Hyperliquid’s PURR Stands Alone in Profit as DAT Peers Sink Into Losses

Operating income, not passive token reserves, gives PURR a structural edge as DAT peers face heavy unrealized losses.

Digital Asset Treasury products face mounting pressure as crypto prices remain below prior cost bases. As a result, most treasury vehicles tied to passive holdings now carry heavy unrealized losses. Artemis data shows only one exception. Hyperliquid Strategies’ PURR remains in profit while peers struggle to recover.

Hyperliquid’s PURR Defies DAT Slump With $356M Unrealized Profit

According to Artemis, PURR holds roughly $356 million in unrealized gains. In contrast, every other tracked Digital Asset Treasury product sits underwater. Among them, Bitmine posted the deepest deficit, exceeding $7.5 billion. Meanwhile, Strategy and several asset-heavy treasuries report multi-billion-dollar mark-to-market losses.

Hyperliquid Strategies ($PURR) stands alone as the only DAT in the green, with $356M in unrealized gains while the rest sit underwater. pic.twitter.com/6NycrekHp3

— Artemis (@artemis) February 27, 2026

In most cases, DAT products hold large amounts of Bitcoin and other cryptocurrencies. Therefore, balance sheets move almost entirely with spot prices. Recent volatility has translated directly into widespread unrealized losses.

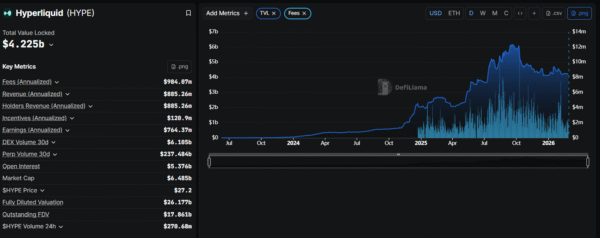

Instead of relying on passive token reserves, PURR links to the economics of the Hyperliquid protocol. Current protocol data shows about $4.2 billion in total value locked. At the same time, annualized fees approach $984 million, while annualized earnings are near $764 million.

Operating Income Gives PURR Structural Advantage Amid Treasury Losses

Over the past 30 days, Hyperliquid processed more than $237 billion in perpetual volume. Open interest stands above $5.3 billion. As a result, the platform operates as a high-margin derivatives venue with consistent fee generation.

_Image Source: _DeFiLlama

Unlike BTC-heavy treasuries that depend on price recovery, Hyperliquid generates operating income even during choppy markets. Moreover, earnings relative to its roughly $6.5 billion market cap imply a compressed valuation multiple compared with many crypto growth names.

The contrast becomes clear in current conditions. Passive treasuries face mark-to-market pressure and extended breakeven levels. Consequently, many remain materially above prevailing spot prices. Unless crypto markets reclaim key cost-basis zones, capital impairment could persist.

PURR’s profitability reflects operating exposure rather than pure beta. In effect, cash flow provides a buffer that passive structures lack. The performance gap may persist if price momentum stays uneven.

Related Articles

PEPE Jumps 2.3% With $337M Volume Surge — Is $0.054135 the Next Breakout Trigger?

NEAR Surges 14.5% — Will a Break Above $1.25 Ignite a Run Toward $3–$4?

SHIB Tests $0.0560 Resistance as Broader Altcoin Cycle Extends Toward 2026

Crypto Market Drops 3% As Fear Index Hits Extreme

ASTER Holds $0.70 After Channel Breakout as Traders Eye Key FVG Zone

PEPE Holds $0.053796 Support After 12% Drop Amid $580M Trading Spike