Is Bitcoin's Scarcity Dead? Crypto Industry Executives Respond: Derivatives Do Not Mint New Coins

Market analysis reports claim that the emergence of cash-settled futures, ETFs, and other financial derivatives has effectively turned Bitcoin’s supply cap of 21 million coins into a “theoretically infinite” supply. However, many industry leaders and researchers in the cryptocurrency space state that derivatives markets will not alter the underlying on-chain supply structure of Bitcoin, and the 21 million hard cap remains unchanged.

Core Argument of the Kendall Report

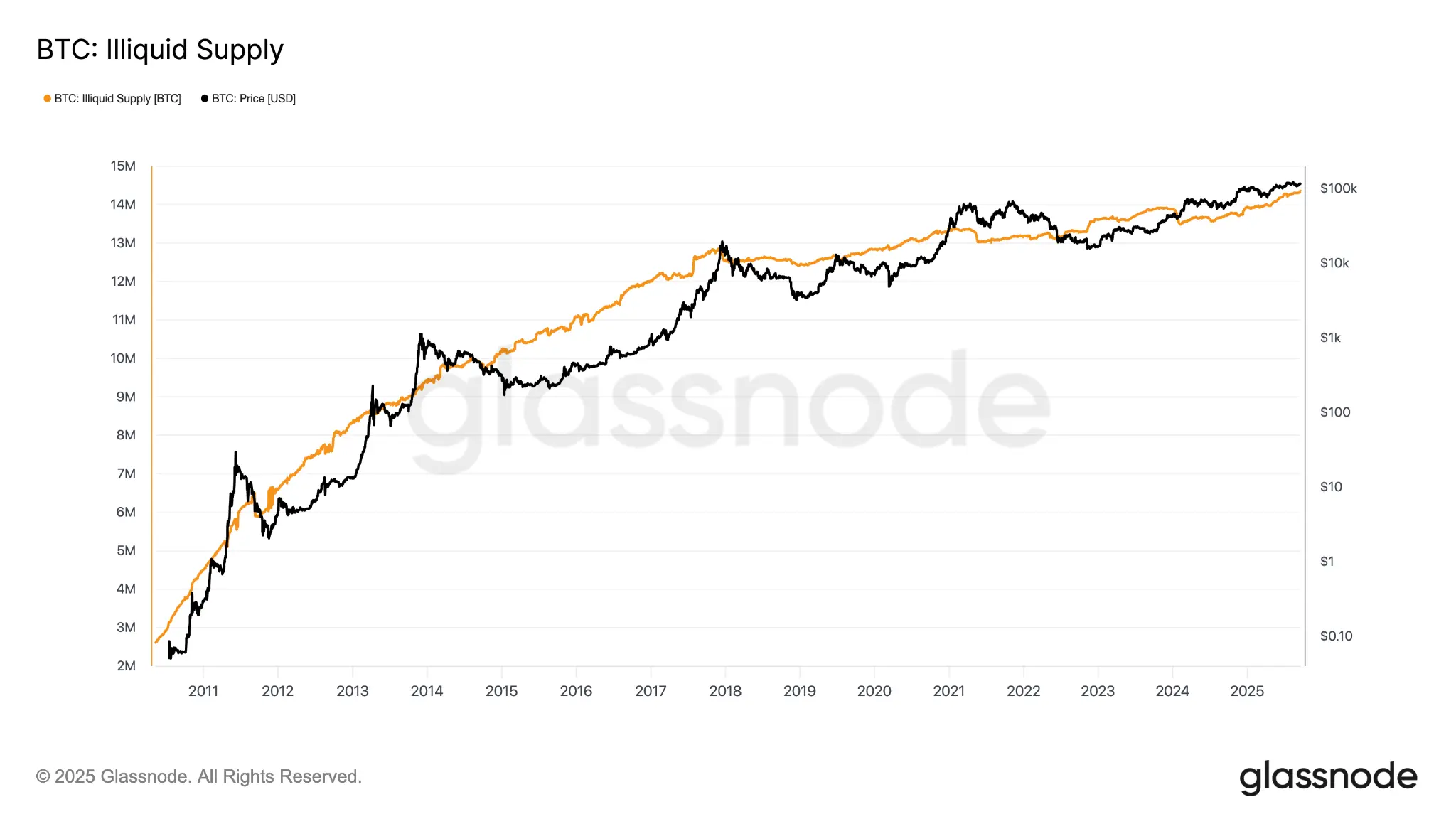

(Source: Glassnode)

The author of this analysis, Robert Kendall, believes that once cash-settled derivatives are layered on top of Bitcoin assets, the valuation logic based on fixed supply “fails.” His main point is that the emergence of paper Bitcoin markets creates large financial exposure without actual Bitcoin holdings, thereby diluting the scarcity narrative at the marginal pricing level.

