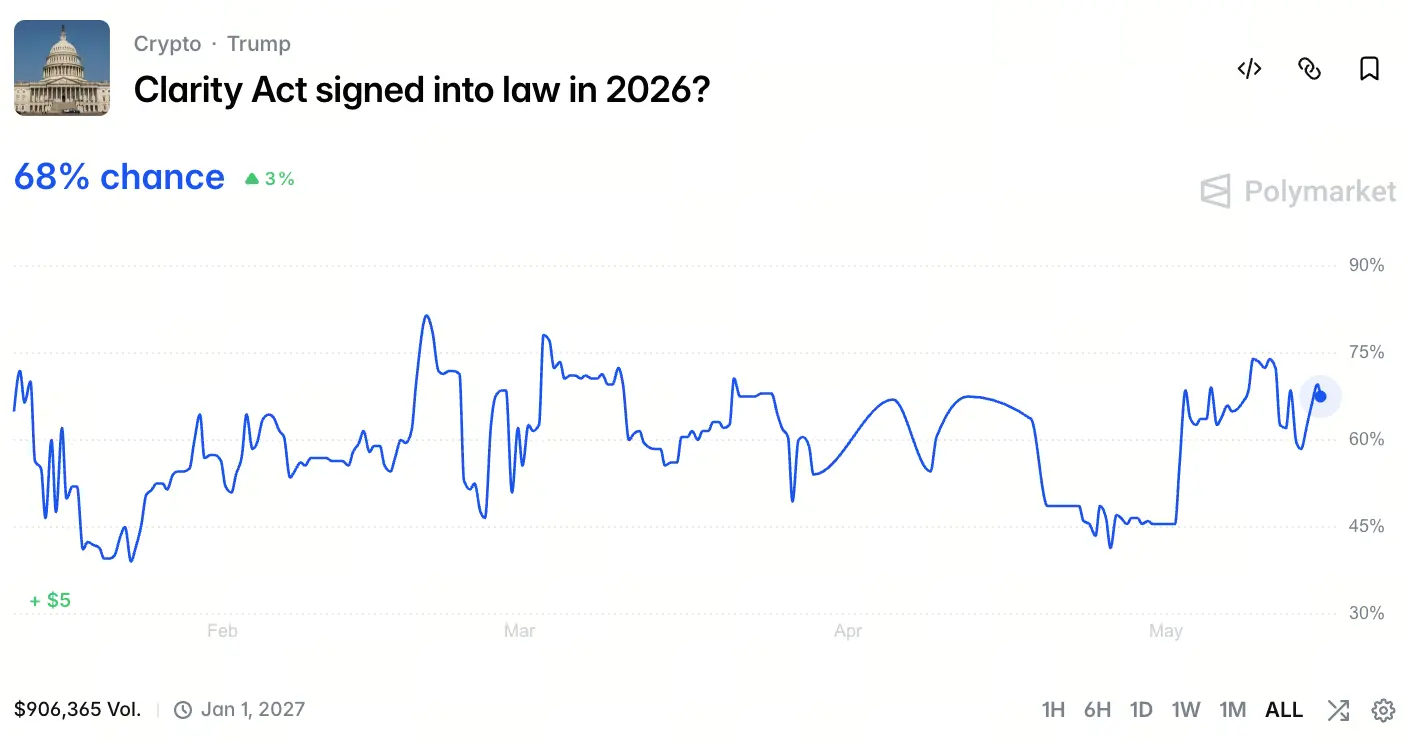

On May 15, 2026, the U.S. Senate Banking Committee officially passed the Digital Asset Market Clarity Act (CLARITY Act) with a vote of 15 in favor and 9 against, marking a key step forward in the legislative process for this long-mooted Crypto regulatory framework. The bill will then be submitted for a full Senate vote. The White House aims to complete the legislative process by July 4. As of the time of writing, market forecasts have raised the probability that the bill will ultimately be signed into law to 68%. This legislative development is pushing the U.S. digital-asset regulatory logic to transition from enforcement-based supervision to legislative recognition and clarification.

