In May 2026, one of the most persistent narratives in the Crypto market began to loosen. Strategy (formerly MicroStrategy), this corporate whale holding nearly 4% of the total Bitcoin supply, for the first time officially acknowledged in its quarterly report: to pay preferred stock dividends, repay convertible notes, or meet redemption needs, the company might need to sell some of its Bitcoin. This statement quickly ignited trading enthusiasm in the prediction market.

Source: Polymarket

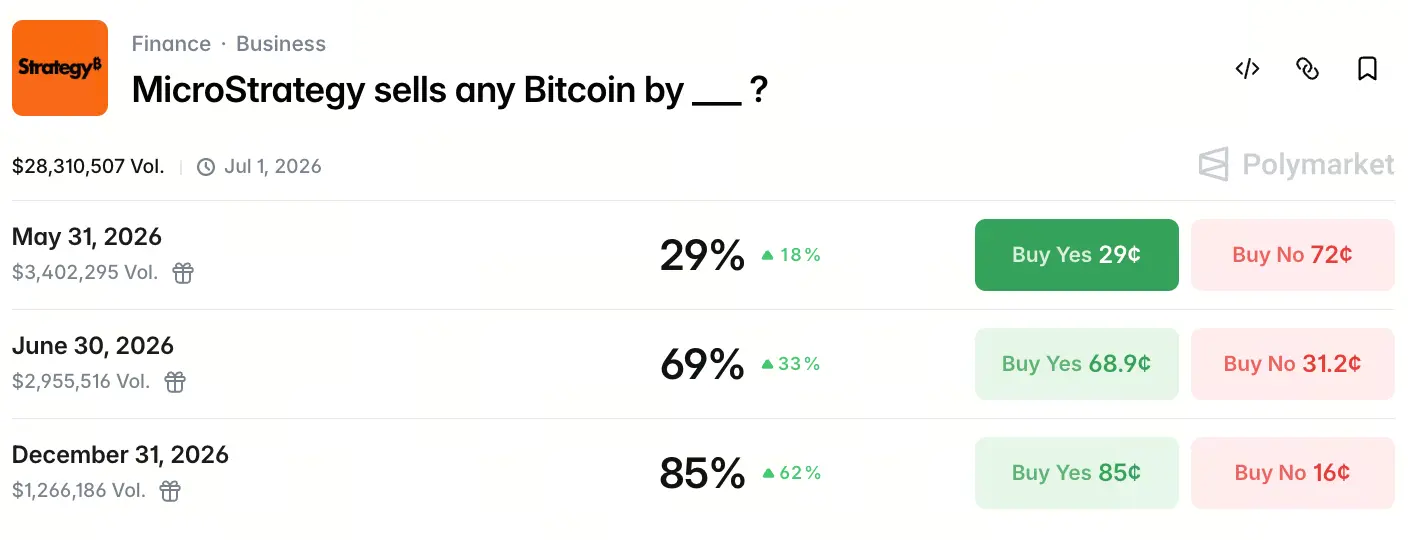

As of May 18, 2026, the total trading volume on Polymarket for the contract “MicroStrategy will sell any amount of Bitcoin before ____” has reached $28.3 million. The probabilities at three key time points formed a clear expectation curve: the probability of selling before May 31 is 29%, rising to 69% before June 30, and reaching 85% before December 31. The market is not betting on “whether” it will sell, but on “when” it will sell.

Why Strategy’s high-probability selling expectation suddenly emerged

On May 5, 2026, after Strategy released its Q1 earnings report, its core narrative of “never selling coins” was rewritten by the official release. The report shows the company holds 818,334 BTC, accounting for 3.9% of the total BTC supply, with an average cost basis of about $75,500. But more importantly, in its risk disclosures, the company formally listed “selling BTC” as one of the possible options to raise cash.