Kendall later clarified that his intention was not to say derivatives “eliminate scarcity from the blockchain,” but rather that they change the “marginal price setting position.” However, this clarification was only viewed approximately 3,000 times, compared to the original post’s 5 million views, leading to widespread misunderstandings due to information asymmetry.

Industry Leaders’ Rebuttal: Three Core Points

(Source: Trading View)

Harriet Browning, Vice President of Sales at institutional staking company Twinstake, states: “When institutions allocate through ETFs and Digital Asset Custody (DAT), they do not dilute scarcity because the total Bitcoin supply remains at 21 million. They are not minting new Bitcoin but are transferring Bitcoin to long-term institutional holders.”

CoinShares senior researcher Luke Nolan counters with an analogy to gold: “The paper market for gold is huge, far exceeding physical supply, but no one denies gold’s scarcity. The paper holdings do not change the amount of gold underground, and the same logic applies to Bitcoin.”

Nolan further points out that spot ETFs require physical Bitcoin custody, and with ETF and corporate treasury holdings increasing significantly in 2025, actual market supply is effectively being removed. As of September last year, on-chain illiquid Bitcoin supply reached 14.3 million, accounting for over 71% of the total mined.

Nima Beni, founder of crypto leasing platform BitLease, also states: “The view that synthetic investments will eliminate scarcity is like mistakenly applying the paper gold analogy from commodity markets here — it was wrong in the past, and it remains wrong now.”

What Exactly Have Derivatives Changed: The Shift in Bitcoin Price Discovery Mechanism

Even critics of Kendall’s supply theory generally agree on one fact: Bitcoin’s short-term price discovery heavily depends on derivatives markets. Browning points out that derivatives influence Bitcoin’s spot price through three main channels:

CME Futures Dominating Institutional Pricing: Institutional traders express their views in the futures market before acting in the spot market; when futures and spot prices diverge with futures premium, hedge funds engage in basis trading (buying spot ETFs and shorting CME futures) to profit.

Banks Creating Indirect Demand via Structured Products: Banks issue Bitcoin-linked notes to clients, using ETF purchases to hedge risk, creating additional spot buying pressure.

Perpetual Contract Funding Rate Arbitrage: Positive funding rates drive traders to buy spot Bitcoin and sell futures to earn the rate; when rates turn negative, capital flows reverse, exerting downward pressure on prices.

Browning concludes: “The spot market is increasingly playing the role of settlement and inventory layer, while derivatives are increasingly dominant in price discovery.”

Frequently Asked Questions

Will Bitcoin derivatives markets break through the 21 million supply cap?

No. The 21 million hard cap is embedded in the protocol code; no derivatives, ETFs, or structured products can create additional Bitcoin on-chain beyond this limit. The existence of derivatives only affects how Bitcoin is held and priced, not the underlying blockchain supply structure.

What is the actual impact of paper Bitcoin markets on ordinary holders?

Paper markets (futures, ETFs, structured products) mainly influence short-term price volatility and market liquidity. For long-term holders, increased volatility is the primary impact, while institutional holdings of physical Bitcoin via ETFs effectively reduce circulating supply, which is theoretically beneficial for long-term holders.

Why is the illiquid supply of Bitcoin as high as 71%?

According to Glassnode data, a large portion of Bitcoin is held long-term and locked away from daily trading; additionally, an estimated 4 million coins have been lost due to lost private keys. This makes the actual circulating supply much less than the 19.99 million mined, further emphasizing Bitcoin’s scarcity as an asset.

Related Articles

Trump's State of the Union address did not mention Bitcoin and cryptocurrencies, and the market's expectations were disappointed, causing intense price volatility.

Bitcoin Depot Requires ID for Every Crypto ATM Transaction

Bitcoin may decline for the fifth consecutive month. What should be the next focus?

Peter Schiff warns that Trump's State of the Union address could trigger a "sell-off," increasing the risk of a short-term pullback after Bitcoin's rally.

Missouri Advances Bill to Establish State Bitcoin Strategic Reserve