Brazil opens up for Bitcoin mining to utilize excess renewable energy

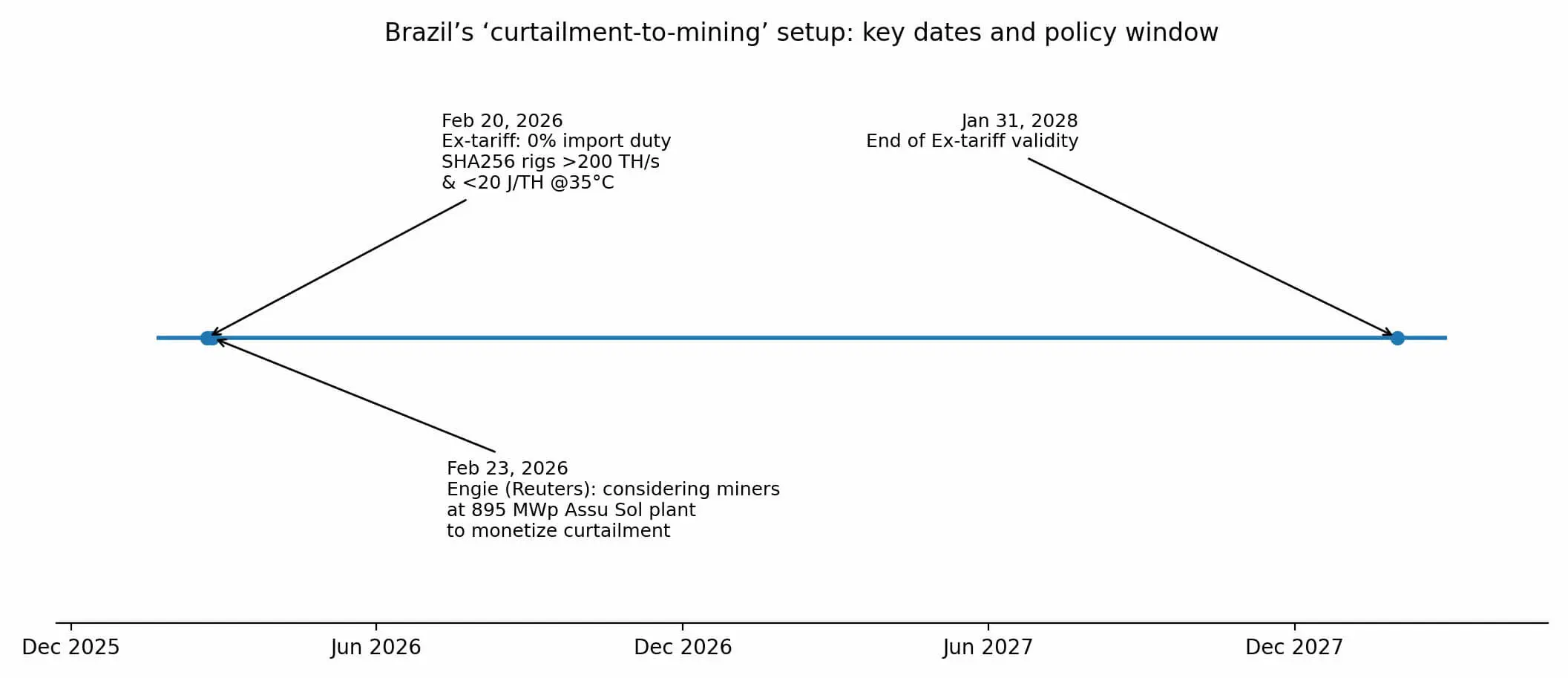

On February 20th, the Brazilian Foreign Trade Council issued a technical resolution reducing import tariffs to 0% for a very specific hardware group: SHA256 Bitcoin mining machines with a capacity over 200 terahash/second and energy efficiency below 20 joules/terahash.

Three days later, the French state-owned energy group Engie told Reuters they are considering installing Bitcoin miners at the Assu Sol plant, an 895 MW facility in northeastern Brazil—Brazil’s largest solar power plant—to leverage curtailment and improve financial efficiency.

These two developments within 72 hours reveal an overlooked point: Brazil is creating a “pressure release valve” for stranded renewable energy, and Bitcoin mining is the mechanism to unlock that wasted value.

This isn’t about Brazil “legalizing” mining or implementing a national strategy. Instead, it’s the silent convergence of three factors: prolonged renewable curtailment, declining hardware costs, and profit pressures at power plants. When these conditions align, the hash rate can gradually shift toward a previously overlooked market.