During the earnings call, Michael Saylor made an even more direct statement: “We may sell some Bitcoin to pay dividends, and the purpose is to give the market a shot—so everyone knows this can happen. The company is fine, Bitcoin is fine, and the industry is fine.” CEO Phong Le added further: “When it is in the best interest of the company, we will sell Bitcoin. We won’t just sit there and say we’ll never sell.”

This line effectively ended the underlying commitment that enabled Strategy to command an MSTR valuation premium over the past five years. Once the discipline of “never selling” was broken, the market began to reprice at scale.

Has the dividend pressure from STRC priority shares already reached a tipping point?

STRC is Strategy’s perpetual preferred stock product launched in 2025, with an annualized dividend yield of about 11.5% and a cumulative issuance size of about $8.5 billion. Unlike common stock MSTR, preferred stock does not rely on share price premiums to sustain operations; instead, it requires the company to continuously pay fixed cash.

In Q1, Strategy’s software business generated revenue of about $124.3 million, up about 11.9% year over year, but against an annual dividend obligation of about $1.5 billion, this figure is almost negligible. The company has about $2.25 billion in cash reserves, but this money also needs to address a redemption requirement for about $1 billion of convertible notes in 2027.

The structural contradiction of STRC is that it provides funding for the company to buy BTC at scale, but it also creates persistent pressure from ongoing cash outflows. Without selling BTC, cash reserves can only offer limited buffer. The Polymarket sell probability of 69% by the end of June largely reflects the market’s recognition of this cash shortfall.

How tax arbitrage becomes the core motive to sell Bitcoin

Beneath the surface of “selling coins to pay dividends,” tax factors may be the real driving force.

In Q1 2026, Strategy recorded a net loss of about $12.54 billion, mainly due to unrealized losses on its books caused by large fluctuations in the BTC price. This loss created a deferred tax asset of about $2.2 billion on the company’s balance sheet.

By selling some BTC—especially BTC purchased at a cost basis higher than the current market price—Strategy can convert these book losses into actual tax deductions, offsetting future tax on capital gains. This is not an isolated move: in December 2022, Strategy sold 704 BTC at $16,776 per coin to harvest tax losses, then repurchased 810 BTC within two days at a higher price.

The difference from the 2022 operation lies in both scale and narrative level. The tax benefit space involved now is as high as about $2.2 billion, and the company has made clear that selling BTC is being included as a proactive tool in asset-liability management. This is no longer “a one-time loss harvest,” but a potential system-level adjustment to strategy.

Do convertible note maturity and debt structure create selling pressure?

Another layer of pressure is hidden in Strategy’s capital structure: the maturity of convertible notes.

The company has about $8.2 billion in principal of convertible notes, with the first repayment cycle starting in September 2027. Based on analysts’ estimates, if the MSTR stock price is below about $183 (corresponding to a BTC price of about $91,500) at that time, bondholders may choose to redeem rather than convert into stock, forcing the company to use cash reserves or sell assets to repay.

Currently, Strategy’s cash reserves of about $2.25 billion can cover the first repayment pressure in 2027, but for 2028 there is no clear solution for the larger-scale debt maturity. Compared with the debt pressure in 2027, the core motivation for selling BTC in 2026 still centers on dividend payments and tax optimization. But the debt structure itself determines that the “option to sell BTC” has been formally incorporated into the company’s strategic toolbox for 2026.

Why the MSTR narrative premium is facing a structural reshaping

Strategy’s valuation logic over the past five years was built on three core pillars: continued accumulation of BTC, never selling BTC, and maintaining growth in BTC per share via share dilution. Among them, “never selling” is the fundamental reason MSTR earned a large premium versus its BTC net asset value (NAV)—investors paid that premium for the promise.

Saylor’s loosening— even if it’s only a small, strategic sale—would shake the premium logic at its core. The market will no longer treat Strategy as a passive vehicle for “hoarding coins,” but will reprice it as a “financial company that actively manages a BTC asset-liability balance sheet.”