What core long-standing regulatory problems in the market does the bill solve

The core mission of the CLARITY Act is to provide clear classification standards for digital assets. For years, the U.S. Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) have had overlapping jurisdiction and ambiguous standards when it comes to characterizing Crypto assets. The same token could be viewed as both a security and a commodity under different regulatory contexts, putting issuers, exchanges, and developers in compliance dilemmas.

By establishing “de-securitization” judgment criteria, the bill clarifies under what conditions a digital asset can break away from an investment-contract status and become a non-security attribute. This mechanism fundamentally reduces regulatory uncertainty for projects at different stages of a token’s lifecycle.

How will the SEC and CFTC regulatory boundaries be reshaped

The bill makes structural adjustments to the power boundaries of the two agencies. The SEC retains jurisdiction over digital assets in the “initial issuance stage” that also exhibit characteristics of an investment contract, focusing on disclosure in financing activities and investor protection. Once a type of digital asset reaches a sufficient degree of decentralization or meets functional standards, jurisdiction would be transferred to the CFTC, with the asset being brought under the regulation framework for commodity-type digital assets.

This “dynamic jurisdiction transfer” mechanism replaces the former either-or approach to characterization and provides a compliance pathway for hybrid assets. The two agencies are required to jointly publish implementing details within 180 days after the bill takes effect, clarifying the technical decision indicators.

How will the asset classification standards change exchanges’ regulatory characterization of tokens

For exchange ecosystem tokens, the CLARITY Act’s characterization shift is especially direct. Previously, exchange tokens that rank high by circulating market value have long been in a regulatory gray area due to the overlap of ecosystem functions and financing attributes. The bill’s classification logic requires regulators to judge based on the token’s actual current function rather than the financing behavior at the time of issuance.

This means that if, after issuance is complete, a token achieves sufficient network decentralization, has functionally independent utility, and holders no longer rely on third-party efforts to form reasonable expectations, it could be reclassified as a non-security. This change will directly affect exchange-token compliance costs, listing strategies, and the structure of secondary-market liquidity.

How will DeFi protocols and stablecoin issuers’ compliance paths be reshaped

Decentralized Finance (DeFi) protocols and stablecoin issuers are the two directly related parties to the bill’s push:

- For DeFi protocols, the bill clearly distinguishes between protocol development activities and protocol operation activities. Code development and open-source contributions typically do not constitute a regulatory trigger, while the issuance and distribution of governance tokens for a protocol require compliance assessment based on the degree of decentralization.

- For stablecoins, the bill sets up a dedicated registration framework for payment stablecoins, requiring issuers to meet standards such as reserve asset transparency, 1:1 fully backed redemption, and anti–money laundering compliance. Compliant stablecoins will be explicitly excluded from SEC/SEC-related securities law jurisdiction, clearing institutional obstacles for payment-scenario applications.

What kind of political and economic game does the 15:9 committee vote reflect

The Senate Banking Committee vote split of 15 in favor and 9 against reflects a subtle balance between the two parties on digital asset regulation issues. The supporting votes include senators from both parties, indicating that the CLARITY Act has formed cross-party consensus around its core demands of “clear rules” and “prevent regulatory arbitrage.”

The opposing viewpoints mainly focus on two areas: some believe that the bill’s definition of decentralization standards still leaves ambiguity and could be used by large institutions for compliance arbitrage; others worry that after regulatory power shifts from the SEC to the CFTC, investor protection standards may diverge structurally. Even so, the 15:9 margin implies that the bill has significant political momentum before it enters the full Senate vote.

What logic is driving the market probability of completion of legislation to rise to 68%

Source: Polymarket

As of May 15, 2026, according to data shown on the Polymarket page, the market predicts the probability of the CLARITY Act ultimately being signed into law is 68%, a figure calculated using multiple weighted factors.

