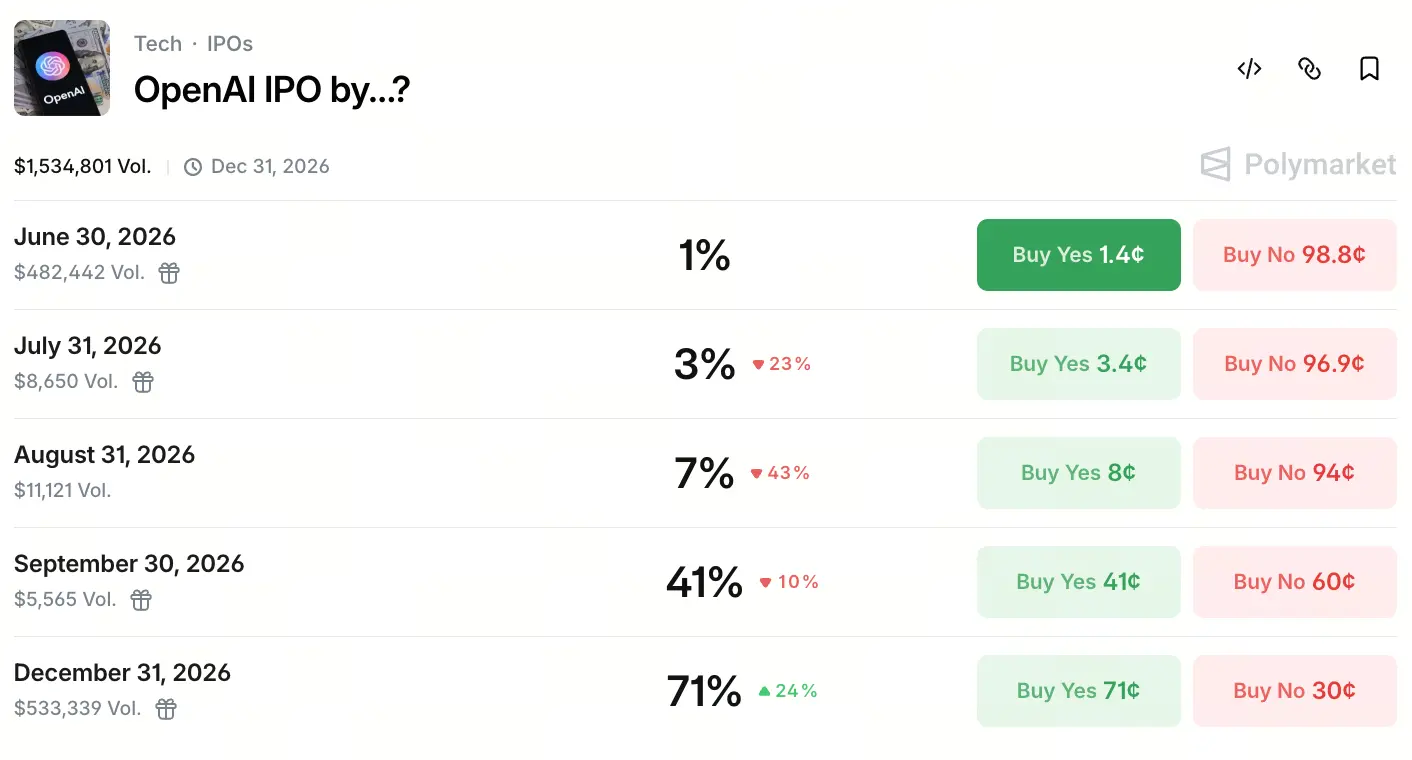

As of May 22, 2026, contracts on the prediction platform Polymarket for “When will OpenAI conduct its IPO?” have become a hot prediction topic, with total trading volume exceeding $1.5 million. Market funds are significantly prefer the Q4 window: the probability of listing before September 30 is 41%, while the probability of listing before December 31 rises to 71%.

Click to participate in the prediction

This expectation did not come out of nowhere. In mid-May, SpaceX officially filed its IPO registration statement, with a market value target of about $1.75 trillion, greatly fueling market expectations for the AI giant’s listing timeline. On the same day, multiple media outlets disclosed that OpenAI is working with Goldman Sachs and Morgan Stanley, with plans to secretly submit a draft registration statement to the SEC as early as May 22, aiming to be in a position to list in September 2026. While no official SEC announcement has been made as of the time this article was written, the involvement of investment banks has already led the market to perceive tangible progress.

Prediction markets generally believe the odds of trading being listed in official in 2026 Q4 are higher. CNBC cited data from the Kalshi platform showing that traders believe the probability of OpenAI filing for an IPO this year is as high as 92%. This data strongly echoes Polymarket’s year-end expectations.