Curtailment – the structural challenge of renewable energy

From October 2021 to September 2025, Brazil’s wind power sector has had to cut approximately 32 TWh, resulting in an estimated revenue loss of about 6 billion reais (roughly $1.2 billion USD). Curtailment occurs when the grid cannot absorb all generation due to transmission limitations or supply-demand mismatches in time and region. For renewable generators, each MWh curtailed effectively erases its value.

In 2024, wind and solar accounted for 24% of Brazil’s total electricity; by August 2025, this share reached 34% for the first time. As the share of renewable energy grows faster than transmission capacity, bottlenecks and curtailment increase. In this context, plants need a flexible demand source that can quickly turn on/off to absorb excess electricity. Bitcoin mining fits this profile perfectly.

Brazil’s policy of zero import tariffs on high-performance mining hardware, lasting from February 2026 to January 2028, was announced just three days after the policy was enacted. Engie’s Assu Sol plant is located in the northeast—an area with high solar radiation but limited transmission infrastructure. Engie states that integrating Bitcoin mining or energy storage could help monetize curtailed electricity, though deployment may take years. Notably, this signal comes from a European state-owned energy company, viewing Bitcoin mining as a tool for industrial load balancing rather than crypto speculation.

Brazil’s policy of zero import tariffs on high-performance mining hardware, lasting from February 2026 to January 2028, was announced just three days after the policy was enacted. Engie’s Assu Sol plant is located in the northeast—an area with high solar radiation but limited transmission infrastructure. Engie states that integrating Bitcoin mining or energy storage could help monetize curtailed electricity, though deployment may take years. Notably, this signal comes from a European state-owned energy company, viewing Bitcoin mining as a tool for industrial load balancing rather than crypto speculation.

What does the tariff policy really change?

Resolution GECEX 861 amends Brazil’s ex-tariff list, reducing import duties to 0% for certain specialized information technology equipment. Appendix I adds a line for crypto mining servers using SHA256, with efficiency below 20 J/TH (measured at 35°C) and capacity over 200 TH/s. The 0% tariff is valid until January 31, 2028.

This doesn’t mean a blanket exemption for all mining rigs. The technical thresholds are designed to apply only to high-performance ASICs; older or less efficient devices are excluded. The policy directly targets hardware capable of competing at an industrial scale.

While Brazil’s import tax system includes other layers like IPI, PIS/COFINS-Import, ICMS…, reducing import duty to zero removes a significant cost barrier, shortening project payback periods.