With the probability of selling reaching 85% before year-end on Polymarket, what’s being reflected is not a pessimistic view on the BTC price, but the market repricing Strategy’s business model evolution path. That probability itself is a kind of “expectation coordinate”: the market is no longer debating whether it will sell, but speculating about the timing of the sale.

How big is the real impact on BTC market liquidity from the whale’s selling?

From the standpoint of market capacity, if Strategy sells part of its holdings, the direct impact on spot BTC liquidity may be limited.

According to Gate market data, as of May 18, 2026, the BTC price has been trading in a range around $77k. If Strategy were to sell only 1% of its holdings (about 8,183 BTC, worth about $660 million), this size would only be equivalent to 1 to 2 days of normal trading volume on the CME or spot market. Exchange BTC holdings have fallen to about 2.693 million BTC, the lowest level in seven years, meaning the market’s capacity to absorb far exceeds this scale.

The bigger risk is at the narrative level. Once an enterprise whale holding nearly 4% of total supply begins selling—no matter how small the amount— it will release a signal to the market: “the biggest long is starting to de-risk.” This expectation effect may trigger follow-through behavior from other institutional holders and miners. In Q1 2026, publicly listed mining companies collectively sold about 32,000 BTC, exceeding the total for all of 2025; the market’s supply side is already in a relatively sensitive state. Strategy’s decision to sell could become a catalyst for broader selling pressure.

Summary

From “never selling” to “sell depending on the situation,” Strategy’s narrative shift is one of the most iconic events in the 2026 Crypto market.

The $28.3 million volume on Polymarket and the 85% probability of selling by year-end reflect the market’s pricing of this shift. The drivers behind the selling decision are not only STRC’s dividend pressure, but also about $2.2 billion of tax arbitrage space, the convertible note maturity structure, and the business model evolution from a “coin-hoarding narrative” to “asset-liability management.” The expected time window is distributed in steps: the probability in Q2 is significantly higher than in Q1, with the highest probability by year-end.

The loosening of the narrative premium may have an even deeper impact on the market than the actual selling actions. Strategy’s value positioning is moving from “a symbol of Crypto belief” to “a financial institution that actively manages Crypto assets”—and this transition itself may be more worth the industry’s attention than the sale of any specific quantity of BTC.

FAQ

Q1: How much Bitcoin does Strategy currently hold? What is its average cost?

As of May 2026, Strategy holds 818,334 BTC, accounting for 3.9% of the total BTC supply. Its cumulative purchase cost is about $6.18 billion, with an average cost of about $75,537.

Q2: How are probabilities calculated on Polymarket?

Polymarket is a decentralized prediction market where users express their judgment about event outcomes by buying “Yes” or “No” contracts. The contract price (between 0 and 1) directly corresponds to the probability implied by the market. The higher the probability, the more capital is betting that the event will happen.

Q3: If Strategy sells Bitcoin, how much impact would it have on the BTC price?

If it sells only a small amount of BTC (such as 1% of holdings, about 8,183 BTC), the direct impact on spot market liquidity is limited because daily average trading volume is far larger than this scale. The bigger risk lies at the narrative level: de-risking behavior by the biggest corporate long could trigger follow-through from other institutions.

Q4: What is STRC? Why would it force Strategy to consider selling BTC?

STRC is a perpetual preferred stock product issued by Strategy, with an annualized dividend yield of about 11.5% and a cumulative size of about $8.5 billion. Unlike common stock, preferred stock requires the company to continuously pay fixed cash dividends, and Strategy’s software business revenue is insufficient to cover this expense—making selling BTC one of the realistic options to supplement cash flow.

Q5: Didn’t Strategy already sell Bitcoin in 2022? Why is this time getting more attention?

In December 2022, Strategy sold 704 BTC for the purpose of harvesting tax losses, then quickly repurchased them within two days. At the time, the operation was small in scale and short in cycle, so it did not affect the “overall buy but not sell” narrative. But this statement formally brings “selling BTC” into the company’s routine capital management toolbox, making the narrative-level impact far greater than the actual trading scale.