Forced IPO: Capital logic and cash-flow pressure in the AI arms race

OpenAI’s push toward an IPO is rooted in the fact that its massive capital expenditures have outgrown what the private markets can bear. In court testimony revealed by Greg Brockman, OpenAI’s cofounder and president, OpenAI’s IPO is not fundamentally a cash-out exit after the company matures; it’s because capital expenditures for AI training and inference are too large, private markets are no longer enough, and ultimately the public market must take over the funding.

Financial data validates this view. In Q1 2026, OpenAI generated revenue of about $5.7 billion, but its adjusted operating margin was only -122%, meaning the company loses $1.22 for every $1 of revenue. In the first half of 2025, the company’s net loss reached $13.5 billion, with R&D costs as the main expense—$6.7 billion—mainly used to develop new AI models and to run infrastructure such as the servers required for ChatGPT.

In terms of burn rate, the company’s cumulative fundraising has already exceeded $180 billion. OpenAI’s monthly revenue has climbed to $2 billion, with revenue growth rates 4x those of Alphabet and Meta over the same period. But higher growth comes with greater capital consumption: with continued investment in server expansion, large-model iteration, and enterprise infrastructure, the marginal impact of private-market financing is diminishing, making the public market the only remaining outlet for capital replenishment.

Transition from non-profit to for-profit: OpenAI’s governance restructuring battle and IPO qualification

The institutional cost of OpenAI’s transition from a non-profit lab to a for-profit entity is the most unique structural obstacle on its IPO path. Since starting in 2015 as a non-profit organization, OpenAI’s governance model has been led primarily by a non-profit board, with the main beneficiaries defined as “all of humanity” rather than investors.

To meet listing and regulatory requirements of public markets such as NASDAQ, OpenAI has been discussing major restructuring plans internally. Reports say the company is considering adopting a for-profit holding company structure similar to Alphabet (Google’s parent company), planning to split its robotics and hardware divisions into independent businesses to simplify the IPO process for its core AI business.

On the equity governance front, a suspected leaked capitalization table shows Microsoft holds about 26.79%, the OpenAI Foundation holds 25.8%, SoftBank holds about 11.66%, and current and former employees combined hold about 20%. CEO Sam Altman still does not directly hold OpenAI equity, which is a structural variable that still needs further clarification within governance expectations. Despite external doubts about its governance mechanism, internal efforts are further advancing governance optimization through moving toward “public-company” operations—just as CFO Sarah Friar said, “Companies like OpenAI need to be more like a public company in terms of governance and external image.”

Can a trillion-dollar valuation be delivered? The tug-of-war between revenue, user stagnation, and a deep-loss pit

Despite high expectations for the IPO, OpenAI’s fundamentals still show significant imbalance, and there has always been doubt in the market about whether a trillion-dollar valuation can actually be realized.

On the revenue side, OpenAI’s revenue in Q1 is about $5.7 billion, and the full year is expected to stay around $30 billion. The company expects that by 2030, advertising alone could contribute about $102 billion in revenue. On the user side, ChatGPT’s weekly active users have reached 905 million, but growth appears to be stalling, failing to break the 1 billion active users target. Enterprise-side revenue share has already exceeded 40%, and it is expected that by the end of 2026 it will match the scale of the consumer side. API processing volume exceeds 15 billion tokens per minute, and progress on the commercialization infrastructure side appears relatively stable.

But the scale of losses is the biggest threat. Based on current profit margins, for every $5.7 billion of revenue generated, the company needs to incur about $6.95 billion in losses. If it cannot significantly improve its profit model before listing, investor-relations pressure in the public market will likely persist long term. In the first half of 2025, cash burn reached $2.5 billion, with R&D expenses becoming the largest expense category. For institutional investors seeking stable EBITDA and EPS evaluation, this deep-loss structural condition becomes an important valuation discount factor.

Valuation slashed and secondaries go cold: investors’ real sentiment and divergence

While IPO expectations are running high, OpenAI’s performance in the secondary market shows a clear contrast. After closing a $122 billion fundraising round in March this year, the official valuation was pushed to $852 billion, but secondary-market buy-side interest is significantly lower than in previous periods.

According to media reports, about $600 million worth of OpenAI shares in the secondary market faces pressure from insufficient buy-side demand. Even though the transaction price already shows about a 10% discount versus the official valuation, buyers’ psychological price targets have been further lowered. Goldman Sachs and Morgan Stanley have even launched zero-commission promotional schemes to attract investors.

In stark contrast, competitor Anthropic is seeing a “premium scramble” situation in the secondary market—subscription orders have repeatedly surpassed $1.6 billion, with large numbers of investors bidding at a premium. Secondary-market valuation has been raised to $600 billion, nearly 50% higher than the valuation from the previous round of financing.

This divergence—“official valuations holding firm vs. secondary-market cool reception”—reveals the core institutional concern about the sustainability of the profit model. Worries in the investment community mainly center on a few areas: OpenAI’s capital expenditures for AI infrastructure are too high; the speed of its transition on the enterprise side is slower than the market expects; and in the face of Anthropic’s stable-growth enterprise customer structure and an expanding profit space, competitive pressure from rivals may continue to intensify.