First, the high-vote passage by the Senate Banking Committee greatly lowers the threshold for the next full-vote stage. Second, the White House has clearly set completing the legislation by July 4 as a policy goal, meaning the executive branch has already reserved political capital to push the process forward.

Third, over the past 18 months, the bill text has undergone multiple rounds of bipartisan negotiations and revisions, and extremely controversial provisions have been replaced or removed.

Finally, Crypto industry political donations and lobbying spending in the election cycle from 2024 to 2026 have increased significantly, creating sustained legislative pressure. The remaining 26% uncertainty mainly comes from amendment risks during the full Senate vote and potential procedural delays.

A demonstration effect for other global jurisdictions is beginning to take shape

The progress of the U.S. CLARITY Act is not an isolated domestic legislative event; its demonstration effect on the global digital asset regulatory landscape is already evident. The EU’s MiCA framework has entered the implementation phase, but its level of refinement in asset classification still differs from the CLARITY Act.

Hong Kong has clearly proposed the principle of “same business, same risk, same rules” for virtual asset regulation and is observing how the U.S. legislation balances incentives for innovation with risk controls. Singapore’s MAS stablecoin regulatory framework is also entering an iteration window.

If the bill is ultimately approved, it will strengthen the global mainstream position of “function-oriented” regulation, pushing countries to accelerate the rollout of more operational classification standards rather than broad policies of outright bans or laissez-faire.

What uncertain risks still exist in the current legislative process

Despite the strong momentum for the CLARITY Act, a comprehensive review can still identify several potential risks. The full Senate vote stage could trigger amendment debates targeting “decentralization determination thresholds”; if the standards are tightened excessively, the bill’s compliance buffer for small and medium-sized projects could be weakened. In addition, after the bill formally takes effect, the process for the SEC and CFTC to jointly draft implementing details could be prolonged due to institutional power and interest games, creating a gap between actual enforcement and the legislative intent. Finally, 2026 coincides with the U.S. midterm election cycle, which could squeeze the legislative timetable as election politics dominate the agenda, and the goal of completing the legislation by July 4 still faces some pressure.

FAQ

Q: After the CLARITY Act passes, do currently issued tokens need to reapply for compliance recognition?

A: The bill does not require already-issued tokens to complete a new initial registration. However, issuers must conduct a self-assessment based on the decentralization and functional standards set by the bill. If the token is reclassified as a non-security, it would no longer be bound by the SEC’s ongoing disclosure obligations. Regulators will provide an official application channel for recognition.

Q: What impact does the bill have on Crypto projects outside the U.S.?

A: The bill mainly applies to issuance, trading, and sales activities within U.S. jurisdiction. But if a non-U.S. project provides services to U.S. users or its tokens are listed on U.S. exchanges, it must comply with the classification and compliance requirements established by the bill. This could lead global Crypto projects to proactively reference the bill’s standards when designing tokenomics.

Q: After the bill takes effect, will compliance obligations for individual investors participating in Crypto asset trading change?

A: Individual investors’ trading activities themselves do not create new registration or reporting obligations because of the bill. However, compliance requirements differ across trading venues for different categories of digital assets, so investors must ensure the trading platform they use has completed the appropriate licenses or permit arrangements under the bill. Compliance-oriented operators like Gate will continue to provide users with trading environments that fit within the regulatory framework.

Q: After the CFTC takes over regulation of non-security digital assets, will its regulatory力度 be weaker than the SEC’s?

A: The CFTC’s regulatory framework focuses on preventing market manipulation and regulating trading conduct, rather than information disclosure at the issuance end. The two models have different emphases and there is no simple “stricter vs looser” distinction. The CFTC’s compliance requirements for commodity trading platforms are also equally stringent, including requirements for segregating customer funds, reporting obligations, and risk-control standards.