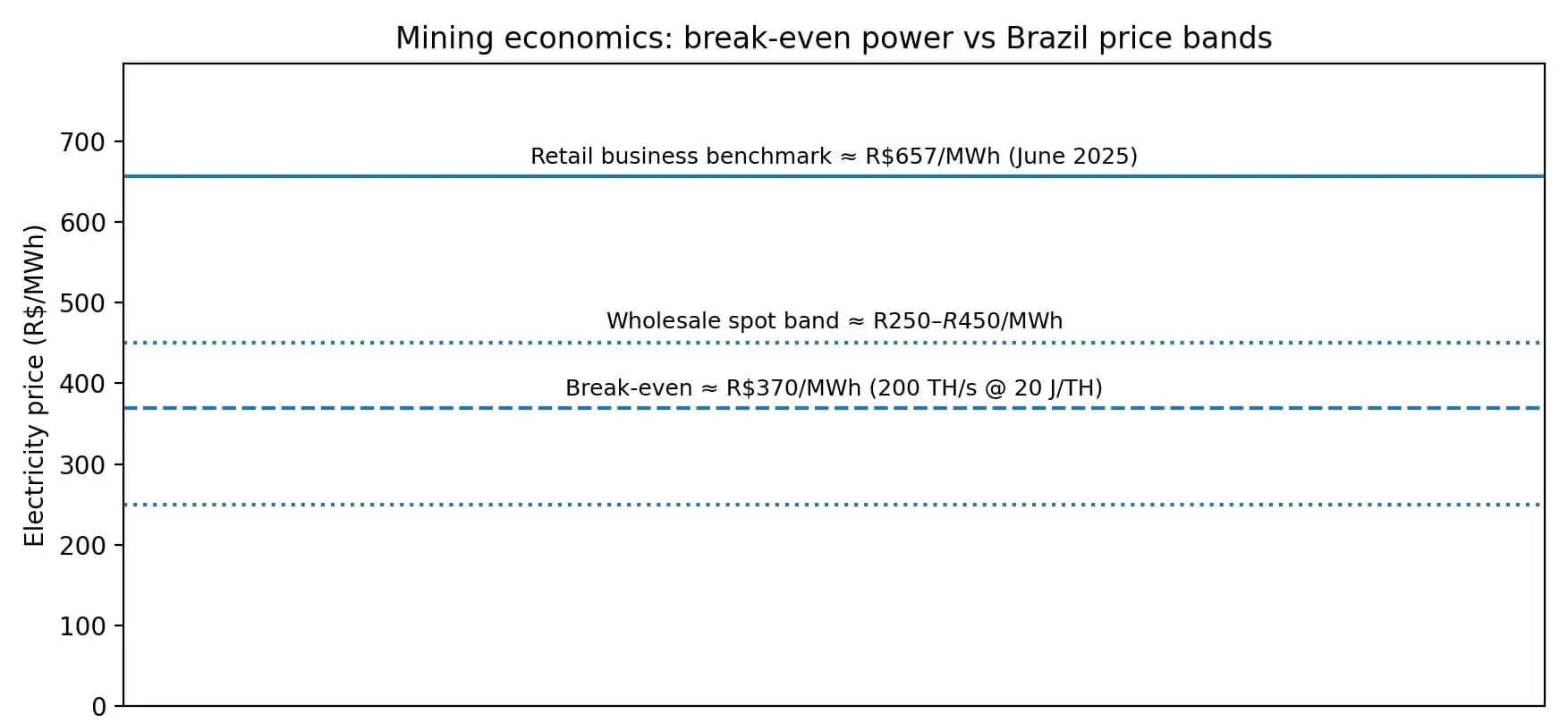

Bitcoin mining breakeven electricity price is around 370 R$/MWh, lower than Brazil’s wholesale spot price and much below retail rates, creating profit opportunities based on curtailment.## Breakeven electricity price

Bitcoin mining breakeven electricity price is around 370 R$/MWh, lower than Brazil’s wholesale spot price and much below retail rates, creating profit opportunities based on curtailment.## Breakeven electricity price

Mining profitability depends on three variables: hashprice (revenue per PH/s/day), hardware efficiency, and electricity costs.

On February 16th, hashprice was about $34.05/PH/s/day, while Bitcoin traded around $65,000 on February 25th. For a minimum qualifying machine (200 TH/s, 20 J/TH), estimated daily revenue is about $6.81. Power consumption is 4.0 kW, or 96 kWh per day.

Ignoring investment and operational costs, the breakeven electricity price is roughly $0.071 per kWh, or about 370 reais/MWh (exchange rate around 5.17 reais/USD). Meanwhile, the average retail price for businesses in Brazil in June 2025 was 0.657 reais/kWh (657 reais/MWh)—too high for profitable mining.

However, spot wholesale prices typically range between 250–450 reais/MWh. More importantly, curtailed electricity essentially has no buyers. If generators can sell the “lost” output at or below breakeven prices to miners, they can recover revenue instead of losing it entirely.

The mechanism is clear: curtailment creates stranded value; Bitcoin mining converts that value into computational capacity; the ex-tariff policy reduces hardware costs enough to open profit margins.

What happens if this scenario materializes?

If curtailment continues to rise as renewables expand faster than transmission capacity, revenue pressure on generators will intensify. Bitcoin mining can be deployed via bilateral PPAs, without new transmission, and can be quickly activated after equipment installation. The 0% tariff window until January 2028 provides roughly 24 months for companies to lock in hardware costs and test project economics.

If, within the next year, many colocated agreements emerge between miners and large renewable projects, Brazil could become a significant hashrate hub—not through direct subsidies, but through economically attractive projects.

However, this thesis could also fail. If transmission infrastructure upgrades quickly, curtailment decreases, and electricity prices rise, the “stranded value” shrinks. If Bitcoin’s difficulty increases sharply, lowering hashprice, breakeven prices will fall below curtailment levels. If permitting and grid connection delays occur, hardware cost advantages diminish. And if the ex-tariff expires in January 2028 without renewal, the tariff barrier will reappear.

What is Brazil really betting on?

Brazil isn’t claiming to become a global mining hub. Instead, it aims to reduce costs for a hardware class capable of addressing the grid’s structural issues, while a major state-owned company publicly tests this hypothesis.

The core question isn’t about a national strategy but about project economics: can miners absorb enough curtailed electricity to improve plant efficiency without adding systemic risks?

If yes, Brazil could attract additional hash rate without direct subsidies: miners pay for electricity, generators recover revenue, and the tariff policy merely reduces friction. If not, the policy will expire in January 2028, ending the “experiment.”

Currently, conditions are converging: rising curtailment, falling hardware costs, and a large power producer publicly analyzing the problem. The window of opportunity remains open until early 2028—what happens afterward depends on market actions.

Related Articles