Racing to open the listing window: competitive pressure from Anthropic’s synchronized push

The biggest variable in the 2026 AI IPO competition comes from Anthropic’s simultaneous listing tempo.

Anthropic not only surpasses OpenAI in secondary-market popularity, but is also actively preparing to apply for a NASDAQ listing in the second half of 2026. It has rapidly risen in the enterprise AI and AI programming markets, with its enterprise customer base exceeding 300,000. According to recent reports, Anthropic’s valuation is about $380 billion, and it is negotiating a new funding round, with the target valuation expected to reach $900 billion.

In the prediction markets around “who lists first” for the IPO, market views have shifted significantly. Before reports about OpenAI’s listing timeline were released, traders believed the probability of OpenAI getting there first was only about 32%. After the news came out, the Kalshi platform’s market-implied probability that OpenAI would list earlier jumped to 83%. Over the same period, Polymarket cut the probability of “Anthropic listing before OpenAI” from 69% to 20%.

However, whether this race channel can be smoothly opened still depends on uncertain factors such as the pace of regulatory review, internal restructuring timing, and remaining litigation risks. But the signal is already clear—when the listing windows of these two leading companies overlap, it means that 2026 Q4 will become the most concentrated IPO window in the AI sector in history.

Meaning of AI company listings for the digital asset market

For the Crypto market, the listing tempo of top AI companies like OpenAI forms an important signal value.

First, an IPO wave means the traditional financial system has provided systematic institutional recognition of AI as a digital sector that highly relies on compute power and data-center infrastructure. Once companies like SpaceX and OpenAI enter the Nasdaq core index constituent sequence, capital is expected to flow more systematically into Crypto tracks such as AI tokenization, compute-power rental RWA (Real World Assets), and DePIN (decentralized physical infrastructure networks). OpenAI itself does not directly issue tokens, but the demonstration effect of its listing will push more AI infrastructure projects toward blockchain-based RWA designs.

Second, prediction-market platforms such as Polymarket have expanded the application boundary of the Crypto industry through active trading around OpenAI’s IPO timeline. Stable liquidity for contracts predicting listing probabilities provides crypto users with a data-driven entry point for betting. The total trading volume breaking through the $1.5 million scale is not accidental—it reflects the Crypto industry’s ability to participate in mainstream technology narratives.

Third, after an AI titan with market value in the range of $852 billion to $1 trillion completes its listing, its weight in the economic system will force the Crypto market to establish a new valuation coordinate system that anchors the AI track. Projects directly related to AI compute, allocation of computing resources, and AI data markets and other infrastructure will gain clearer and more direct macro reference benchmarks.

FAQ

Q1: Will OpenAI be listed in 2026 for sure?

Not formally confirmed yet. Although media reports say OpenAI has been working with Goldman Sachs and Morgan Stanley to prepare draft IPO filings targeting September 2026 for listing eligibility, as of now the SEC has not received any publicly disclosed formal documents. The prediction market Polymarket shows a probability of about 71% to complete the IPO by the end of 2026, but the specific timing may still be subject to adjustment.

Q2: What is OpenAI’s IPO valuation roughly?

The latest official financing round (March 2026) has a post-money valuation of $852 billion. Market rumors put the target valuation for listing in the range of $1 trillion to $1.25 trillion. Polymarket user data shows a probability of about 65% that OpenAI would close above $1.4 trillion at the end of its first day of public trading.

Q3: Can OpenAI’s financials support an IPO?

Pros and cons. In 2026 Q1, revenue is about $5.7 billion, but the operating margin is -122%, still placing it in a state of deep losses. Net loss in the first half of 2025 reached $13.5 billion. However, the company’s revenue growth rate is 4x that of Alphabet and Meta over the same period; monthly revenue is already close to $2 billion, implying substantial structural growth potential.

Q4: Will Anthropic list before OpenAI?

The likelihood has dropped significantly. After the news that OpenAI plans to file IPO documents quickly was released in mid-May, the Polymarket probability of “Anthropic listing first” fell sharply from 69% to 20%. Currently, the market broadly expects OpenAI to be relatively ahead in the competition for the IPO window.

Q5: What impact will OpenAI’s IPO have on the Crypto market?

Mainly three impacts: first, it will push traditional capital to systematically allocate to the AI infrastructure track, benefiting Crypto projects such as compute-power RWA and DePIN; second, prediction market applications such as Polymarket will accelerate the expansion of ecosystem boundaries through these popular IPO contracts; third, once the AI giant completes its listing, it will provide a reference for the overall valuation framework of the AI track, indirectly affecting valuation logic for projects in the Crypto market related to AI, compute resources, and data-infrastructure.